ORDER

Girish Agrawal, Accountant Member.- This appeal is filed by the assessee is against the order of CIT(A)/ National Faceless Appeal Centre vide order reference no. ITBA/APL/S/250/2025-26/1081170896(1) dated 25.09.2025, passed against the assessment order by Deputy Commissioner of Income Tax 14(2)(1), Mumbai u/s 143(3) of the Income-tax Act (hereinafter referred to as the “Act”), dated 30.12.2016 for the Assessment Year 2014-15.

2. Assessee has raised the following grounds of appeal:

| 1) |

|

On the facts and in the circumstances of the case and in law, the Ld CIT(A) erred in confirming the action of the Assessing Officer in assessing the total income of the Appellant at Rs. 65,13,58,470 as compared to the total income of Rs. 63,47,95,820 computed by the Appellant in the revised return of income for the said assessment year. |

| 2) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in partly upholding the additions made by the Assessing Officer in the assessment order passed under section 143(3) of the Act. |

| 3) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in upholding the disallowance made under section 14A read with Rule 8D of the Income-tax Rules, 1962, without appreciating that the Appellant had already made a reasonable suo motu disallowance under section 14A read with Rule 8D, considering those investments which actually yielded exempt income during the year under consideration. |

| 4) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of the Assessing Officer in including non-current investments in the subsidiary company, from which no exempt income was earned during the year, while computing the average value of investments under Rule 8D(2)(ii) and Rule 8D(2)(iii). |

| 5) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in upholding the addition of Rs. 19,85,241 to the book profit under section 115JB of the Act on account of the disallowance made under section 14A read with Rule 8D, without appreciating that the provisions of sub-sections (2) and (3) of section 14A read with Rule 8D are applicable only for the purpose of computing the disallowance under section 14A under the normal provisions of the Act, and not for the purpose of computing book profit under section 115JB of the Act. |

| 6) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in confirming the action of the Assessing Officer in treating the capital subsidy of Rs. 30,00,000 received under the incentive scheme announced by the Central Government vide Office Memorandum No. 1(10)/2001-NER dated 07.01.2003 issued by the Ministry of Commerce & Industry (Department of Industrial Policy & Promotion), as a revenue receipt liable to tax. |

| 7) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in not appreciating that the subsidy was granted for establishing a new industrial undertaking in a specified region of Uttarakhand and other states and was specifically intended to encourage capital investment and set-up of industrial units in the notified area, and was therefore capital in nature. |

| 8) |

|

On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in not appreciating that eligibility for the subsidy was directly linked to the investment made in plant and machinery, and that the Appellant had duly reduced the amount of subsidy from the actual cost of plant and machinery and had claimed depreciation only on the reduced cost. |

3. Brief facts of the case as culled out from records are that assessee is a public limited company engaged in the business of manufacturing and sale of packaging material of different types and sizes, manufacturing of metalized films and poly films, labeling material, cartons of different types and manufacturing and sale of packaging machinery, etc. It filed its return of income on 26.11.2014, reporting total income at Rs. 64,63,73,231/- with book profit under section 115JB at Rs. 75,37,67,322/-. Return was revised on 31.03.2016 with revised total income at Rs. 63,47,95,820/- and book profit remaining the same.

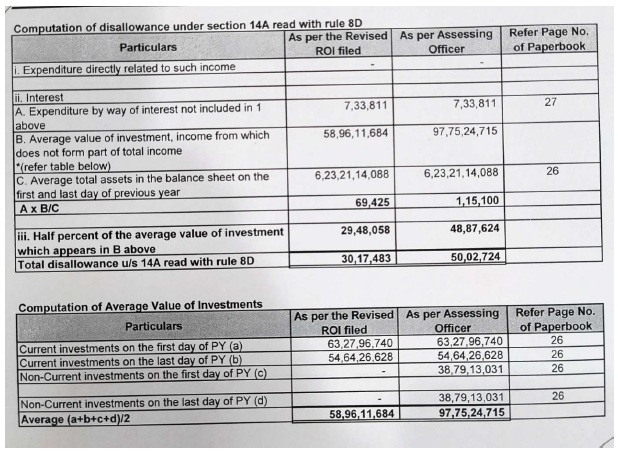

4. In respect of the first issue relating to disallowance made under section 14A r/w Rule 8D of the Income-tax Rules, 1962 (the Rules) for expenditure attributable to earning of exempt income, relevant facts are that assessee had earned dividend income of Rs. 3,26,46,424/-from mutual funds, claimed exempt under section 10(35). Assessee had suo-moto disallowed expenditure of Rs. 30,17,484/- computing it as per the provisions of Rule 8D. Assessee while computing this suo-moto disallowance, considered average value of only those which yielded exempt income. This methodology was adopted in view of decision of the Hon’ble Special Bench of ITAT, Delhi in the case of ACIT v. Vireet Investment (P) Ltd. (Del.) (SB). Hon’ble Special Bench had held that only those investments are to be considered for computing average value of investment which yielded exempt income during the year. Contrary to this, ld. AO observed and held that non-current investment of Rs. 38,79,13,031/- made by the assessee in its subsidiary company Webtech Labels Private Limited ought to have been included while computing the disallowance under Rule 8D. On this, assessee’s contention is that no dividend income was earned from the said investment during the year. Working of disallowance made both, by the assessee and by the ld. AO along with reference to their relevant supporting document which forms part of the paper book on record, is tabulated below for ready reference:

4.1. On the above stated facts and taking into consideration the decision of Hon’ble Special Bench (supra), the issue before us is no longer res integra. The fact that assessee did not earn any exempt income on the non-current investment made by it in its subsidiary is undisputed. Revenue has not brought on record anything to controvert this factual position. Accordingly, stance taken by the ld. AO is contrary to the decision of the Hon’ble Special Bench in the case of Vireet Investment (supra). The incremental disallowance made by the ld. AO of Rs. 19,85,241/- is deleted. Ground nos. 3 and 4 raised by the assessee in this regard are allowed.

4.2. On the same issue relating to disallowance under section 14A r/w Rule 8D, ld. AO had added the same to the book profit under section 115JB for which assessee has raised the issue vide ground no. 5. Contention of the assessee is that the said addition made is without appreciating that the provisions of section 14A are applicable only for the purpose of computing total income under the normal provisions of the Act and not for the purpose of computing book profit under section 115JB. This issue is also no longer res integra and is settled by the decision of Hon’ble Special Bench discussed above in the case of Vireet Investment (supra). It was held that the computation under clause (f) of Explanation 1 of section 115JB(1) is to be made without resorting to computation as contemplated under section 14A r/w Rule 8D. Accordingly, ground no. 5 raised by the assessee is allowed.

5. On the second issue relating to treatment of capital subsidy received by the assessee as revenue in nature amounting to Rs. 30,00,000/-, relevant facts are that assessee received the said subsidy from Directorate of Industries, Uttarakhand under the Central Capital Investment Subsidy Scheme, 2003 announced vide notification dated 08.01.2003 by the Ministry of Commerce and Industries, Government of India. The said subsidy according to the assessee was received on account of setting up of an industrial unit within the designated area in the state of Uttarakhand as a capital investment subsidy granted at the rate of 15% of fixed capital investment made by the assessee subject to a maximum ceiling of Rs. 30,00,000/-. Ld. AO treated the said subsidy as a revenue receipt by observing that the said subsidy was granted for generating employment and therefore, is to compensate employment cost debited in the profit and loss account.

5.1. Contention of the assessee in this regard is that the scheme under which assessee has been granted capital investment subsidy was announced with a view to accelerate industrial development in the concerned state. Reference was also made to CBDT Circular no. 7/2003 dated 05.09.2003 which acknowledged the fact that the Union Cabinet has announced a package of physical and non-physical concessions for the special category states of Himachal Pradesh, Uttarakhand, Sikkim and North-eastern states in order to give boost to the economy in these states. From the said CBDT Circular, reference is made to para 3.1(II) which mentions about eligibility for capital investment subsidy at the rate of 15% of investment made in plant and machinery subject to ceiling of Rs. 30,00,000/-. Even the existing units are entitled to the said subsidy for their substantial expansion.

5.2. Reference is also made to the letter issued by the Directorate of Industries, Uttarakhand dated 22.09.2012 in relation to this subsidy wherein the quantum of subsidy is computed which is based on investment made in the fixed capital towards plant and machinery. Para 3 of this letter is relevant to delve on the issue before us which reflects the intent for which the said subsidy is granted. According to this para, the sanctioned subsidy shall be disbursed upon verification of the fixed assets by the concerned authority and certification of the erection of plant and machinery at site. It also requires a certificate from bank from whom the loan if any, has been obtained for financing the project. The said para 3 form the letter is extracted below:

“The above section subsidy can be disbursed as and when fixed assets are created at factory/unit location duly verified by the concerned G.M. DIC. For claiming the disbursement, G.M. DIC shall also have certifying the value of complete erection of plant and machinery/building works at site. A certificate from the Bank from whom loan has been obtained for financing the project should also be please be furnished.”

5.3. Further, assessee contended that it has reduced amount of subsidy from the gross block of assets, i.e. from the cost of plant and machinery for the purpose of calculating depreciation for the year. Thus, when the cost of plant and machinery itself has been reduced by the amount of this capital subsidy, it has a direct bearing on the quantum of depreciation which is claimed by the assessee at a reduced level, resulting into higher profits reported by it. In other words, indirectly, by charging lower quantum of depreciation on account of reduction in the cost of plant and machinery by the amount of capital subsidy so received, the amount of subsidy is brought to tax, though spread over the number of years. Assessee thus, strongly contended that purpose of subsidy is decisive factor for treating it as capital or revenue in nature. In the present case, it is certainly a capital subsidy as it is granted based on capital investment made by the assessee in plant and machinery.

6. Ld. DR on the other hand referred to the amendment brought in by Finance Act, 2015 wherein clause (xviii) inserted to section 2(24) so as to expressly include subsidy, grants, incentives etc. within the definition of income subject to the exclusions carved out in Explanation 10 to section 43(1) and for grants given towards corpus of trust/institutions. He supported the view taken by the authorities below to uphold the addition so made.

7. We have heard both the parties and perused the material on record. Case before us is prior to the amendment brought in by the Finance Act, 2015. In the present case, the pre-amendment jurisprudence continues to apply whereby the settled position in law is that the nature of a subsidy whether capital or revenue is to be determined by applying the ‘purpose test’. If the object of subsidy is to support the setting up of a new unit or acquisition of a capital asset, it has been held to be capital in nature and consequently not taxable. Conversely, if the subsidy is granted to meet day to day operations, reimbursement, recurring expenses or make business activities profitable, it has been held as revenue in nature and thus, subjected to tax.

7.1. Reference is made to the decision of Hon’ble Supreme Court in the case of

CIT v.

Chaphalkar Brothers [2017]

(SC). In this judgment, Hon’ble Court referred to various judicial precedents including Sahaney Steel and Press Works Ltd. v.

CIT [1997] 2028 ITR 253

(SC), CIT v.

Ponni Sugars and Chemicals Ltd. [2008] 306 ITR 392

(SC). It also dealt with the judgment of Shree Balaji Alloy v.

CIT [2011] 333 ITR 335 (Jammu & Kashmir) wherein subsidy granted was held to be capital in nature. Hon’ble Supreme Court observed on the decision of Shree Balaji Alloy (

supra) that the concessions were issued in order to achieve the twin object of acceleration of industrial development in the state of Jammu & Kashmir and generation of employment. It thus, held that the incentives would be capital and not revenue. It held that the findings of the Hon’ble High Court of Jammu & Kashmir on the fact of incentive subsidy are absolutely correct.

7.2. From the perusal of office memorandum issued by Ministry of Commerce and Industry (Department of Industrial Policy and Promotion), Government of India, dated 07.01.2003 as discussed above, reveals the eligibility for capital investment subsidy at the rate of 15% on the investment made by the assessee in plant and machinery, subject to ceiling of Rs. 30,00,000/-. This subsidy is also available to the existing units on their substantial expansion. This is provided to the assessee for making investment in plant and machinery and not intended for earning from the business. It is for setting up of unit or substantial expansion of the existing business. The purpose of the subsidy so granted to the assessee is clearly spelt out in the office memorandum issued by the Government of India. Also, from perusal of the letter issued by the Directorate of Industries, Uttarakhand, reveals that it has been computed on the quantum of investment made by the assessee in plant and machinery and is subject to certain verification and certification. Furthermore, assessee on its own reduced the subsidy amount from the cost of acquisition of plant and machinery which has a direct bearing on the quantum of depreciation claimed. In the conspectus on the aforesaid discussion on the fact situation, position of law relevant to the year under consideration and judicial precedents referred above, the subsidy received by the assessee is capital in nature and not exigible to tax. Addition made by the ld. AO on this account is deleted. Ground no. 6, 7 and 8 raised by the assessee are allowed.

8. Assessee has also raised an additional ground vide letter dated 11.02.2026 in respect of refund of access Dividend Distribution Tax (DDT) paid by it which is to be restricted to tax rate of 10% under Article 10(2) of the India-Netherlands Double Tax Avoidance Agreement (DTAA). The additional grounds so raised by assessee are reproduced below:

“9. On the facts and in the circumstances of the case and in law, the Ld. CIT(A) erred in not admitting and adjudicating the additional ground raised by the Appellant seeking restriction of Dividend Distribution Tax (“DDT”) under section 115-0 of the Act, to the rate prescribed under Article 10(2) of the India-Netherlands DTAA.

10. In doing so, the Ld. CIT(A):

(a) erred in not appreciating that the dividend paid by the Appellant to Huhtavefa B.V., a tax resident of the Netherlands, is governed by Article 10(2) of the India-Netherlands DTAA, which restricts India’s taxing rights on such dividends to 10% of the gross amount of dividends

(b) failed to appreciate that DDT is, in substance, a tax on the dividend income of the non-resident shareholder, merely collected from the distributing company for administrative convenience, and therefore falls within the expression “income-tax” covered under Article 2 (Taxes Covered) of the DTAA. This principle has been affirmed by the Hon’ble Bombay High Court in case of Colorcon Asia Pvt. Ltd. v. JCIT (2025).

(c) failed to appreciate that, in view of section 90(2) of the Act, the provisions of the DTAA, being more beneficial to the Appellant, override the provisions of section 115-O. Consequently, the levy of DDT at 16.995%, instead of the treaty-mandated rate of 10%, is contrary to the DTAA and also violates the mandate of Article 265 of the Constitution of India, which stipulates that no tax shall be levied or collected except by authority of law.”

9. According to the assessee, admission of the said additional grounds needs no verification of facts and the issue involved is purely question of law and thus, seeks its admission. Since there being no objection on the admissibility of the additional grounds by the Revenue, the same are admitted for adjudication.

10. Before us, ld. Counsel for the assessee placed reliance on the decision of Hon’ble jurisdictional High Court of Bombay in the case of Colorcon Asia (P) Ltd. v. JCIT (Bom) which according to him has settled the controversy in favor of the assessee. In this regard, it is important to take note of the recent development after the conclusion of hearing in the present case before us. Hon’ble High Court of Bombay has referred the issue in the case of Colorcon Asia (supra) which is similar to the one raised by the assessee through its additional ground, to the larger bench. The reference to larger bench is made by the Hon’ble Court to settle the issue of whether the Coordinate Bench decision in Colorcon Asia (supra) reads down the correct position in law or whether it is per incuriam, that is, the same being contrary to the provision of section 115-O, considering the decision of Hon’ble Supreme Court in the case of Godrej and Boyce Manufacturing Company Limited. Subsequent to this reference to the larger bench of the Hon’ble High Court, Hon’ble Supreme Court decided to hear the SLP filed by the Revenue in the case of Colorcon Asia (supra). While admitting the SLP of the Revenue, Hon’ble Supreme Court observed that it is an interesting case and thus, posted the matter for hearing on 13.05.2026. In view of the stated subsequent development after the conclusion of hearing before us, we find it appropriate to remit this particular issue raised by the assessee by way of additional grounds, to the file of ld. Assessing Officer so as to give effect to the issue based on the outcome of the above stated matter pending before the Hon’ble Supreme Court. Needless to say, assessee be given reasonable opportunity of being heard in this regard. Accordingly, additional grounds raised by the assessee are allowed for statistical purposes.

11. In the result, appeal filed by the assessee is allowed.