ORDER

T.R. Senthil Kumar, Judicial Member.- These cross appeals are filed by the Assessee and Revenue as against the common appellate order dated 19-07-2024 passed by the Commissioner of Income Tax (Appeals)-11, Ahmedabad, arising out of separate assessment orders passed under section 153A rws 143(3) of the Income Tax Act, 1961 (hereinafter referred to as ‘the Act’) relating to the respective Assessment Years 2018-19 and 2019-20. Since common issues of disallowances are involved in all these appeals, for the sake convenience the same are disposed of by this common order.

2. Brief facts of the case are as such that search action under section 132 of the Act in the case of Riddhi Siddhi Groups on 0102-2019 in which the assessee was also covered. The facts which came to light from the search action on Riddhi Siddhi Group was that the assessee/Dhaval N. Patel was found to be the most trusted person of the Riddhi Siddhi group. At the time of search action, the assessee was present at the corporate office, his wife Smt. Vaishali D. Patel is also one of the director of Riddhi Siddhi Gluco Biols Ltd., flagship company of Riddhi Siddhi Group. From the evidences seized, the assessee was found to be handling the unaccounted cash transactions of Riddhi Siddhi Group. Plethora of such evidences were seized from his mobile phone which proved that these incriminating evidences are related to various entities of the Riddhi Siddhi Group and they have been discussed in respective assessment orders of various entities of Riddhi Siddhi Group. Further, the assessee vide his reply dated 25-07-2019 has categorically submitted that he is just a custodian of unaccounted cash and accounts of Shri Siddharth G. Chowdhary and Riddhi Siddhi Group.

2.1. Apart from the above facts, the importance of the assessee to Riddhi Siddhi Group can also be gauged from the fact that the impugned unaccounted cash of Rs.4,44,96,000/- found and seized from the corporate office of Riddhi Siddhi Group was found in the possession of the assessee, who had come to the corporate office and was carrying such unaccounted cash with him which belonged to the Group. Considering the above facts, notice section 153A was issued on 15.11.2019. In response, the assessee filed his return of income on 13.12.2019 declaring total income at Rs. 9,55,580/-. Assessments were completed for the asst years 2018-19 by making following disallowances:

| Asst Year |

Date |

Nature of disallowance |

Amount |

| 2018-19 |

28-07-2021 |

Unexplained unsecured loan u/s.68 of the Act

Unexplained investment

Unexplained Advance

Interest income

Credits in bank account

Addition on a/c of Whatsapp chat

Unexplained transaction |

48,00,000

1,00,00,000

3,22,00,000

29,05,855

1,452

50,00,000

6,01,60,800 |

3. Aggrieved against the assessment order the assessee filed appeals before Ld CIT[A], who by common order dated 19-072024 confirmed few additions/disallowances and deleted few additions. Let us first deal with each issue relating to the Asst. Year 2018-19.

3.1. The AO has made addition on account of Unexplained Unsecured Loans obtained in lieu of Promissory Notes. The AO has made addition based on images of various promissory notes totaling to Rs.48,00,000/- found from the mobile of the assessee. The Ld AO held that the assessee has received unaccounted cash loan of Rs.48,00,000/- based on the images of various promissory notes and the assessee is unable to identify the persons from whom cash loan is received. Therefore, the Ld AO concluded that the promissory notes represent unaccounted cash receipt of the assessee and provisions of Section 68 of the Act are applicable in this case since the assessee failed in discharge the burden cast upon him u/s. 68 of the Act.

3.2. On appeal before Ld CIT[A], who has considered the submissions of the assessee and deleted the addition by observing as follows:

“… 32.3. I have perused the submissions of the appellant and the contentions of the AO. It is seen from the assessment order that there is no corroborative evidence on record to prove that cash loans have been received against the said promissory notes. There is no other evidence found and placed on record to establish that cash loans have actually been received by the appellant. On perusal of the images found from the mobile of the appellant, it is evident that there is no name mentioned of the lender on any of the promissory notes nor any other details are filled up. Even there is no strike off on cash/cheque. The promissory notes might have been made by the appellant to obtain loans but the AO has not been able to establish whether actual loans were received against these promissory notes or not. The copy of said promissory note is reproduced as under:-

32.4 The provisions of The Negotiable Instruments Act relating to validity of a promissory note require attention and it is clear that the promissory notes found are not validly issued as per these provisions and the promissory notes found are incomplete and inconclusive.

32.5 In view of the above discussion, the addition of Rs. 48,00,000/- made by the AO is hereby deleted. Thus, the grounds of appeal no. 2 to 4 are allowed.

33.1 The AO has made addition of Rs 1,00,00,000/- in the case of the appellant on account of Unexplained Investment in Land based on an image found from the mobile of the appellant. The AO has stated that based on the image and on plain reading of the lower part image, it is clearly mentioned that token of Rs.1,00,00,000/- has been paid. The AO also found out that the said property is under litigation. However, the AO stated that Rs. 1,00,00,000/- has been paid as a token on or before the date of MoU which is dated 26/08/2017 relevant to A.Y.2018-2019. The AO contended that the appellant has not given any details of the parties to the MoU. The image is found from the mobile phone of the appellant and hence he is bound to furnish necessary evidence in support of his submissions. The AO has referred to the provisions of Section 132(4A) of the Income Tax Act and made addition to the income of the appellant.

33.4 I have considered the submissions made by the appellant and the contentions of the AO. On perusal of the assessment order, it is observed that the appellant is neither the buyer nor the seller for the said property. The said fact has been confirmed by the AO himself wherein he has verified the details of the owners from the government website. The AO has also verified that the property is still under litigation and in the name of the original land owners, which establishes the fact that the deal for the said property never took place.

33.5 As regards the token payment of Rs.1,00,00,000/-there is no corroborative evidence but the preliminary reading of the image indicates that the same has been paid. However, the fact remains that the appellant has acted as a broker in the said deal and is neither the purchaser nor the seller. Therefore, even if the deal was finalized the amount of Rs. 1 crore could not be treated as the income of the appellant. However, the appellant has admitted that he has acted as a broker for the aforesaid deal and therefore what can be added to the income of the appellant is the brokerage on the said deal.

33.6 It is observed from the facts on record that the appellant is not acting only as a broker but he is also providing various ancillary services like approaching the solicitors, following up with the procedures, acting as a custodian wherever required. Therefore, the appellant cannot be said to have earned mere brokerage like other brokers who act only as a broker. Considering the totality of the facts of the case and the services provided by the appellant, addition of brokerage @5% would meet the ends of justice.

33.7 In view of the above discussion, the addition of Rs.5,00,000/- is confirmed in the case of the appellant towards brokerage and the balance addition of Rs.95,00,000/- is hereby deleted. Since acting as a broker is the main business activity of the appellant, the income is required to be taxed u/s 28 of the Act and therefore the provisions of section 115BBE will not be applicable to the addition of Rs.5,00,000/-confirmed in the appellant’s case. Thus, the ground of appeal no. 5 to 7 are partly allowed.”

4. The next addition of Rs.3,49,05,858/- (2,72,00,000 + 29,05,858 + 50,00,000) on account of undisclosed income based on two images found from the mobile of the assessee. On appeal Ld CIT[A] deleted the above additions by observing as follows:

“… 34.2.5. I have carefully considered the contentions of the AO and the submissions made by the appellant. On perusal of the image, it can be observed that the nature of transaction is not mentioned anywhere. However, dates of repayment and calculation of interest on reducing balance is made in the said image which would indicate that the transactions relate to loan transactions and interest thereon. It cannot be established whether the page represents notings for loans taken or given or investments or any other use. Further, the AO’ has assumed the details to be relevant for the current assessment year. On perusal of the image, it is seen that there is no year written to conclude that the image is relevant for the current assessment year.

However, the appellant has in his submissions before the AO stated that these are loans given by him and interest income thereon is offered by the appellant in the Revised Computation of Income for A.Y.2019-20. Also, no evidence is again brought on record to establish that such transactions are undertaken in F.Y.2017-18 relevant to A.Y.2018-19. On a plain reading of the image, it is seen that the amount of Rs. 2,72,00,000/- is written as opening balance as on 1st April. Further, the AO and appellant both have submitted that these are loan transactions. Therefore, the same cannot be added in the appellant’s case in the absence of any corroborative material or evidence that the same represented income of the appellant for the current year.

34.2.6 However, the addition of interest of Rs.29,05,858/- is confirmed in the appellant’s case as the appellant has offered the interest income for taxation on his own. The appellant has not provided any evidence or explanation as to why the said interest income is offered in A.Y.2019-20 and therefore in the absence of any such details from the appellant, the addition of Rs.29,05,858/- is confirmed in the year under consideration.

34.3.3 I have considered the submissions made by the appellant and the order passed by the AO. The issue involved in this addition is more or less similar to the addition discussed in the preceding paragraph. On perusal of the image, it is seen that the nature of transaction is not mentioned as to whether it represents loans taken or given. The AO has assumed the details to be relevant for the current assessment year without any basis since no dates or year are written in the image.

34.3.4 Further, if the contentions of the AO are believed and the loan confirmation for cheque transaction submitted by the appellant is perused, it is seen that the appellant has given the loan by cheque. As a corollary, the cash noted in the image would be cash received by the appellant and not paid as contended by the AO. Even in such circumstances, addition cannot be made in the appellant’s case since the appellant is the recipient of cash and therefore the source of the same cannot be added in the appellant’s case. Considering the totality of the facts, the addition of Rs.50,00,000/- is hereby deleted.”

5. The next addition of an amount of Rs.50,00,000/- on account of undisclosed income based on WhatsApp chat found from the mobile of the assessee. The AO has made an addition on the basis of an outgoing message found from the mobile of the assessee

1) Direction: Outgoing Deleted: No Type: WhatsApp message Time stamp

(Device time +00:00): 11-12-2017 04:35:37 Remote party: 919998612120 Text/Description: “50 lacks given to Manan yesterday”

From: 919825822225 To: 919998612120

Details Data source: WhatsApp Google Backup ID: 284485

Remote party: 919998612120

Type: Text Created (Device time +00:00): 11-12-2017 04:35:37

Received by server (Device time +00:00): 11-12-2017 04:35:38

Delivered (Device time +00:00): 11-12-17

5.1. The assessee submitted before the AO that the WhatsApp chat referred to cheque of Rs.50 lacs given to Shri Manan K. Trivedi and submitted ledger of Shri Manan K. Trivedi. The Ld AO observed that as per the confirmation, there was an opening balance of Rs.37,00,000/- as on 01.04.2017 and there were no transactions of Rs.50,00,000/- during the year under consider ation. The AO held that on verification of the WhatsApp chat it was clear that the transaction amounting to Rs.50,00,000/- has been carried out on 10.12.2017. The AO stated that the date of transaction is clear from the description of the message and there is no such transaction of Rs.50,00,000/- in the confirmation submitted by the assessee. Therefore, the AO held that the transaction mentioned in the WhatsApp chat amounting to Rs.50,00,000/- is not accounted for and added the same to the Total Income of the assessee.

5.2. On appeal before Ld CIT[A] considered the above submission and confirmed the addition made by the AO by observing as follows:

“… 35.4 I have considered submissions made by the appellant and the contentions of the AO. On a plain reading of the WhatsApp message, it can be concluded that the appellant has paid an amount of Rs.50,00,000/- to Mr. Manan and there is no ambiguity regarding the same. The appellant has not been able to substantiate that the transaction was done through cheque. Therefore, it is evident that cash payment is made by the appellant. Hence, the addition of Rs.50,00,000/-made by the AO is hereby upheld, hence confirmed. Thus, the grounds of appeal no. 13 & 14 are dismissed.”

6. Next addition of Rs.6,01,60,800/- (5,50,00,000/- + 51,60,800/-) as unaccounted transaction on the basis of image found from the mobile phone of the assessee. The image contained transaction of Rs.17 crore out of which Rs.11.50 crore is in cheque and balance Rs.5.5 crore is added by the AO as unexplained cash transaction. Also, a noting relating to interest of Rs.51,60,800/- was also added by the AO to the Total Income of the assessee.

6.1. On appeal before Ld CIT[A] considered the above submission and deleted the above addition by observing as follows:

“… 36.6 I have considered the contentions of the AO and the submissions made by the appellant. The appeal in the case of Shri Prakash M. Sanghvi is decided by the undersigned and an order dated 28.03.2024 has been passed in his case. The additions made on the basis of entries appearing in the seized diaries of Shri Prakash M. Sanghvi has already been dealt with and decided by the undersigned and addition with respect to various sources of income has already been confirmed in the case of Shri Prakash M. Sanghvi. Thus, the addition on account of the source of payments recorded in the said image has already been confirmed by the undersigned while passing appellate orders in the case of Shri Prakash M. Sanghvi. If the addition is also confirmed in the case of the appellant, the same would amount to double taxation of the same income. Following the rule of consistency, the addition for source of funds for payments noted in the image which are also recorded in the seized diaries, as being already confirmed in the hands of Shri Prakash M. Sanghvi, is required to be deleted in the appellant’s case.

36.7 Thus, the addition on account of Unexplained transaction is hereby deleted in the case of the appellant. Also, the interest is not recorded by Prakash M. Sanghvi and the addition on account of notional interest is also adjudicated by the undersigned in the case of Shri Prakash M. Sanghvi. Following the rule of consistency, the addition on account of such notional interest is deleted in the appellant’s case also. Thus, the grounds of appeal no. 16 to 18 are allowed.

7. Aggrieved against the appellate order, Assessee is in appeal before us raising the following Grounds of Appeal in IT(SS)A No. 63/Ahd/2024 for A.Y. 2018-19:

| 1. |

|

The learned CIT(A) has erred in not holding that the notice issued u/s. 153A of the Act is bad in law, illegal and void-ab-initio. The learned CIT (A) has erred in not holding that the assessment order passed by AO u/s. 153A r.w.s. 143(3) of the Act is bad in law, illegal and null and void. |

| 2. |

|

The learned CIT(A) has erred in confirming the additions made by AO in the Appellant’s case and rejecting the submissions that the noting in the image donot pertain to/belong to the Appellant. |

| 3. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 5,00,000/- on account of brokerage. |

| 4. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 29,05,858/-on account of Interest earned on Unexplained advances. The learned CIT(A) has erred in confirming the action of the AO in invoking s. 115BE in respect of the said addition. |

| 5. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 50,00,000/-on as unaccounted transaction account of Interest earned on Unexplained advances. The learned CIT(A) has erred in confirming the action of the AO in invoking s. 115BE in respect of the said addition. |

| 6 |

|

The Appellant states that the search proceedings carried out in his case are beyond jurisdiction, illegal and void. The consequential assessment order passed is bad-in-law, illegal and void-ab-initio. |

| 7. |

|

The learned CIT(A) has erred in not holding that the assessment order passed by AO is in gross violation of principles of natural justice. |

| 8. |

|

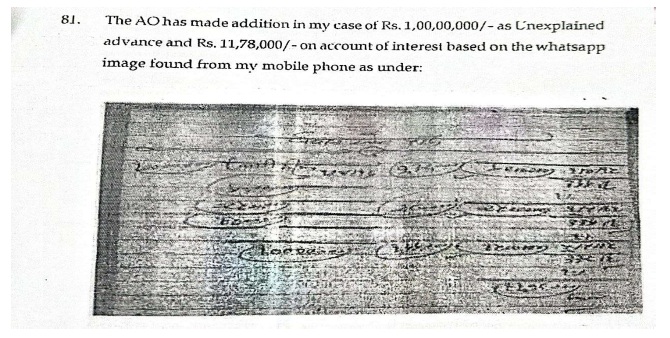

The Appellant craves leave to add, amend and/ or alter the ground or grounds of appeal either before or at the time of hearing of the appeal. |

8. Aggrieved against the appellate order, Revenue is in appeal before us raising the following Grounds of Appeal in IT(SS)A No. 77/Ahd/2024 for A.Y. 2018-19:

| 1) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of Rs.48,00,000/ on account of Unexplained Unsecured Loan in lieu of Promissory Notes without appreciating the facts that during the course of search action, statement of the assessee was recorded and while recording the statement of Shri Dhaval N. Patel, he categorically accepted that these are forged documents, created and signed by him with an intention to carry out financial fraud by accepting loans/advances from parties.” |

| 2) |

|

“In the facts and on the circumstances of the case and in law, the ld. CIT(A) has erred in deleting the addition of Rs.95,00,000/ on account of unexplained investment in land without appreciating the facts that during the post search inquiry, the assessee failed to give details of the parties involved in the said land deal and considering the assessee as broker in the land deal without mentioning any cogent proof |

| 3) |

|

“In the facts and on the circumstances of the case and in law, the ld CIT(A) has erred in deleting the addition of Rs.3,22,00,000/ on account of unexplained advance without appreciating the facts that during the post search proceedings, the assessee himself accepted that the transactions are unaccounted and he earned interest of Rs. 29,05,858/as well.” |

| 4) |

|

“In the facts and on the circumstances of the case and in law, the ld. CIT(A) has erred in deleting the addition of Rs.6,01,60,800/- on account of unaccounted Income as per whatsapp chats extracted from the mobile phone of Dhaval N. Patel simply relying upon the submission of the assessee and without any verification of the said transaction from the seized diary in the case of Prakash M Sanghvi” |

| 5) |

|

“The Revenue craves leave to add/alter/armed and/or substitute any or all of the grounds of appeal. |

9. Heard rival submissions at length and we first deal with assessee appeal. Ld AR Shri Vijay Mehta appearing for the assessee submitted that the assessee is NOT Pressing Ground Nos.1, 2, 4, 6, 7 & 8 on the jurisdiction of assessment and other issues, recording the same Ground Nos. 1, 2, 4, 6, 7 & 8 are dismissed.

9.1. Ground No.3 is inter-connected with Ground No.2 filed by the Revenue, hence the same will be dealt in Revenue appeal.

10. Remaining only Ground No.5 is Ld CIT(A) erred in confirming the addition of Rs.50 lakhs as unaccounted income of the assessee. Ld AR appearing for the assessee submitted that the assessee duly explained before the Ld AO that he had given cheque of Rs.50 lakhs to Manan Trivedi, however the same not deposited by him. Therefore, the WhatsApp chat do not mention whether the amount is paid in cash or cheque. Further, there were no other WhatsApp chat confirming receipt or payment was found in the mobile phone of the assessee except “50 lacs given to Manan yesterday”. The assessee also provided PAN and address of Manan Trivedi before the Ld AO. But, the AO simply presumed the same to be cash payment and without making any further enquiry confirmed the addition, which is confirmed by the Ld CIT[A] and therefore requested to delete the addition.

11. Ld Sr-DR, Shri Nitin Kulkarni appearing for the Revenue supported the orders passed by the Lower Authorities and requested to confirm the addition made on account of unaccounted income.

12. We have carefully considered the rival submissions and perused the materials available on record. The impugned addition of Rs.50 lakhs has been made solely on the basis of a WhatsApp message found in the mobile phone of the assessee stating that “50 lacks given to Manan yesterday”. The Ld AO presumed that the said transaction represented an unaccounted cash payment made by the assessee to Shri Manan Trivedi and accordingly treated the same as undisclosed income of the assessee. The Ld. CIT(A) also confirmed the addition primarily on the basis of the wording contained in the message. However, on a careful appreciation of facts, we find that the conclusion drawn by the lower authorities is not supported by any corroborative materials. The WhatsApp message merely mentions that Rs.50 lakhs were “given” to Manan. The message nowhere states that the amount was paid in cash. In absence of any specific reference to cash payment, the authorities below were not justified in presuming that the transaction represented unaccounted cash outflow. It is a settled proposition that suspicion, however strong, cannot take the place of evidence.

12.1. Further the assessee, from the very beginning, consistently explained that the message pertained to cheque transactions with Shri Manan K. Trivedi. The assessee had also furnished the ledger account, PAN and address details of Shri Manan Trivedi before the Ld AO. Once such primary explanation and identity details were furnished, the burden shifted upon to the AO to conduct further verification or enquiry from Shri Manan Trivedi. However, perusal of assessment order shows that no such independent enquiry was carried out by the Ld AO. No statement of Shri Manan Trivedi was recorded. No evidence was brought on record to establish that any cash was actually paid by the assessee. Further, no incriminating material such as cash withdrawal, cash availability, diary entry, receipt, acknowled gement or corresponding evidence from the recipient side has been brought on record to corroborate the allegation of unaccounted cash payment. Further the WhatsApp chat clearly mention the other Cell no namely “9825822225” but the AO has not verified with that cell number.

12.2. It is further noted that the addition has been made merely because the exact entry of Rs.50 lakhs was not reflected in the ledger account during the relevant period. However, such discrepancy by itself cannot automatically lead to the conclusion that the transaction represented undisclosed income of the assessee, particularly when the Revenue has failed to establish the nature and character of the alleged payment with cogent evidences. Further, the WhatsApp message, in isolation and without any corroborative material, cannot be treated as conclusive evidence for making addition of Rs.50 lakhs. Electronic communication may at best create a doubt requiring further investigation, but addition cannot be sustained merely on assumptions and presumptions. The Revenue has failed to discharge the burden of proving that the impugned amount represented unexplained or undisclosed income of the assessee. Accordingly, in the absence of any corroborative evidence establishing actual cash payment by the assessee, we hold that the addition of Rs. 50 lakhs made by the AO and sustained by the Ld. CIT(A) is unsustainable in law. The same is therefore directed to be deleted. Thus, the ground no.5 raised by the assessee is hereby allowed.

13. In the result, the appeal filed by the assessee in IT[SS]A No. 63/Ahd/20224 is partly allowed.

14. Now we deal with Revenue appeal. Ground No.1 is CIT(A) has erred in deleting the addition of Rs.48,00,000/ on account of Unexplained Unsecured Loan in lieu of Promissory Notes. During the course of search proceedings, certain images of promissory notes were found in the mobile phone of the assessee. Based on such images, the Ld AO concluded that the assessee had obtained unaccounted cash loans aggregating to Rs.48,00,000/-. According to the AO, the assessee failed to identify the persons from whom such loans were allegedly received and therefore the provisions of section 68 of the Act were attracted. Consequently, the AO treated the amount of Rs.48 Lakhs as unexplained cash credit and added the same to the income of the assessee. On appeal, the Ld. CIT(A) deleted the addition after examining the contents of the promissory notes and observing that there was no corroborative evidence to establish actual receipt of cash loans by the assessee. Aggrieved by the relief granted by the Ld. CIT(A), the Revenue is in appeal before the Tribunal.

14.1. The Ld Sr-DR, Shri Nitin Kulkarni appearing for the Revenue relied upon the assessment order and submitted that the images of promissory notes clearly established that the assessee had entered into loan transactions outside the books of account. It was contended that the assessee failed to explain the nature and source of such transactions and therefore the AO was justified in making addition u/s.68 of the Act.

15. Per contra, the Ld AR Shri Vijay Mehta appearing for the assessee supported the order of the Ld. CIT(A) and submitted that the entire addition was made merely on the basis of incomplete images found in the mobile phone without any corroborative evidence. It was submitted that no lender was identified in the promissory notes, no actual cash movement was established and no enquiry was conducted by the AO to prove receipt of any unaccounted loan. Therefore, it was argued that the addition was rightly deleted by the Ld. CIT(A).

16. We have considered the rival submissions and perused the material available on record. The sole basis for making the impugned addition is the images of certain promissory notes found in the mobile phone of the assessee. However, on perusal of the copies of such promissory notes, it is evident that the documents are incomplete and do not conclusively establish any actual loan transaction. It is further noticed that the alleged promissory notes neither contain complete particulars of the lenders nor specify the nature of payment. Even the relevant columns relating to cash/cheque were left blank. The documents do not bear complete execution details so as to establish that any enforceable transaction had actually taken place. Therefore, mere existence of such incomplete documents cannot automatically lead to the inference that the assessee had in fact received cash loans of Rs.48,00,000/-. More importantly, except for the images found in the mobile phone, no corroborative evidence whatsoever has been brought on record by the AO to prove actual receipt of money by the assessee. No evidence relating to cash flow, bank deposits, confirmations, statements of lenders, cash trail or any other incriminating material has been found or brought on record. The AO has proceeded purely on assumptions and presumptions without conducting any independent enquiry.

16.1. The provisions of section 68 can be invoked only when there is a credited amount found in the books of account of the assessee and the assessee fails to satisfactorily explain the nature and source thereof. In the present case, the addition is not based on any actual credit entry found in the books of account but merely on certain incomplete images recovered from a mobile phone. In the absence of evidence establishing actual receipt of money, the foundational requirement for invoking section 68 itself remains unfulfilled. The Ld. CIT(A), after detailed examination of facts, rightly observed that the alleged promissory notes were incomplete and inconclusive in nature and that the AO failed to establish whether any actual loans were received against such documents. The findings recorded by the Ld. CIT(A) remain unrebutted by the Revenue by bringing any contrary material on record.

16.2. It is a settled principle of law that addition cannot be sustained merely on suspicion, conjectures or surmises. Loose papers, draft documents or incomplete notings, in absence of independent corroboration, do not constitute conclusive evidence for making addition under the Act. Since the Revenue has failed to establish with cogent evidence that the assessee actually received unexplained cash loans of Rs.48 lakhs the addition made by the AO is unsustainable. Accordingly, we find no infirmity in the order of the Ld. CIT(A) deleting the addition of Rs.48 lakhs. The same is hereby upheld and the Ground no.2 raised by the Revenue is devoid of merits and hereby dismissed.

17. Regarding Ground No.2 namely deletion of Unexplained investment in land at Ambali of Rs.1 Crore and Ground No.3 of the assessee namely confirmation of addition of Rs.5 lakhs being brokerage earned @ 5%. Since both the issues are interconnected the same are dealt herein together. The brief facts of the case are that during the course of search proceedings, an image relating to a proposed land transaction was found from the mobile phone of the assessee. Based on the contents of the image, the AO observed that a token amount of Rs.1,00,00,000/-had allegedly been paid in connection with the said land deal. The AO further observed that the Memorandum of Understanding relating to the transaction was dated 26.08.2017 relevant to Assessment Year 2018-19. According to the AO, the assessee failed to furnish complete details of the parties involved in the transaction. Referring to the provisions of section 132(4A) of the Act, the AO presumed that the contents of the document belonged to the assessee and represented unexplained investment made by him. Accordingly, the AO added Rs.1,00,00,000/- to the income of the assessee.

17.1 . On appeal Ld. CIT(A), after considering the submissions of the assessee and examining the material available on record, observed that the assessee was neither the buyer nor the seller in the impugned land transaction. The Ld. CIT(A) further noted that the Assessing Officer himself had verified from the Government records that the property continued to remain in the name of the original owners and was under litigation, thereby establishing that the transaction had never materialized. The Ld. CIT(A) further held that though the image prima facie referred to payment of token amount, there was no corroborative evidence to establish that the assessee himself had made such payment. Since the assessee admitted to having acted merely as a broker in the proposed transaction, the Ld. CIT(A) held that at best only brokerage income could be brought to tax in the hands of the assessee and not the entire amount of Rs.1 crore. Considering the nature of services rendered by the assessee in such transactions, the Ld. CIT(A) estimated brokerage income at 5% and sustained addition of Rs.5,00,000/- while deleting the balance addition of Rs.95,00,000/-.

17.2 Thus Revenue is in appeal against the relief granted by the Ld. CIT(A), whereas the assessee is aggrieved by the addition of brokerage addition.

18. We have heard the rival submissions and perused the materials available on record. The entire addition of Rs.1 crore has been made by the AO merely on the basis of an image found from the mobile phone of the assessee indicating payment of token amount in relation to a proposed land transaction. On careful perusal of the assessment order as well as the findings recorded by the Ld. CIT(A), it emerges as an undisputed fact that the assessee was neither the Purchaser nor the Seller of the impugned property. In fact, the Ld AO himself verified from Government records and reproduced data downloaded from the AnyROR [Gujarat government portal] that the property continued to remain in the name of the original owners and was under litigation. Therefore, the material available on record clearly demonstrates that the proposed land transaction never culminated into an actual transfer. Further, except for the impugned image, no corroborative evidence has been brought on record by the Revenue to establish that the assessee had actually invested an amount of Rs.1 crore in the said property transaction. No evidence regarding source of funds, payment trail, bank transaction, cash movement, confirmation from parties or execution of sale transaction has been brought on record. The addition has thus been made merely on assumptions drawn from a solitary image recovered from the mobile phone of the assessee is unsustainable in law.

18.1. It is well settled that loose papers, unsigned documents or electronic images, in absence of corroborative evidence, cannot conclusively establish undisclosed investment. Though the presumption under section 132(4A) may permit the Revenue to draw a prima facie inference regarding possession and contents of seized material, such presumption is rebuttable and cannot by itself dispense with the requirement of establishing actual investment through cogent evidence. In the present case, the Revenue has failed to establish that the amount of Rs.1 crore represented investment made by the assessee in his personal capacity. On the contrary, the material on record supports the explanation of the assessee that he had merely acted as a broker in the proposed transaction. However, the land deal itself is not materialised and land itself is in dispute as per State Government records, therefore there cannot be addition on account of payment of brokerage to the assessee at 5% and the addition made by the Ld CIT[A] is liable to be deleted. In the result, the Ground No.2 filed by the Revenue is dismissed and Ground No.3 filed by the assessee is allowed.

19. Regarding Ground No.3 namely CIT(A) has erred in deleting the addition of Rs.3,22,00,000/ on account of unexplained advance without appreciating the facts that during the post search proceedings, the assessee himself accepted that the transactions are unaccounted and he earned interest of Rs. 29,05,858/as well. The facts in brief are that during the course of search proceedings, certain images were found from the mobile phone of the assessee. Based on the notings contained in such images, the Assessing Officer made additions aggregating to Rs.3,49,05,858/ comprising of Rs.2,72,00,000/ Rs.29,05,858/- and Rs.50,00,000/- treating the same as undisclosed income of the assessee. According to the AO, the seized images represented unaccounted transactions undertaken by the assessee during the relevant previous year. The AO accordingly treated the amounts noted therein as unexplained transactions and added the same to the income of the assessee.

19.1. On appeal Ld. CIT(A), after considering the submissions of the assessee and examining the seized material, deleted the additions of Rs.2,72,00,000/- and Rs.50,00,000/- while sustaining the addition of Rs.29,05,858/- towards interest income. The Revenue is aggrieved by the deletion of additions whereas the assessee is aggrieved by the addition of Rs.29,05,858/- towards interest.

20. The Ld. CIT-DR Mr. Alpesh Parmar appearing for the Revenue relied upon the findings of the AO and submitted that the seized images clearly reflected undisclosed transactions undertaken by the assessee. It was contended that the assessee failed to properly explain the nature and source of the entries contained in the images and therefore the AO was justified in making the additions.

21. Per contra, the Ld. AR for the assessee supported the order of the Ld. CIT(A) deleting the additions and submitted that the entries merely represented loan transactions and interest calculations. It was argued that no corroborative evidence was found by the Revenue to establish that the amounts represented undisclosed income of the assessee for the year under consideration.

22. We have heard the rival submissions and perused the material available on record. The additions in the present case have been made solely on the basis of certain images found from the mobile phone of the assessee. On perusal of the seized images, it is noticed that the nature of the transactions is nowhere specified in the documents. The notings merely contain figures along with calculations of interest and dates of repayment. The seized material does not conclusively establish whether the entries relate to loans advanced, loans received, investments or any other nature of transactions. It is further observed that no year or relevant period is mentioned in the seized images so as to conclusively hold that the transactions pertain to the financial year relevant to the asst year 2018-19. The AO has merely presumed that the entries relate to the current assessment year without bringing any supporting evidence on record.

22.1. As regards the addition of Rs.2,72,00,000/-, the seized image itself reflects the said amount as opening balance as on 1st April. Therefore, even assuming the entries relate to loan transactions, the same cannot be treated as income arising during the year under consideration. Moreover, both the assessee as well as the Ld AO have proceeded on the basis that the transactions represented loan transactions carrying interest. In absence of any corroborative material to establish that the said amount represented undisclosed income earned during the year, the addition made by the AO is unsustainable in law.

22.2. The Ld. CIT(A), after appreciating the seized material in proper perspective, rightly held that no addition could be made merely on the basis of ambiguous notings found in electronic form without any corroborative evidence. The Revenue has failed to controvert the findings of the Ld. CIT(A) by bringing any contrary material on record. Therefore, I find no infirmity in the deletion of addition of Rs.2,72,00,000/-.

22.3. With regard to the addition of Rs.50,00,000/-, it is noticed that the seized image does not clearly indicate whether the amount represented cash paid or cash received. The assessee had submitted loan confirmations indicating cheque transactions. As rightly observed by the Ld. CIT(A), if the interpretation of the AO is accepted, the corresponding cash entries would indicate cash received by the assessee and not cash paid by him. Even otherwise, in absence of any clarity regarding the nature of the transaction and without any supporting evidence, no addition could have been made merely on presumptions and assumptions. It is a settled proposition of law that loose papers, rough notings or electronic images by themselves do not constitute conclusive evidence unless corroborated by independent material. Suspicion, however strong, cannot substitute legal proof. Since the Revenue has failed to establish through cogent evidence that the amount of Rs.50,00,000/- represented undisclosed income of the assessee, the deletion made by the Ld. CIT(A) is justified. Accordingly, we uphold the order of the Ld. CIT(A) deleting the additions of Rs.2,72,00,000/- and Rs.50,00,000/- and the Ground No.3 raised by the Revenue is devoid of merits and liable to dismissed.

23. Ground No.4 raised by the Revenue is ld. CIT(A) erred in deleting the addition of Rs.6,01,60,800/- on account of unaccounted income as per whatsapp chats extracted from the mobile phone of Dhaval N. Patel simply relying upon the submission of the assessee and without any verification of the said transaction from the seized diary in the case of Prakash M Sanghvi.

24. We have heard rival submissions and perused the materials available on record and including the Paper Books filed by the assessee and seized materials. We have discussed the facts of the case and reproduced the findings of Ld CIT[A] at paragraph 6 and 6.1 above. We need not much labour on this addition in the case of the assessee, since Co-ordinate Bench of this Tribunal in the case of Prakash Misrimal Sanghvi v. Dy. CIT [IT Appeal Nos. 1138 to 1146/Ahd/2024, dated 18-02-2025] wherein JM is the co-author] discussed in detail and held that where no principle was recovered from parties over a long period of time, the entry for notional interest cannot be held as accrued and considered as ‘real income’, specially when the AO had already made addition for the actual interest received was separately credited in the seized diaries under “Shree Vyaj Khate” and following the cash system of accounting, no addition could have been made in respect of notional entries on the basis of mercantile system of accounting. We, therefore, do not find any reason to interfere with the findings and the decision of the Ld. CIT(A) on this issue. Further, when the interest actually realized by the Prakash Misrimal Sanghvi was already taxed following the cash system of accounting, no addition could have been made in respect of notional interest on accrual basis. We, therefore, do not find anything wrong with the findings and the decision of the Ld. CIT(A) on this issue.

24.1. Ld AR for the assessee also placed on record, pursuant to the order by this Tribunal, the various additions amounting to Rs.189.84 crores confirmed in the hands of Sri. Prakash Misrimal Sanghavi for the various Asst. years 2013-14 to 202122. Thus we have no hesitation in confirming the orders passed by Ld CIT[A] deleting the addition made in the hands of the assessee, since already additions were made in the hands of Sri. Prakash Misrimal Sanghavi for the various Asst. years 2013-14 to 2021-22. Therefore, taxing the same income again in the hands of the assessee would result in double taxation, which is impermissible. Thus, the Ground No.4 raised by the Revenue is devoid of merits and liable to be dismissed.

25. In the result, the appeal filed by the Revenue in IT[SS]A No.77/Ahd/ 2024 is dismissed.

AY 2019-20

26. Assessments were completed for the asst years 2019-20 by making following disallowances:

| Asst. Year |

Date |

Nature of disallowance |

Amount |

|

|

Unexplained cash receipts

Unexplained cash receipts and unaccounted brokerage

Unexplained cash receipts

Unexplained investment

Unexplained credits in bank account

Unexplained transactions

Unexplained transactions

Unaccounted cash found in locker

Unaccounted cash found in residence

Unaccounted Foreign currency found in residence

Unaccounted Jewellery found in locker

Unaccounted loan

Unaccounted Interest paid

Unaccounted transaction

Unaccounted cash receipt

Unaccounted brokerage income

Unaccounted income |

5,25,87,500

1,67,57,000

54,29,200

1,83,81,000

46,68,168

58,00,000

10,00,000

1,04,00 7,92,750

22,72,470

6,89,078

8,75,000

40,157

30,00,000

3,16,14,625

9,27,000

2,31,192 |

26.1. Aggrieved against the assessment order the assessee filed appeal before Ld CIT[A], who by common order dated 19-072024 confirmed few additions/disallowances and deleted few additions.

27. Now let us deal with each [Modified] Grounds of Appeal raised by the Assessee in ITA No.1582/Ahd/2024:

| 1. |

|

The learned CIT(A) has erred in not holding that the notice issued u/s 143(2) of the Act is bad in law, illegal and void-ab-initio. The learned CIT (A) has erred in not holding that the assessment order passed by AO u/s. 143(3) of the Act is bad in law, illegal and null and void. |

| 2. |

|

The learned CIT(A) has erred in confirming the additions made by AO in the Appellant’s case and rejecting the submissions that the noting in the image/chat do not pertain to/belong to the Appellant. |

| 3. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 26,29,375/-on account of brokerage. |

| 4. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 1,65,000/-on account of brokerage. |

| 5. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 9,40,000/-on account of unaccounted profit. |

| 6. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 58,00,000/-as unexplained transaction on the bases of Whatsapp chat. |

| 7. |

|

The learned CIT(A) has erred in confirming the addition of Rs. 40,157/-as interest on unaccounted loan. |

| 8. |

|

The learned CIT(A) has erred in facts in ignoring that Rs. 9,27,000/- is already offered in the revised computation filed with AO. |

| 9. |

|

The learned CIT(A) has erred in facts in ignoring that Rs. 91,111/- towards brokerage is already offered in the revised computation filed with AO. |

| 10. |

|

The learned CIT(A) has erred in not giving the benefit of telescoping in respect of application of income (towards expenses/assets/cash) against additions confirmed on the basis of receipts representing source of funds. The Id. CIT (A) ought to have held that benefit of telescoping should be given to the assessee in respect of additions made by the AO on the basis of receipts and payments. |

| 11. |

|

The Appellant states that the search proceedings carried out in his case are beyond jurisdiction, illegal and void. The consequential assessment order passed is bad-in-law, illegal and void-ab-initio. |

| 12. |

|

The learned CIT(A) has erred in not holding that the assessment order passed by AO is in gross violation of principles of natural justice. |

| 13. |

|

The Appellant craves leave to add, amend and/ or alter the ground or grounds of appeal either before or at the time of hearing of the appeal. |

28. Ld AR Shri Vijay Mehta appearing for the assessee submitted that the assessee is NOT Pressing Ground Nos. 1, 2, 7, 8, 9, 11, 12 and 13 on the jurisdiction of assessment and other issues. Recording the same Ground Nos. 1, 2, 7, 8, 9, 11, 12 and 13 are dismissed as NOT Pressed.

29. Ground Nos.3, 4 & 5 raised by the assessee are inter connected with the Ground Nos.1, 2 & 3 raised by the Revenue. Hence the same are dealt together in Revenue appeal.

30. Regarding Ground No. 6 namely unaccounted income of Rs.58,00,000 as per WhatsApp chat (Page no 32 of assessment order). During the course of search, following WhatsApp chats were seized from assessee’s mobile.

| “a. |

|

Original rtgs of 59.00 and 8.00 from Dhaval Patel so totaling to 67.00, last week given 8.00 cash so 75.00 and not doing rtgs of 32.00 so 108.00 and 8.00 refunding so net 100.00. |

| b. |

|

Have you pick up cash 50 Saturday from angadiya” |

30.1. As regards the WhatsApp message of Rs. 8,00,000 the AO held that the contents of the WhatsApp message clearly indicate that cash transaction of Rs. 8,00,000 has been carried out and that the other contents of the message are accounted for and transactions have happened so there is no reason to assume that unaccounted transaction did not occur.

30.2. As regards WhatsApp message of Rs.50,00,000 the AO held that the transaction of Rs.50,00,000 was accepted by the assessee as unaccounted transaction as the same was incorporated in the cash book submitted during post search proceedings.

31. On appeal before ld CIT (A), who confirmed the addition of Rs.58,00,000 as the chat clearly mentioned that cash was collected.

32. Ld AR appearing for the assessee submitted that the addition of Rs.8 lakhs was made on the basis of WhatsApp chat and no corroborative material or evidence found. Further the WhatsApp chat referred to RTGS of Rs. 8 lacs which was actually not sent. Same can be verified from bank statement. Also, other RTGS mentioned in the same chat were actually sent. Similarly, cash of Rs. 8 lacs was not sent. Also, refund of RTGS of Rs. 8 lacs is mentioned in the same WhatsApp chat which did not take place since the original RTGS of Rs.8 lacs was also not done. Thus, all the transactions noted in the WhatsApp chat including bank transactions did not take place. On similar grounds cash transaction of Rs. 8 lacs did not take place and there is no other chat or corroborative material found for the same.

33. Ld AR appearing for the assessee submitted that the addition of Rs.50 lakhs made on the basis of WhatsApp chat. No corroborative material or evidence found. The WhatsApp chat was sent by appellant to Malav asking him whether 50 was collected from Angadiya. No such amount was received through Angadiya and no corroborative material or evidence found. Further back-up of entire mobile of the assessee was taken and no other chat confirming receipt of Rs. 50 lacs through Angadiya was found, no details as to the name of the Angadiya, particulars, etc. were mentioned in the chat. Thus, there is no material or evidence establishing that the said amount of Rs. 50 lacs was actually received through Angadiya. Without prejudice, if AO’s contention is believed, assessee received Rs. 50 lacs through Angadiya which can be on client account and cannot be treated as income of the assesssee.

34. Per contra Ld CIT DR appearing for the Revenue supported the orders passed by the Lower Authorities and requested to confirm the additions.

35. Heard rival submissions and perused the materials available on record. As regards the addition of Rs.8,00,000/-, the WhatsApp message reproduced by the AO, inferred that cash transaction of Rs.8,00,000/- had actually taken place. However, except for the aforesaid WhatsApp message, no corroborative material whatsoever has been brought on record by the Revenue to establish that any such cash transaction was actually carried out. The assessee has specifically contended that the RTGS transaction of Rs.8,00,000/- referred to in the same message never materialized and the same is verifiable from the bank statement. It is also submitted that the reference to “8.00 refunding” equally did not materialize. Thus, according to the assessee, the WhatsApp message merely records proposed or contemplated transactions and not concluded transactions.

35.1. It is a settled proposition that loose notings, dumb documents, WhatsApp chats or uncorroborated electronic material, by themselves, cannot form the sole basis for making addition unless supported by independent evidence establishing that the transaction actually took place. In the present case, no cash was found during search relatable to the impugned entry, no corresponding entry was found in any books or diaries, no statement of the counter-party was recorded, and no trail of movement of funds has been brought on record. The AO has merely proceeded on presumption that since some transactions mentioned in the chat had happened, the alleged cash transaction must also have happened. Such inference, in absence of supporting evidence, cannot take the place of proof.

35.2. Further, the contents of the message themselves indicate that the discussion was in the nature of reconciliation or proposed adjustments between RTGS and cash components. The Revenue has not demonstrated with cogent material that the alleged cash amount of Rs.8,00,000/- was in fact paid or received by the assessee. In absence of corroborative evidence, the addition of Rs.8,00,000/- is based merely on suspicion and conjectures and therefore cannot be sustained.

35.3. Coming to the addition of Rs.50,00,000/-, the WhatsApp message relied upon by the AO reads as “Have you pick up cash 50 Saturday from angadiya.” The AO held that the assessee had accepted the transaction as unaccounted since the same was allegedly incorporated in the cash book submitted during postsearch proceedings. However, on perusal of the assessment order, no specific cash entry corresponding to the impugned amount has been identified by the AO. Further, except for the aforesaid one-line WhatsApp message, there is no corroborative material evidencing actual receipt of cash of Rs.50,00,000/-through any Angadiya channel.

35.4. The message merely enquires whether cash was picked up from an Angadiya. The message neither identifies the sender nor the recipient of funds, nor specifies the Angadiya operator, date, place or purpose of the alleged transaction. No investigation has been conducted by the Ld AO to verify the identity of the alleged Angadiya operator or the movement of funds. No corresponding asset, investment, expenditure, or cash utilization has been brought on record. Admittedly, even after complete extraction of mobile data, no further chats or material evidencing completion of the transaction were found.

35.5. The addition has thus been made solely on the basis of an isolated WhatsApp message without any independent corroboration. It is trite law that however strong the suspicion may be, the same cannot substitute legal evidence. In search assessments particularly, additions are required to be based on credible and cogent incriminating material. A vague and incomplete WhatsApp message, without supporting evidence establishing actual flow of unaccounted money, cannot justify addition under the Act.

36. In view of the above facts and circumstances, we are of the considered view that the Revenue has failed to discharge the burden of proving that the impugned amounts of Rs.8,00,000/-and Rs.50,00,000/- represented undisclosed income of the assessee. Accordingly, the addition of Rs.58,00,000/- sustained by the ld. CIT(A) is directed to be deleted. Thus, Ground No.6 of the assessee is allowed.

37. Regarding Ground No.10, the ld. AR submitted that during the course of assessment, various additions were made by the AO both on account of alleged unexplained receipts/source of funds as well as on account of alleged unexplained expenditure, investments, assets and cash applications. A chart demonstrating the nexus between the additions representing source and application of funds was also filed before the lower authorities. It was contended that once certain receipts are treated as undisclosed income of the assessee, corresponding application or utilization thereof cannot again be separately taxed, as the same would amount to double addition of the very same income. Accordingly, it was prayed that suitable benefit of telescoping/set-off be granted in respect of additions sustained, if any.

38. We have considered the rival submissions and perused the materials available on record. The principle of telescoping is a well-recognized principle in taxation jurisprudence. Where additions are made on account of undisclosed income or unexplained receipts, and there are corresponding additions towards investments, expenditure, cash, assets or other applications of funds, the assessee is entitled to claim that such application has been made out of the undisclosed income already brought to tax. The object is to avoid double taxation of the same income under different heads or in different forms.

38.1. It is settled law that once the source of funds stands taxed in the hands of the assessee, separate addition towards utilization or application of the same funds should not ordinarily be made unless the Revenue establishes that the applications are from independent and distinct unexplained sources. The Revenue cannot simultaneously treat the same amount both as undisclosed receipt and also as unexplained investment/ expenditure without establishing separate streams of income.

38.2. In the present case, the assessee had furnished a chart correlating additions made by the AO towards alleged receipts/ source of funds and additions made towards alleged expenditure/application of funds. However, the lower authorities have not properly examined the claim of telescoping in the light of the factual nexus demonstrated by the assessee. In my considered view, the claim of telescoping deserves to be allowed wherever the additions sustained on account of application of funds can reasonably be correlated with additions sustained on account of unexplained receipts or undisclosed income.

38.3. Accordingly, the AO is directed to grant the benefit of telescoping/set-off in respect of additions sustained, if any, towards unexplained expenditure, investments, assets, cash or other applications of funds against additions sustained on account of unexplained receipts/source of funds, after due verification of the nexus and to the extent overlap is established. Needless to mention, the same income cannot be taxed twice in different forms. Thus, Ground No.10 raised by the assessee is allowed for statistical purposes.

39. In the result, the appeal filed by the assessee in ITA No. 1582/Ahd/20224 is partly allowed.

40. Grounds of Appeal raised by the Revenue in ITA No. 1647/Ahd/ 2024:

| 1) |

|

“In the facts and on the circumstances of the case and in law, the Id.CIT(A) has erred in deleting the addition of Rs. 4,99,58,125/- out of total addition of Rs. 5,25,87,500/- on account of unexplained cash receipt without appreciating the facts that during the course of assessment proceedings, the assessee failed to explain source of such cash receipt.” |

| 2) |

|

“In the facts and on the circumstances of the case and in law, the ld. CITIA) has erred in deleting the addition of Rs 1,65,92,000/- out of total addition of Rs. 1,67,57,000/-on account of unexplained cash receipt & unaccounted brokerage in land without appreciating the facts that during the post search inquiry, the assessee failed to give details of the parties involved in the said land deal and considering the assessee as broker in the land deal without mentioning any cogent proof. |

| 3) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of Rs.44,89,200/- out of total addition of Rs.54,29,200/- on account of unexplained cash receipt without appreciating the facts that during the post search inquiry, the assessee failed in establishing the source of funds regarding the transactions.” |

| 4) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of Rs.1,83,81,000/- on account of unexplained investment without appreciating the facts that during the post search inquiry, the assessee failed to give details of the parties involved in the said land deal.” |

| 5) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of Rs. 10,00,000/- on account of unexplained transactions contained in whats app chats ignoring the message found in the whatsapp chats of the assessee.” |

| 6) |

|

“In the facts and on the circumstances of the case and in law, the ld. CIT(A) has erred in deleting the addition of addition of Rs.6,89,078/ on account of Unexplained jewellery found from Locker without appreciating the facts that during post search proceedings assessee himself accepted that the said jewellery was purchased from unexplained sources.” |

| 7) |

|

“In the facts and on the circumstances of the case and in law, the ld. CIT(A) has erred in deleting the addition of addition of Rs.8,75,000/- on account of unaccounted loan taken without appreciating the facts that the assessee failed to provide the genuineness of transactions, identity of persons & creditworthiness of lenders etc to substantiate the transactions.” |

| 8) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of addition of Rs.30,00,000/- on account of unaccounted transaction ignoring the facts that assessee has failed to substantiate the said transaction.” |

| 9) |

|

“In the facts and on the circumstances of the case and in law, the ld.CIT(A) has erred in deleting the addition of Rs.3,16,14,625/- on account of Unaccounted cash receipt against the sale of land situated at Chandkheda ignoring the facts that as per incriminating documents found, the transactions of said land were done and the cash was received by the assessee.” |

| 10) |

|

“The Revenue craves leave to add/alter/armed and/or substitute any or all of the grounds of appeal” |

41. Ground No.1 by the Revenue and Ground No.3 by the Assessee. Addition u/s.68 of the Act of Rs.5,25,87,500/- made by the AO based on image allegedly containing cash receipts and opening balance. On appeal Ld CIT[A] deleted the addition by observing as follows:

“. 43.5 I have considered the submissions made by the appellant and the contentions of the AO. The AO has while giving background of the appellant, emphasized in the assessment order that the appellant is handling the real estate deals of Riddhi Siddhi Group. The AO has admitted the fact that appellant has acted as a broker and a custodian for the deals of Riddhi Siddhi Group and made addition on account of brokerage in the appellant’s case. It is also stated by the AO that the appellant is found to be the most trusted person of Riddhi Siddhi group and the appellant is handling the unaccounted cash transactions of Riddhi Siddhi Group.

43.6 Thus, it is an admitted fact by the AO that the appellant acted as a broker for Riddhi Siddhi Group and handled various sale and purchase deals of the group. Thus, the image found from the appellant represents amounts handled by the appellant on behalf of his client. The appellant has also provided intermediary services including negotiations, finalisation of terms and process to be followed, handling payment transactions, etc. The appellant has not provided detalls of brokerage income earned on account of real estate transactions of Riddhi Siddhi group and has not shown the same in his return of Income. Thus, brokerage income should be added to the income of the appellant.

43.7 It is observed from the facts on record that the appellant is not acting only as a broker but he is also providing various ancillary services like approaching the solicitors, following up with the procedures, acting as a custodian wherever required. Therefore, the appellant cannot be said to have earned mere brokerage like other brokers who act only as a broker. Considering the totality of the facts of the case and the services provided by the appellant, addition of brokerage @5% would meet the ends of justice.

43.8 Thus, the entire amount of Rs.5,25,87,500/-representing transactions undertaken on behalf of Riddhi Siddhi group cannot be added to the total Income of the appellant as these transactions do not pertain to him. The appeal in the case of Riddhi Siddhi Infraspace LLP has been adjudicated by the undersigned and an order dated 26.03.2024 has been passed. In the appellate order, the undersigned has confirmed additions on account of cash received by Riddhi Siddhi group from Rajanbhai. The amount noted in the image is fraction of the total deal and confirming addition of the same in the appellant’s case would amount to double addition.

43.9 Since the appellant has not offered any brokerage income on the above deals, addition of 5% i.e. Rs 26,29,375/-is confirmed in the case of the appellant and the remaining addition of Rs.4,99,58,125/- is deleted. Since acting as a broker is the main business activity of the appellant, the income is required to be taxed u/s 28 of the Act and therefore the provisions of section 115BBE will not be applicable to the addition of Rs.26,29,375/- confirmed in the appellant’s case. Thus, the grounds of appeal no. 2 to 4 are partly allowed.

42. Ld AR appearing for the assessee submitted that the assessee was acting as an intermediary on behalf of Riddhi Siddhi group in respect of their real estate transactions and the transaction does not pertain to the assessee. The transaction pertains to Riddhi Siddhi group and addition for the same is considered in the case of Riddhi Siddhi group. As regards the AO’s contention that the assessee has admitted these transactions by way of incorporating them in the cash book submitted before Investigation Wing, it is submitted that the assessee has nowhere admitted that these are his unaccounted transactions. The assessee has consistently stated that he has acted as a broker and the image represents amounts received and given on behalf of his clients. In fact the AO has admitted that the assessee was most trusted person of Riddhi Siddhi group. The AO has held that from the evidences found, the assessee is found to be handling unaccounted cash transactions of Riddhi Siddhi group. The AO has stated that the cash of Rs. 4,44,96,000 seized from the corporate office of Riddhi Siddhi group was also found in the possession of the assessee and thus confirmed that the assessee was key person of Riddhi Siddhi group. Thus, the AO has admitted that the assessee was acting on behalf of Riddhi Siddhi group. Further, Riddhi Siddhi group had sold real estate to Rajanbhai and the cash of Rs. 1,00,00,000 shown as received from Rajanbhai in the image, was towards the said sale and addition for the said sale transaction with Rajanbhai is already made in the case of Riddhi Siddhi group. As regards, the addition of brokerage @5% it is submitted that in the assessee’s line of business, normal brokerage is 1% to 2% which fact has also been stated by the AO at various places in the assessment order. Thus, addition on account of brokerage, if any should be made at a reasonable % and not at 5% as confirmed by Ld CIT(A).

43. Per contra Ld CIT DR requested to sustain the addition made by the Ld AO.

44. We have considered the rival submissions and perused the material available on record. The issue involved in the present ground relates to addition sustained by the ld. CIT(A) to the extent of Rs.26,29,375/- being 5% of the total transaction value of Rs.5,25,87,500/- treated as brokerage/commission income earned by the assessee in relation to transactions undertaken on behalf of Riddhi Siddhi Group.

44.1. The facts emerging from record show that during the course of search certain images/documents were found from the mobile phone of the assessee containing details of cash transactions relating to real estate dealings. The AO treated the entire amount of Rs.5,25,87,500/- as unexplained income of the assessee. However, the ld. CIT(A), after examining the surrounding facts and material on record, recorded a categorical finding that the assessee was acting as an intermediary/broker for Riddhi Siddhi Group and that the transactions reflected in the seized material did not pertain to the assessee in his individual capacity.

44.2. The ld. CIT(A) has specifically noted that the AO himself, in the assessment order, repeatedly acknowledged that the assessee was handling real estate transactions of Riddhi Siddhi Group, acting as a broker/custodian and managing unaccounted cash transactions on behalf of the group. The ld. CIT(A) further observed that corresponding additions relating to the substantive real estate transactions had already been considered in the hands of Riddhi Siddhi Group and therefore addition of the entire amount again in the hands of the assessee would result in impermissible double taxation.

44.3. The aforesaid findings of the ld. CIT(A) have not been controverted by the Revenue by bringing any material on record to establish that the impugned amounts actually belonged to the assessee. On the contrary, the material on record supports the consistent stand of the assessee that he was functioning as an intermediary in real estate transactions of Riddhi Siddhi Group and was handling negotiations, coordination, cash movement and related activities on behalf of the group.

44.4. In view of the above factual position, we are in complete agreement with the finding of the ld. CIT(A) that the entire transaction value of Rs.5,25,87,500/- could not have been assessed as undisclosed income in the hands of the assessee. Once the substantive transactions are accepted as pertaining to Riddhi Siddhi Group and corresponding additions have already been examined in the hands of such group concerns, taxing the entire amount again in the hands of the assessee merely because he acted as an intermediary would clearly amount to double addition. Thus, the Ground No.1 raised by the Revenue is devoid of merits and liable to be dismissed.

45. The next issue for consideration is regarding estimation of brokerage income. The ld. CIT(A) sustained addition by estimating brokerage/commission income at 5% of the transaction value considering the nature of services rendered by the assessee. The assessee has contended that in the line of real estate brokerage business, normal brokerage ranges between 1% to 2%, which fact has also been acknowledged by the AO in the assessment order, and therefore estimation at 5% is excessive and arbitrary.

46. We find merit in the contention of the assessee. Though the assessee appears to have rendered services wider than that of a conventional property broker, including coordination, liaisoning, handling documentation and acting as custodian for cash movement, estimation of brokerage at 5% of the total transaction value appears on the higher side in absence of any comparable instances or material brought on record by the Revenue. The estimation made by the ld. CIT(A) is purely adhoc and not supported by any cogent basis.

46.1. Considering the nature of activities carried out by the assessee, the volume of transactions and the prevailing practice in the real estate market, I am of the considered view that estimation of income at 2% of the transaction value would meet the ends of justice. Accordingly, the brokerage/commission income is restricted to 2% of Rs.5,25,87,500/-, which works out to Rs.10,51,750/-.Since the income represents brokerage/ business income arising from activities carried out by the assessee as intermediary in real estate transactions, the same shall be assessable under the head “Profits and Gains of Business or Profession” and consequently the provisions of section 115BBE shall not apply. Accordingly, the addition sustained by the ld. CIT(A) is reduced from Rs.26,29,375/- to Rs.10,51,750/-. Thus, the ground no.3 raised by the assessee is partly allowed.

47. Ground No.2 by the Revenue and Ground No.4 by the Assessee. Addition of Unexplained and unaccounted cash receipt of Rs.1,67,57,000/- and Brokerage of Rs.1,65,000/ on land deal made by the AO based on the image containing in mobile phone. On appeal Ld CIT[A] deleted the addition by observing as follows:

“…44.4 I have considered the submissions made by the appellant and the contentions of the AO. It is seen from the assessment order that it is not the AO’s case that the appellant is a buyer or seller in the above deal. As per AO, the appellant has acted as a broker and the AO has made addition of brokerage as well in the appellant’s case.

44.5 It is an undisputed fact that the appellant is a real estate broker and not the buyer or seller in the above deal. Therefore, addition of the entire sale consideration of Rs.1,65,92,000/- cannot be made in the appellant’s case. The appellant has himself accepted that the brokerage of Rs.82,500/- was offered as income being his share of 50% since he was a joint broker.

However, the appellant has failed to provide details of the other broker and therefore addition in respect of entire brokerage of Rs.1,65,000/- is considered to be the income of the appellant. Since acting as a broker is the main business activity of the appellant, the income is required to be taxed u/s 28 of the Act and therefore the provisions of section 115BBE will not be applicable to the addition of Rs. 1,65,000/-confirmed in the appellant’s case. Thus, the grounds of appeal no. 5 to 7 are partly allowed.”

48. Ld AR appearing for the assessee submitted that on perusal of the image it cannot be ascertained that the deal has actually taken place. Similarly, the year in which the deal is carried out is also not written on the image. Ld AO has presumed that the transaction pertains to the year under consideration. Since no details as to the land, buyer, seller, etc. were mentioned on the image, appellant could not provide any information. The AO has not brought any material on record to evidence that any such land was sold by the assessee and that the agreement value was credited in the assessee’s bank account or that the assessee had executed any registered agreement. Therefore, the sale consideration cannot be added in the assessee’s hands. Further, in the absence of any material evidencing that the deal had actually taken place, addition on account of brokerage cannot be made in appellant’s case.

49. Per contra Ld CIT DR requested to sustain the additions made by the Ld AO.

50. We have considered the rival submissions and perused the materials available on record. The issue involved in the present ground relates to addition sustained by the ld. CIT(A) to the extent of Rs.1,65,000/- being alleged brokerage income arising from a real estate transaction noted in an image found during the course of search. The Ld AO had treated the notings contained in the seized image as representing sale transaction of immovable property involving consideration of Rs.1,65,92,000/-. Though the AO did not treat the assessee as buyer or seller in the transaction, he proceeded on the footing that the assessee acted as a broker in the deal and accordingly made addition. The ld. CIT(A), while holding that the entire sale consideration could not be assessed in the hands of the assessee, sustained addition of brokerage income of Rs.1,65,000/- on the reasoning that the assessee failed to furnish details of the alleged co-broker.

50.1. From the material placed on record, it emerges that the impugned addition is based solely on certain rough notings contained in an image found from the mobile phone of the assessee. The seized material does not contain complete particulars of the alleged transaction such as identity of buyer, seller, survey number of land, location of property, date of transaction, or details of execution of any agreement. Even the year to which the transaction allegedly pertains is not discernible from the seized material. The AO has merely presumed that the transaction pertains to the year under consideration without bringing any independent evidence on record.

50.2. It is also not the case of the Revenue that any corresponding registered document was discovered during search or that any sale consideration moved through the bank account of the assessee. No enquiry has been conducted with any alleged purchaser or seller. No evidence has been brought on record to establish that the alleged land transaction was actually concluded. Thus, the very existence and completion of the transaction itself remains unsubstantiated. However the ld. CIT(A) sustained brokerage addition primarily on the basis that the assessee admitted offering Rs.82,500/- as his share of brokerage income. However, merely because the assessee, during the course of proceedings, attempted to explain the seized material by assuming that it may relate to a brokerage transaction, the same cannot by itself establish conclusively that the underlying property transaction had actually materialized. In the absence of any corroborative material evidencing completion of the deal, no income can be brought to tax merely on the basis of conjectural notings.

50.3. In the present case, except for the isolated image containing incomplete notings, no material has been brought on record to establish that the alleged land deal was finalized or that the assessee actually earned brokerage income therefrom. The Revenue has failed to discharge the primary burden cast upon it. Therefore, even the addition sustained by the ld. CIT(A) towards brokerage income cannot be upheld. In view of the aforesaid facts and circumstances, the addition of Rs.1,65,000/- sustained by the ld. CIT(A) is directed to be deleted. Consequently, the Ground No.4 raised by the assessee is allowed. We do not any merit in the Ground No. 2 raised by the Revenue and the same is dismissed.

51. Ground No.3 raised by the Revenue and Ground No.5 raised by the Assessee. Addition of Rs.54,29,200/-[Unaccounted Income Rs.44,89,200 + Profit of Rs.9,40,000] on the basis of image relating to a deal and working of profit found from the mobile of the Assessee. On appeal Ld CIT[A] deleted the addition by observing as follows:

“… 45.5. I have considered the order passed by the AO and the submissions made by the appellant. The AO has held that the said image contains notings with respect to sale of a property in which the appellant was a partner. On perusal of the image, it can be observed that meticulous calculations are made and the mode of payment has also been discussed in detail indicating that the image is not merely a proposed deal but an actual transaction. It is the responsibility of the appellant to prove that the transaction did not take place. The appellant could not provide any documentary evidence to prove that the sale did not take place. The appellant was unable to establish that he has not received profit on the sale of the said property.

45.6 As per the image, there is a clear mention of profit of Rs.9,40,000/- The same has not been offered by the appellant in his return of income. Thus, the same is to be treated as the income of the appellant. The AO has also made an addition of Rs.44,89,200/- on account of sale value of the property. However, only the profit earned on any sale can be added to the income of the appellant and the entire sale consideration cannot be treated as income. Therefore, the addition of unaccounted profit of Rs. 9,40,000/- is confirmed and the balance addition of Rs.44,89,200/- is hereby deleted. Thus, the grounds of appeal no. 8 to 10 are partly allowed.”