ORDER

R.K. Panda, Vice President. – This appeal filed by the Revenue is directed against the order dated 08.10.2025 of the Ld. CIT(A) / NFAC, Delhi relating to assessment year 2023-24.

2. Facts of the case, in brief, are that the assessee is an individual and has filed his return of income u/s 139 of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) for the impugned assessment year declaring total income of Rs.98,53,380/-. The case was selected for scrutiny under CASS on the ground that the sale consideration of the property reported in ITR is less than the sale consideration of property reported in SFT. Accordingly, the Assessing Officer issued statutory notice u/s 143(2) of the Act and thereafter notice u/s 142(1) of the Act along with a questionnaire were issued and served on the assessee in response to which the assessee filed his response.

3. During the course of assessment proceedings the Assessing Officer noted that the assessee has received an amount of Rs.33,00,00,000/- as sale consideration for immovable property. The value of the property as per the stamp valuation authority was declared at Rs.15,18,86,616/-. He noted that the assessee has claimed deduction under section 48 of the Act for the indexed cost of acquisition of Rs.32,44,30,676/- wherein the cost of acquisition was declared at Rs.9,80,15,310/-. Further, the assessee claimed deduction under section 54F amounting to Rs.14,47,358/-. The assessee accordingly declared long term capital gains of Rs.41,21,966/-.

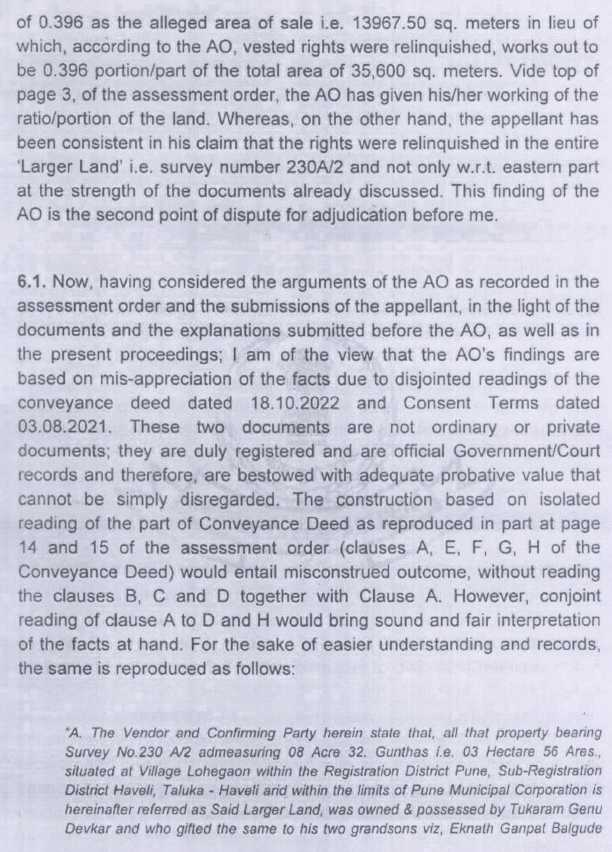

4. The Assessing Officer, on perusal of the sale deed, noted that the conveyance deed of Rs.83,36,27,000/- in respect of area admeasuring 01 hectare, 39.675 acres i.e. 13967.500 sq.mtrs out of survey No.230A/2, admeasuring 01 hectare i.e. 17800 sq.mtrs situated at village Lohegaon, Haveli Taluka, Pune was entered between the vendors M/s Lunkad Reality (partners Shri Amit Kantilal Lunkad & Shri Amol Kantilal Lunkad) and the Purchaser M/s Highspot Realtors LLP wherein the assessee was a confirming party. The assessee was paid an amount of Rs.33 crores for transferring his interest in the said property. Thus the capital asset transferred was the land admeasuring 13967.500 sq.mtrs. and the consideration received in respect of the above land was Rs.83,36,27,000/-. Out of Rs.83,36,27,000/-, Rs.33,00,00,000/- was received by the assessee, who was the confirming party in terms of the Consent decree dated 03.08.2021. The assessee has claimed cost of acquisition of Rs.9,80,15,310/- (F.Y.2001-02) in respect of the above land. He, therefore, issued a show cause notice asking the assessee to explain as to why the amount of Rs.33 crores should not be added to the total income under the head ‘Income from other sources”. The Assessing Officer noted that the assessee failed to submit any document in respect of cost of acquisition declared at Rs.9,80,15,310/- in the F.Y. 2001-02. He further noted that as per the sale deed the said property admeasuring 13967.50 sq.mtrs out of the larger land admeasuring 35,600 sq.mtrs was sold. As per the valuation report submitted by the assessee, the value determined at Rs.9,96,80,000/- is in respect of larger land admeasuring 35,600 sq.mtrs. The Assessing Officer further noted that the share of the assessee out of the sale consideration of Rs.83,36,27,000/- is only Rs.33,00,00,000/-. Therefore, he was of the opinion that the right of the assessee in the sold property be taken on proportionate basis i.e. Rs.33,00,00,000/ Rs.83,36,27,000 which works out to 0.396. The Assessing Officer accordingly worked out the indexed cost of acquisition at Rs.5,04,06,410/- as against Rs.9,96,80,000/- claimed by the assessee and worked out the long term capital gains at Rs.20,28,10,757/-. He accordingly assessed the total income of the assessee at Rs.21,26,64,137/- as against the returned income of Rs.98,53,380/-.

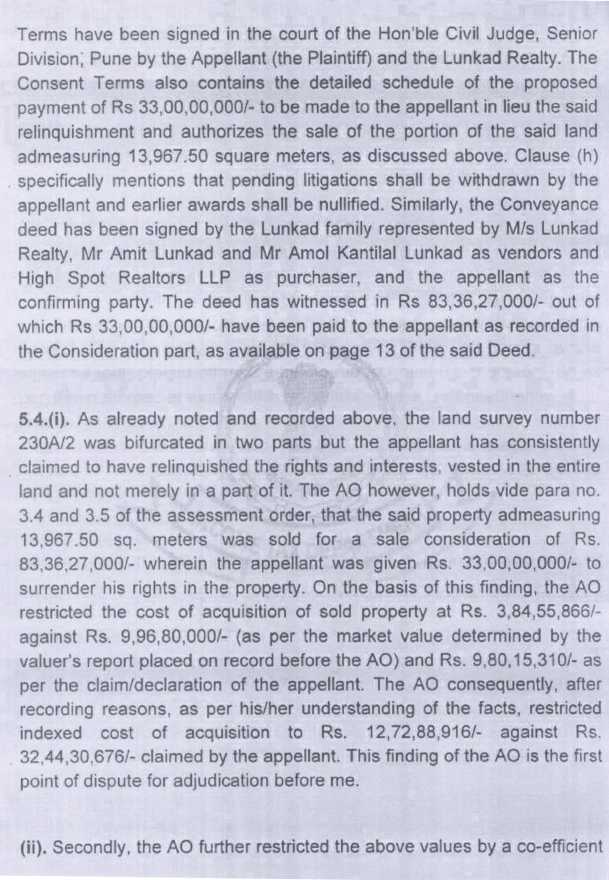

5. In appeal the Ld. CIT(A) / NFAC allowed the appeal of the assessee and deleted the addition holding that the assessee has relinquished his rights over the entire parcel of the land and the Assessing Officer was wrong in allowing the restricted cost of acquisition of land. The relevant observations of the Ld. CIT(A) / NFAC from para 5 onwards read as under:

6. Aggrieved with such order of the Ld. CIT(A) / NFAC the Revenue is in appeal before the Tribunal by raising the following grounds:

| 1. |

|

On the facts and circumstances of the case and in law, Ld CIT(NFAC) has erred in deleting the addition of Rs.20,28,10,757/- in Long Term Capital Gain arisen because of reduction in indexed cost of acquisition as Assessing Officer has allowed indexed cost of acquisition for 13967.50 sq mtr only. |

| 2. |

|

The Ld. CIT(A) has erred in allowing indexed cost of acquisition of Rs.32.44 cr holding that the assessee has received Rs.33 crs for waiver of interest/right for the entire larger land of 35,600 sq. mtr whereas the conveyance DEED dated 18.10.2022, in which the assessee in confirming party is for the part land admeasuring 13967.50 sq mtr sold to the Hotspot Realtors LLP by the vendor Lunkad Realty. |

| 3. |

|

The Ld. CIT(A) has erred in allowing indexed cost of acquisition of Rs.32.44 cr holding that the assessee has received Rs.33 crs for waiver of interest/right for the entire larger land of 35,600 sq mtr whereas as per para 10(a) of the consent term dated 4.08.2021, in which the assessee is plaintiff is for the part land admeasuring 13967.50 sq mtr only which was later on sold to the Hotspot Realtors LLP by the vendor Lunkad Realty. Also clause 10(g) of the consent term dated 4.08.2021 does not specify that the consent terms are for larger areas of land measuring 35600 sq mtr. |

| 4. |

|

Without prejudice Ld CIT(A) has failed to note that the development agreement signed by assessee with Balguide Family and others in 1989, the assessee has not acquired total rights in the entire area of 35,600 sq. mtr on payment of Rs.50,00,0000 because as per clause 8 of agreement 10.04.1989 of the development agreement, the landlord and assessee agreed to distribute the profit share in ratio of their share and allowance of cost of acquisition for entire area of 35,600 sq. mtr by CIT(A) is unjustified. |

| 5. |

|

The appellant craves leave to add, amend, alter or delete any of the above grounds of appeal during the course of the appellate proceedings before the Hon’ble Income Tax Appellate Tribunal. |

7. The Ld. DR strongly challenged the order of the Ld. CIT(A) / NFAC deleting the addition made by the Assessing Officer and filed a detailed written submission which reads as under:

“4.0 Contention of the Revenue

What is the cost of acquisition ?

4.1 First and foremost, it is important to appreciate that the capital asset transferred in this case vide conveyance deed 18.10.2022 by M/s Lunkad Realty to M/s Highspot Realtors LLP was land admeasuring 13,967.5 sq mtrs. at Survey No.230A/2. Please see Index-II (assessee’s paper book page no.67) and Schedule of property (assessee’s paper book page no. 95). Both the Index-II and Schedule of property clearly mentions that the land transferred was admeasuring 13,967.5 sq mtrs at Survey No.230A/2. Now, the sale consideration for this land admeasuring 13,967 was Rs.83,36,27,000/- as per page no.3 of the conveyance deed dated 18.10.2022. Rs.33,00,00,000/- received by the assessee, who was the confirming party, in terms of the Consent decree dated 03.08.2021 from the vendor M/s Lunkad Realty. Thus, in case of the assessee, full value of consideration received or accruing as a result of the transfer of rights in the capital asset i.e. land adm 13,967.5 sq. mtrs of land is the amount of Rs.33,00,00,000/-. From this would be deducted the cost of acquisition of the asset and cost of improvement and expenditure in relation to the transfer. The cost of acquisition to be deducted would be the cost of acquisition in relation to the asset transferred i.e. rights in land of 13,967.5 sq mtrs. However, in the case of the assessee, it is seen that the assessee has deducted cost of acquisition in respect of land admeasuring 35,600 sq. mtr which is not allowable as per section 48. The Ld. CIT(A) failed to appreciate the fact that cost of acquisition allowable to the assessee is the cost incurred to acquire the asset transferred i.e. the cost to acquire right in land adm. 13,957.5 sq. mirs. The Ld. AO had rightly determined the cost acquisition in relation to the asset transferred i.e. rights in land adm. 13967.5 sq. mtrs

Which asset has been transferred ?

4.2 Before we move ahead, it is important to first find out which is the land or asset which has been sold/transferred for which sale consideration of Rs.83,36,27,000/- was received by the vendor M/s Lunkad Realty. The land which is transferred is land admeasuring 1H 39.675 R out of Survey No.230A/2 admeasuring 1H 78R situated at Lohegaon, Pune. Originally, this land of 1H 39.675 R (13,967 sq.mtrs) was part of Larger Land admeasuring 3H 56R at Survey No.230A/2 (35,600 sq. mtrs). This Survey No.230A/2 was later (around 2011) was divided into two parts Survey No.230A/2 (also known as Eastern Part) adm. IH 78R and Survey No.A/2/1 (also known as Western part) admeasuring 1H 78R. It is also pertinent to mention here that PMC had acquired land adm 3832.50 R out of both Survey No.A/2 and Survey No A/2/1. It is seen that the Eastern part of land adm 13,967 out of total land a Survey No. A/2 is the subject capital asset which was transferred in this case. M/s Lunkad Realty was to pay the assessee Rs.31,00,00,000/- as per Consent decree dated 03.08.2021 for relinquishing rights in respect of this land adm. 13,967 out of total land at Survey No A/2 only.

Who owns the land at Survey No.A/2?

4.3 Now, we come to the issue of who was owner of the land at Survey No A/2. The para F and G of the Conveyance deed gives the complete detail of how Lunkad realty i.e. Vendor became owner and possessor of the said land at Survey No.A/2. It narrates that as per compromise decree dated 11.02.2022, the said larger land was partitioned and sub-divided into Survey No A/2 and Survey No.A/2/1. The Survey No.A/2 was owned by legal heirs of one, Late Balkrushna Ganpat Balgude and Survey No.A/2/1 was owned by Ali Asgar Dekhani (Prop. of Ramsar Builders). The para G clearly mentions that vide sale deeds dated 07.06.2014 and 10.06.2014, the vendor i.e. Lunkad Realty has purchased area admeasuring 13967.50 sq. mtrs out of the said Larger land and mutation entry nos 4077 and 0878, name of the vendor is recorded as owner and possessor on the 7/12 extract for Survey No 230A/2 for area admeasuring 13967.5 sq mtrs. Thus, in view of the above, it is clear the Ld. CIT(A) failed to note that the capital asset transferred vide conveyance deed was smaller part adm 13,967.5 sq.mtrs and not the larger land adm.35,600 sq. mtrs.

What is the extent of assesse’s right in land at Survey No.A/2?

4.4 Further, it is seen that the assessee was not the whole and sole owner of the transferred land adm. 13,967 sq. mtrs. It had certain rights in the land created through various agreements with the original owners of the land (Balgude family) and the actual owners of the land (vendor as per the conveyance deed) starting with the Development agreement dated 10.04.1989. In fact, the name of the assessee has never been entered in the official land records as owner of the property. As noted in the above para and in the para H of the conveyance deed, it was the M/s Lunkad Realty who is recorded as owner and possessor on the 7/12 extract for Survey No 230A/2 for area admeasuring 11967.5 sq mtrs. The assessee has not submitted any evidence to show that it is the whole and sole owner of the transferred land. The very fact that the conveyance deed dated 18.10.2022 mentions Lunkad Realty as the “Vendor” and the assessee as mere “Confirming Party” clearly shows that it is the Lunkad Realty who has the greater ownership right and the assessee, though has certain rights in the said land, cannot by any stretch of imagination be called as whole and sole owner of the land. Thus, Ld. CIT(A) failed to note that the assessee was not the owner of the land by held only certain rights by virtue of a development agreement dated 10.04.1989. Ld. CIT(A) overlooked the important fact before allowing the assessee cost of acquisition in relation to the larger land (35,600 sq. mtrs) when the assessee was not the sole owner of even the smaller part (13,967 sq. mtrs). The failure of the Ld. CIT(A) to appreciate this crucial fact has resulted in perverse finding that the assessee was entitled to deduct entire cost of acquisition in relation to the larger land (35,600 sq. mtrs) from the full value of consideration received by him in relation to the certain rights (not whole and sole ownership) in the smaller land (13,967) which was actually sold.

4.5 Ld. CIT(A) also failed to appreciate the fact that the development agreement dated 10.04.1989 submitted by the assessee is only in respect of the development rights of the land. In fact, para 8 (page no.130 of the assesse’s paper book) clearly mentions that due to lack of resources the original owners of the land are not able to develop the land and therefore, they have decided to get the land developed and to divide the resulting financial returns (arthik mobadla in Marathi) amongst themselves as per their share. This shows clearly shows that the rights acquired by the assessee in land were limited. Allowing the assessee complete deduction of cost acquisition even in respect of smaller part (13,967 sq. mtrs) may result in absurd situation wherein the vendor i.e. Lunkad Realty would also claim complete deduction of cost acquisition in respect of smaller part (13,967 sq. mtrs).

4.6 Ld. CIT(A) completely failed to appreciate the importance of Consent Decree dated 04.08.21. This is legal document before the Hon Civil Judge. In para 11(a) clearly mentions that the assessee is surrendering his all rights, title and interest in S.No. A/2, admeasuring 11.967.5 sq mtrs in lieu of payment of Rs.33,00,00,000 does not mention the rights in larger land admeasuring 35,600 sq mtrs. Thus, the Ld. CIT(A) ought to have appreciated that the sale consideration received by the assessee is in lieu of his rights in land adm 13967.5 sq mtrs and ought to have allowed the cost of acquisition only in respect of this land and not the larger land adm.35,600 sq. mtrs.

What is the nature of consideration paid to the assessee?

4.6.1 The larger land adm. 35600 sq.mtrs has been divided into two parts, one is Survey No A/2 and other being Survey No.A/2/1. Both having area adm 13,967.5 sqmtrs. It is pertinent to mention here that the consideration was received by the assessee for his rights in land adm 13967.5 sq mtrs from Lunkad Realty who wanted to clear the encumbrance over their land at Survey No.A/2. The Lunkad Realty owned only Land at Survey No.230A/2 and not Survey No.230A/2/1. Ld. CIT(A) ought to have realised that M/s Lunkad Realty would only be interested in clearing encumbrance over his own land i.e. land adm.13,967.5 sq. mtrs and not the encumbrance over the entire land admeasuring 35,600 sq. mtrs.

4.6.2 Ld.CIT(A) also failed to consider the para 11(h) in correct perspective. Ld.CIT(A) had wrongly concluded that by virtue of para 11(h), the rights of the assessee in Survey No.230A/2/1 have also been exhausted. However, the fact is that para 11(h) clearly mentions that all rights in land assigned to the defendant i.e. Lunkad property in respect of the other portion of land i.e. Survey No.230A/2/1 shall remain with the plaintiff i.e. the assessee. Further, in the last line of para 11(h), it is clearly mentioned that the assessee would be at liberty to enforce his rights against other third parties in respect of the Survey No.A/2/1 and the Lunkad realty will have no objection in this regard. This is completely opposite of what Ld.CIT(A) has concluded in his order. Thus, the finding of CIT(A) is perverse with regard to surrender of rights by the assessee in respect of S.No.230A/2/1.”

8. The Ld. Counsel for the assessee on the other hand while supporting the order of the Ld. CIT(A) / NFAC also filed a detailed written submission. He submitted that the consideration of Rs.33 crores was received as a lump sum, global settlement for the complete extinguishment and relinquishment of all his rights, title and interest in the entire larger property admeasuring 35,600 sq.mtrs (Survey No.230A/2). Consequently the assessee is entitled to the indexed cost of acquisition for the entire 35,600 sq.mtrs. He submitted that this position is conclusively established by an independent and conjoint reading of the foundational documents, the court pleadings, the settlement terms and the subsequent conduct of the parties.

9. The Ld. Counsel for the assessee referring to the agreement entered in 1989 and the Joint Venture agreement entered in 2005 submitted that the assessee acquired development rights and possession of the entire land admeasuring 35,600 sq.mtrs vide the Development Agreement and the Possession receipt dated 10.04.1989. This fact is undisputed by the Revenue. He submitted that the Joint Venture agreement dated 09.11.2005 executed between the assessee and Lunkad Reality was for a sub-portion (1,50,000 sq. ft. or approx. 13,935 sq.mtrs.) of this larger land (the western portion). The balance remained independently with the assessee. This establishes that the assessee’s rights were never confined to any one portion but extended over the entire 35,600 sq. mtrs.

10. Referring to the civil suit No.408/2013 he submitted that when disputes arose due to the Balgude family executing parallel documents with Lunkad Realty in 2006 and Ramsar Builder in 2010 the assessee filed Special Civil Suit No.408/2013. He submitted that the suit was filed for the specific performance of 1989 agreement in respect of the entire 35,600 sq. mtrs. and not just a fraction of it. He submitted that the alternative relief sought in the suit was for damages of Rs.112,50,00,000/- which was calculated based on the saleable area of 3,75,000 sq. ft. representing the aggregate developable area of the entire 35,600 sq. mtrs. The legal claim that was ultimately settled was therefore a claim over the whole property. He submitted that the Consent terms dt 03.08.2021 must be read as a whole to understand the true nature of Rs.33 crore consideration. It was not a payment for the eastern portion alone but a comprehensive buyout of the assessee from the entire property.

11. Referring to various clauses of the Consent Terms dated 03.08.2021 he drew the attention of the Bench to clause (d) of the same which records that “all rival claims of the plaintiff in this suit . stands dissolved / relinquished.” He accordingly submitted that the claims in the suit extended to the entire 35,600 sq. mtrs. Referring to clause (e) of the Consent Terms dated 03.08.2021 he submitted that the said clause records that Lunkad Realty admitted the 1989 agreement and 1989 possession receipt and that the possession derived under those documents was handed over to Lunkad Reality. Since the 1989 documents covered the entire 35,600 sq.mtrs., therefore, the possession handed over was of the entire land. Referring to clause (h) of the Consent Terms dated 03.08.2021 he submitted that the said clause explicitly cancels the 2005 JV agreement (and its supplementary agreements) pertaining to the Western portion (renumbered as Survey No.230A/2/1). It nullifies the related arbitral award. He submitted that the conveyance deed dated 18.10.2022 fortifies the fact. Thus, there is no separate consideration provided in the Consent Terms for the cancellation of the assessee’s rights in the western portion. He submitted that the amount of Rs.33 cores received by the assessee is the single, consolidated consideration for the assessee exiting the entire property i.e. both the eastern and western portions.

12. Referring to the Conveyance Deed dated 18.10.2022 he drew the attention of the Bench to various clauses and submitted that the said conveyance deed expressly records surrender of the larger land. He submitted that while the conveyance deed was executed to transfer the title of the eastern portion (13,967.50 sq. mtrs.) to a third party purchaser (High Spot Realtors LLP), the recitals concerning the assessee i.e. the confirming party deliberately use the terminology of the larger land. Referring to clause (A) of the conveyance deed dated 18.10.2022 he submitted that the said clause defines the “said larger land” as the full Survey No.230A/2 admeasuring 08 Acre 32 Gunthas (35600 sq. mtrs.) He submitted that clause (B) of the conveyance deed dated 18.10.2022 records that the assessee obtained development rights and possession of the said larger land. Referring to clause (D) of the conveyance deed dated 18.10.2022 he submitted that the said clause records the cancellation of 2005 JV agreement which was for a part of the said larger land. He submitted that Clause (H) of the conveyance deed dated 18.10.2022 explicitly records that ‘the confirming party is surrendering all right, title and interest with delivery of possession in favour of the Vendor for consideration of Rs.33 crores’. He submitted that it does not restrict this surrender to the Eastern portion and records the consideration as being for the surrender of rights in the said larger land.

13. The Ld. Counsel for the assessee submitted that the practical and factual culmination of this global settlement is most evident in the subsequent fate of the western portion of the land. He submitted that it is a matter of undisputed fact that Ramsar Builder subsequently sold a portion of the western land to a third party i.e. Symbiosis. He submitted that as per 7/12 extract Symbiosis is now the recorded owner of that portion. He submitted that the assessee was not a party to the Symbiosis transaction. The assessee was not a confirming party and did not sign any NOC and received absolutely no consideration from that sale. He submitted that if the Revenue’s theory was correct that Rs.33 crores was only for the eastern portion, the assessee’s rights in the western portion would have remained intact and alive. Had that been the case, Ramsar Builder could not have sold the western portion to Symbiosis without the assessee’s involvement and the assessee would have certainly taken legal steps to injunct that sale or demand consideration. However, the fact that the assessee did nothing and that his name is completely absent from the recent 7/12 extract for the western portion proves beyond any doubt that all parties understood Rs.33 crores to be the final settlement for the assessee’s complete exit from the entire 35,600 sq. mtrs. He accordingly submitted that the Revenue has artificially bifurcated a composite settlement. The consideration of Rs.33 crores received by the assessee was the price for his total exit from all rights, claims and interests across the entire Survey No.230A/2 derived originally from 1989 development agreement. The assessee has completely moved out of the land. Therefore, the assessee is fully justified in law to claim the indexed cost of acquisition for the entire 35,600 sq.mtrs. and the Assessing Officer’s proportionate restriction is based on a misreading of the transaction. He accordingly submitted that since the Ld. CIT(A) / NFAC has deleted the addition by appreciating the facts properly, therefore, the grounds raised by the Revenue be dismissed.

14. He submitted that the documents must be read as a whole and not in isolation to avoid misinterpretation of the facts. He submitted that u/s 2(14) of the Act, “property of any kind” includes actionable claims, development rights and possessory rights. So far as the substantive rights over the entire 35,600 sq. mtrs are concerned which were judicially recognized and confirmed by the Civil Court vide order dated 30.06.2003 and has attained finality. He submitted that the 2013 civil suit No.408/2013 was instituted for specific performance of the 1989 agreement for the entire 35,600 sq. mtrs. and the alternative claim for damages (Rs.112.50 croes) was calculated on the developable potential of the whole land. He submitted that the assessee has not claimed the cost of the physical land. The assessee determined the fair market value of his intangible rights derived from the 1989 agreement and possession receipt as on 01.04.2001 and computed the indexed cost on that value. Therefore, the Revenue’s fear of an ‘absurd situation’ or double deduction is entirely baseless.

15. So far as the argument of the Ld. DR that the rights acquired by the assessee were limited and allowing the assessee complete deduction of cost of acquisition even in respect of smaller part of 13,967 sq. mtrs. may result in absurd situation wherein the vendor i.e. Lunkad Realty would also claim complete deduction of cost of acquisition in respect of smaller part is concerned, he submitted that this aspect has never been questioned by the Assessing Officer and the Ld. CIT-DR is raising this issue for the first time before the Tribunal. He submitted that the Ld. CIT-DR cannot improve the case of the Assessing Officer. In any case, he submitted that clause 8 of the 1989 agreement merely records the commercial rationale for the transaction that the Balgude family lacked the funds and technology to develop the land themselves. It does not limit the assessee’s rights. On the contrary, the 1989 agreement read with the Possession Receipt dated 10.04.1989 and the Irrevocable Power of Attorney granted the assessee the absolute possessory and development control over the entire 35,600 sq. mtrs. The assessee’s rights were substantive enough that he could successfully defend his possession in the Civil Court in 2003. The substantive rights over the entire parcel are what were ultimately surrendered in 2021 for Rs.33 crores. He submitted that the assessee in consideration of Rs.33 crores has given all his rights and interest on the entire larger land of 35,600 sq. mtrs. Once the parties contracting have decided so, the Revenue has no jurisdiction or authority to question the commercial understanding of what it believe are the true rights of the consenting parties. He submitted that the assessee has not acted upon or raised legal claims when part of the western portion of land was sold by Ramsar Builders. The understanding is clear because the assessee is no longer holding any rights or interest in respect of the entire larger land of 35,600 sq. mts. Further, the Revenue’s assumption that Lunkad Realty was only interested in clear encumbrances over the eastern portion is factually incorrect and ignores the history of the transaction. He accordingly submitted that the order of the Ld. CIT(A) be upheld and the appeal filed by the Revenue be dismissed.

16. We have heard the rival arguments made by both the sides, perused the orders of the Assessing Officer and Ld. CIT(A) / NFAC and the paper book filed on behalf of the assessee. We have also considered the various decisions cited before us. We find the Assessing Officer in the instant case made addition of Rs.20,28,10,757/- under the head ‘long term capital gain’ out of the total amount of Rs.33 crores received by the assessee by restricting the indexed cost of acquisition. According to the Assessing Officer the assessee has transferred his rights only on the area of 13967.50 sq.mtrs. out of the entire larger property admeasuring 35,600 sq.mtrs. He, therefore, worked out the indexed cost of acquisition in proportion to the area transferred. We find in appeal the Ld. CIT(A) / NFAC deleted the addition made by the Assessing Officer, the reasons of which have already been reproduced in the preceding paragraphs.

17. It is the submission of the Ld. DR that the capital asset transferred in this case vide Conveyance Deed dated 18.10.2022 by Lunkad Realty to Hotspot Realtors LLP was the land admeasuring 13967.50 sq.mtrs. According to him, both the Index-II and Schedule of property clearly mentions that the land transferred was admeasuring 13,967.5 sq mtrs at Survey No.230A/2. Therefore, in case of the assessee the full value of consideration received or accruing as a result of transfer of rights in the capital asset i.e. land admeasuring 13967.5 sq.mtrs. of land is the amount of Rs.33 crores. Out of this the assessee is entitled to get deduction towards cost of acquisition in relation to the asset transferred i.e. rights in land of 13967.5 sq.mtrs only. Further, it is his submission that as per clauses (f) and (g) of the Conveyance Deed, M/s. Lunkad Realty i.e. the vendor became the owner and possessor of the said land in Survey No.230A/2. As per the compromise deed dated 11.02.2022 the said larger land was partitioned and subdivided into Survey No.A/2 and A/2/1. The land in S.No.A/2 was owned by the legal heirs of one Late Balkrushna Ganpat Balgude and Survey No.A/2/1 was owned by Ali Asgar Dekhani. Para G clearly mentions that vide sale deeds dated 07.06.2014 and 10.06.2014 the vendor i.e. Lunkad Realty has purchased area admeasuring 13967.5 sq.mtrs out of the said larger land and in the mutation entry Nos.4077 and 0878, the name of the vendor is recorded as owner and possessor on 7/12 extract for Survey No.230A/2 for area admeasuring 13967.5 sq.mtrs. Therefore, the Ld. CIT(A) / NFAC failed to note that the capital asset transferred vide conveyance deed dt 18.10.2022 was smaller part admeasuring 13967.5 sq.mtrs. and not the larger land admeasuring 35,600 sq.mtrs. It is also his submission that the assessee was not the whole and sole owner of the transferred land admeasuring 13967.5 sq.mtrs. It had certain rights in the land created through various agreements and the assessee was merely a confirming party. Therefore, the Ld. CIT(A) / NFAC was not justified in allowing the assessee’s indexed cost of acquisition in relation to the larger land. It is also his submission that the development agreement dated 10.04.1989 submitted by the assessee is only in respect of the development rights of the land. Therefore, allowing the assessee complete deduction of cost of acquisition even in respect of smaller part may result in absurd situation wherein the vendor i.e. Lunkad Realty would also claim complete deduction of cost of acquisition in respect of smaller part i.e. 13967.5 sq.mtrs. It is the argument of the Ld. CIT-DR that the Ld. CIT(A) / NFAC completely failed to appreciate the importance of consent decree dated 04.08.2021 wherein para 11(a) clearly mentions that the assessee is surrendering his all rights, title and interest in S.No.A/2 admeasuring 13967.5 sq.mtrs. in lieu of payment of Rs.33 crores. It does not mention the rights in larger land admeasuring 35,600 sq.mtrs. It is his submission that the Ld. CIT(A) / NFAC without considering various terms and conditions of the consent decree and the development agreement has allowed full deduction of the cost of acquisition which is not justified.

18. It is the submission of the Ld. Counsel for the assessee that the consideration of Rs.33 crores was received as a lump sum, global settlement for the complete extinguishment and relinquishment of all his rights, title and interest in the entire larger property admeasuring 35,600 sq.mtrs., at Survey No.230A/2. Therefore, the assessee is entitled to the indexed cost of acquisition for the entire land of 35,600 sq.mtrs. It is his submission that this position is conclusively established by an independent and conjoint reading of the foundational documents, the court pleadings, the settlement terms and the subsequent conduct of the parties. It is his submission that the Consent Terms dated 03.08.2021 must be read as a whole to understand the true nature of Rs.33 crore consideration. According to him, it was not a payment for the eastern portion alone but a comprehensive buyout from the assessee of the entire property which is as per clauses (d), (e) and (h) of the Consent Terms dt 03.08.2021. Further, the conveyance deed dated 18.10.2022 especially clauses A, B, D and H expressly records the surrender of the larger land. It is also his submission that the practical and factual culmination of this global settlement is most evident in the subsequent fate of the western portion of the land. According to him, it is an undisputed fact that Ramsar builder subsequently sold a portion of the western land to a third party i.e. Symbiosis and it was recorded as owner of that portion as per 7/12 extract. The assessee was not a confirming party, did not sign any NOC and has not received any consideration from that sale. Therefore, if the Revenue’s theory were correct that Rs.33 crores was only for the eastern portion, then the assessee’s rights in the western portion would have remained intact and alive. Had that been the case, Ramsar Builder could not have sold the western portion to Symbiosis without the assessee’s involvement and the assessee would have certainly taken legal steps to injunct that sale or demand consideration. It is his submission that the Revenue has artificially bifurcated a composite settlement which is not correct and the assessee is fully justified in law to claim the indexed cost of acquisition for the entire 35,600 sq.mtrs. According to him, the Assessing Officer’s proportionate restriction is based on a misreading of the transaction. It is also his submission that the Ld. CIT-DR cannot travel beyond the factual findings given by the Assessing Officer.

19. We find sufficient force in the above arguments of the Ld. Counsel for the assessee. There is no dispute to the fact that what was sold by M/s. Lunkad Reality to M/s. Highspot Realtors LLP was land admeasuring 13,975 sq. mtrs. The fundamental error in the Revenue’s approach in our opinion is not appreciating the fact that what the assessee has surrendered is his right, title and interest in the entire land parcel admeasuring 35,600 sq. mtrs. documented in various clauses of the conveyance deed dated 18-10-2022. We find clause ‘A’ of the conveyance deed read as under:

“A. The Vendor and Confirming Party herein state that, all that property bearing Survey No.230 A/2 admeasuring 08 Acre 32 Gunthas i.e. 03 Hectare 56 Ares, situated at Village Lohegaon within the Registration District Pune, SubRegistration District Haveli, Taluka Haveli and within the limits of Pune Municipal Corporation is hereinafter referred as ‘Said Larger Land’, was owned & possessed by Tukaram Genu Devkar and who gifted the same to his two grandsons viz. Eknath Ganpat Balgude and Balkrishna Ganpat Balgude by Gift Deed dated 14/11/1931 registered in the office of Sub-Registrar Haveli No.1 at Serial No. 2606/1931.”

20. Similarly clause ‘H’ of the conveyance deed reads as under:

“H. The Confirming Party is claiming that, it has rights, title and interest in the Said Larger Land and filed SCS No.408/2013 in the Court of Hon’ble Civil Judge Senior Division against the Balgude family, Vendor, Ramsar Builders, Promoters and Developers and others, praying for specific performance of the Development Agreement dated 10/04/1989 and execution of final Conveyance Deed and other consequential reliefs as claimed in the plaint. Considering the pending suit for long time and rival claims of Vendor & Confirming Party against each other, in the presence of respected elderly people in family of both the Vendor & Confirming Party herein decided to arrive at settlement in aforesaid pending suit and after negotiation at length, the Vendor and Confirming Party have mutually reached a settlement by filing Consent Terms dated 03/08/2021 in the aforesaid suit and have mutually agreed that Confirming Party is surrendering all right, title and interest with delivery of possession in favour of the Vendor for consideration of Rs.33,00,00,000/- (Rupees Thirty Three Crores) only. In pursuance of aforesaid Consent Terms, Cancellation Deed dated 04/08/2021 registered in the office of Sub-Registrar Haveli No.23 at Serial No. 14075/2021 has been executed between the Vendor and Confirming Party whereby registered Joint Venture dated 09/11/2005 between them, which was for part of the Said Larger Land, has been cancelled. The Vendor has paid Rs.1,00,00,000/- (Rupees One Crore Only) to the Confirming Party by RTGS No.HDFCR52021080657299597 for amount of Rs.50,00,000/- (Fifty Lakhs Only) on 06/08/2021 and by RTGS No.HDFCR52021080657236596 for amount of Rs.50,00,000/- (Fifty Lakhs Only) on 06/08/2021 and balance amount of Rs.32,00,00,000/- (Rupees Thirty Two Crores only) remains to be paid. All right, title and interest of the Confirming Party with delivery of possession, as received/obtained by the Confirming Party is handed over to the Vendor as per Consent Terms.”

21. Therefore, the assumption that the Assessee transferred rights only in land admeasuring 13,967.5 sq. mtrs. in our opinion is contrary to the documentary evidence on record.

22. We find merit in the argument of the Ld. Counsel for the assessee that the Assessee’s rights stemmed from the Development Agreement dated 10.04.1989, which unequivocally covered the entire 35,600 sq. mtrs. The Civil Suit (SCS No. 408/2013) instituted by the Assessee was for the specific performance of this 1989 Agreement in its entirety, covering the whole 35,600 sq. mtrs., and the alternative claim for damages (112.50 Crores) was calculated on the developable potential of the entire land. A conjoint reading of the Consent Terms dated 03.08.2021 and the Conveyance Deed dated 18.10.2022 clearly establishes that the assessee relinquished all his rights in the entire land parcel admeasuring 35,600 sq. mtrs., and not merely a portion thereof. In our opinion, the ?33 crores received by the Assessee was a lump-sum, global settlement for extinguishing his entire bundle of rights, claims, and litigation across the whole 35,600 sq. mtrs. The Assessee exited the entire project, and therefore, the cost of acquisition referable to his rights in the entire 35,600 sq. mtrs. is fully deductible. We find force in the argument of the Ld. Counsel for the assessee that the documents must be read conjointly and not in isolation to avoid misinterpretations of the facts.

23. We find Clause 11(e) of the Consent Terms (Page No. 177 of the paper Book) records the admission by the vendor (i.e. M/s Lunkad Realty) of the existence of original 1989 Development Agreement and possession receipt in respect of the said land admeasuring 35,600 sq.mtr. This establishes that the Assessee derived and held possession over the entire land admeasuring 35,600 sq. mtrs. from the original owners, and not merely a portion thereof. Thus, it is well established that the Assessee’s rights extends to the whole property admeasuring 35,600 sq. mtrs. For clarification the said clause is reproduced which reads as under:

“e. The Agreement dated 10.04.1989 and the Possession Receipt dated 10.04.1989 stands admitted today by M/s Lunkad Realty and the possession derived by the Plaintiff from the Balgude family under the said documents is handed over to M/s. Lunkad Realty today which is peaceful on the following terms and conditions.”

24. We further find clause ‘A’ of the Conveyance Deed dated 18.10.2022, wherein the Assessee is a Confirming Party defines the “Said Larger Land” as admeasuring 08 Acre 32 Gunthas, equivalent to 35,600 sq. mtrs., thereby clearly identifying the entire land as the subject matter of the transaction. For clarification we reproduce clause ‘A’ of the conveyance deed which reads as under:

“A. The Vendor and Confirming Party herein state that, all that property bearing Survey No.230 A/2 admeasuring 08 Acre 32 Gunthas i.e. 03 Hectare 56 Ares, situated at Village Lohegaon within the Registration District Pune, SubRegistration District Haveli, Taluka Haveli and within the limits of Pune Municipal Corporation is hereinafter referred as ‘Said Larger Land’, was owned & possessed by Tukaram Genu Devkar and who gifted the same to his two grandsons viz. Eknath Ganpat Balgude and Balkrishna Ganpat Balgude by Gift Deed dated 14/11/1931 registered in the office of Sub-Registrar Haveli No.1 at Serial No. 2606/1931.”

25. Similarly, clause D of the Conveyance Deed records the cancellation of the earlier Joint Venture Agreement dated 2005, which pertained to development rights in respect of the western part. This evidences that all rights of the Assessee in the western part beside the eastern part stood extinguished. For clarification, we reproduce clause ‘D’ of the conveyance deed which reads as under:

“D. The Vendor and Confirming Party entered into a Joint Venture Agreement dated 09/11/2005 registered in the office of Sub-Registrar Haveli No.7 at Serial No.1540/2006 for development of area admeasuring 1,50,000 sq.ft out of the Said Larger Land and which Joint Venture Agreement dated 09/11/2005 is duly cancelled as stated in Para H hereunder written.”

26. Further clause H of the Conveyance Deed categorically provides that the Assessee has surrendered and relinquished all rights and possession in respect of the Said Larger Land in consideration of ?33 crore. The language of this clause leaves no ambiguity that the consideration was for the extinguishment of rights in the entire land parcel and not a part thereof. For more clarity, we reproduce clause ‘H’ of the conveyance deed which reads as under:

“H. The Confirming Party is claiming that, it has rights, title and interest in the Said Larger Land and filed SCS No.408/2013 in the Court of Hon’ble Civil Judge Senior Division against the Balgude family, Vendor, Ramsar Builders, Promoters and Developers and others, praying for specific performance of the Development Agreement dated 10/04/1989 and execution of final Conveyance Deed and other consequential reliefs as claimed in the plaint. Considering the pending suit for long time and rival claims of Vendor & Confirming Party against each other, in the presence of respected elderly people in family of both the Vendor & Confirming Party herein decided to arrive at settlement in aforesaid pending suit and after negotiation at length, the Vendor and Confirming Party have mutually reached a settlement by filing Consent Terms dated 03/08/2021 in the aforesaid suit and have mutually agreed that Confirming Party is surrendering all right, title and interest with delivery of possession in favour of the Vendor for consideration of Rs.33,00,00,000/- (Rupees Thirty Three Crores) only. In pursuance of aforesaid Consent Terms, Cancellation Deed dated 04/08/2021 registered in the office of Sub-Registrar Haveli No.23 at Serial No. 14075/2021 has been executed between the Vendor and Confirming Party whereby registered Joint Venture dated 09/11/2005 between them, which was for part of the Said Larger Land, has been cancelled. The Vendor has paid Rs.1,00,00,000/- (Rupees One Crore Only) to the Confirming Party by RTGS No.HDFCR52021080657299597 for amount of Rs.50,00,000/- (Fifty Lakhs Only) on 06/08/2021 and by RTGS No.HDFCR52021080657236596 for amount of Rs.50,00,000/- (Fifty Lakhs Only) on 06/08/2021 and balance amount of Rs.32,00,00,000/-(Rupees Thirty Two Crores only) remains to be paid. All right, title and interest of the Confirming Party with delivery of possession, as received/obtained by the Confirming Party is handed over to the Vendor as per Consent Terms.”

27. In view of the above, we find merit in the argument of the Ld. Counsel for the assessee that the consideration of ?33 crore was received for the transfer, by way of extinguishment, of the assessee’s rights in the entire land admeasuring 35,600 sq. mtrs., which constitutes a “transfer” within the meaning of Section 2(47) of the Act. The Ld. CIT(A), having appreciated the documents in their entirety and in proper perspective in our opinion has rightly allowed the claim of the assessee.

28. So far as the argument of the Revenue that only absolute ownership of physical land constitutes a “capital asset” in our opinion proceeds on the legally flawed premise. Under section 2(14) of the Act, “property of any kind” includes actionable claims, development rights, and possessory rights. The Assessee’s substantive rights over the entire 35,600 sq. mtrs. were judicially recognized and confirmed by the Civil Court vide order dated 30.06.2003, which has attained finality. We find the 2013 Civil Suit (SCS No. 408/2013) was instituted for the specific performance of the 1989 Agreement for the entire 35,600 sq. mtrs., and the alternative claim for damages (112.50 Crores) was calculated on the developable potential of the whole land.

29. We further find, the assessee in the instant case has not claimed the cost of the physical land. The Assessee determined the Fair Market Value (FMV) of his intangible rights (derived from the 1989 Agreement and Possession Receipt) as of 01.04.2001, and computed the indexed cost on that value. Therefore, the Ld. CIR-DR’s argument of an “absurd situation” or double deduction in our opinion is entirely baseless. Lunkad Realty will claim the cost of the physical land it owned and sold; the Assessee is claiming the indexed cost of his distinct, independent capital asset after extinguishing his rights over the 35,600 sq. mtrs. The Assessee being a “Confirming Party” in the 2022 Deed precisely proves that his pre-existing rights over the larger land had to be legally extinguished for Lunkad to pass a clear title. We further find this aspect has never been questioned by the Assessing Officer and this has been raised for the first time before the Tribunal. In our opinion, the Ld. CIR-DR cannot travel beyond the factual findings of the Assessing Officer. We further find the 1989 Agreement, read with the Possession Receipt dated 10.04.1989 and the Irrevocable Power of Attorney has granted the Assessee absolute possessory and development control over the entire 35,600 sq. mtrs. The Assessee’s rights were substantive enough that he could successfully defend his possession in the Civil Court in 2003. These substantive rights over the entire parcel are what were ultimately surrendered in 2021 for ?33 crores. We find merit in the argument of the Ld. Counsel for the assessee that reading Clause 11(a) in isolation is fatal to the true interpretation of the Consent Terms. The document must be read as a whole. We find clause 11(d) explicitly states that “All rival claims of the Plaintiff in this suit. stands dissolved/relinquished”. Therefore, the suit was for the entire 35,600 sq. mtrs.

30. Further, clause 11(e) records Lunkad Realty’s admission of the 1989 Agreement and Possession Receipt (which covered the entire 35,600 sq. mtrs.) and confirms that the possession derived thereunder is handed over.

31. Similarly, as per clause 11(h), the 2005 JV Agreement itself proves Lunkad’s involvement in the entire land. In 2005, Lunkad entered into a JV with the Assessee for the Western portion. In 2006, Lunkad dealt directly with the owners for the Eastern portion. Lunkad was deeply entangled in the entire 35,600 sq. mtrs. The ?33 crores was the price demanded by the Assessee to walk away from the entire property and drop the 2013 suit, allowing Lunkad to monetize whatever portions it held. Clause 11(h) Explicitly cancels the 2005 JV Agreement for the Western portion. This clause was necessary to nullify the Assessee’s lucrative entitlements under that JV (30% profits, 1 Crore, and a 1500 sq. ft. flat).

32. The submission of the assessee that Ramsar Builders subsequently sold a portion of this Western land to a third party, Symbiosis, who is presently the recorded owner of that portion as evidenced by the recent 7/12 extract and when Ramsar sold that land to Symbiosis, the Assessee was not involved in the transaction, received no consideration, and was not a confirming party could not be controverted by the Ld. DR. We, therefore, find merit in the argument of the Ld. Counsel for the assessee that if the assessee had retained any subsisting, enforceable rights in the Western portion after the 2021 Consent Terms, he would have undoubtedly taken legal steps to block the Symbiosis transaction or demanded consideration.

33. We, therefore, find force in the argument of the Ld. Counsel for the assessee that the assessee, in consideration of Rs. 33 crores, has given up his all his rights and interest in the entire larger land of 35,600 sq. mtrs. Once parties contracting have decided so, the Revenue has no jurisdiction or authority to question the commercial understand of what it believe are the true rights of the consenting parties. The T33 crores was the only consideration flowing to the assessee for this entire global settlement, which included the cancellation of his JV rights over the Western portion.

34. In this view of the matter and in view of the detailed reasonings given by the Ld. CIT(A) / NFAC, we do not find any infirmity in his order. Accordingly, the same is upheld and the grounds raised by the Revenue are dismissed.

35. In the result, the appeal filed by the Revenue is dismissed.