ORDER

Ms. Padmavathy S, Accountant Member.- These cross appeals by the assessee and the Revenue for Assessment Year (AY) 2017-18 and the appeal of the Revenue for AY 2019-20 are against the order of the Commissioner of Income Tax (Appeals), Chennai-16 (in short “CIT(A)”) passed u/s. 250 of the Income Tax Act, 1961 (in short “the Act”) both dated 13.10.2025.

2. The issue contended by the assessee is with regard to denial of weighted deduction towards capital expenditure as certified by DSIR u/s. 35(2AB) of the Act. The assessee is also contended the issue of allowing the uncertified note u/s. 35(1)(iv) of the Act. The Revenue is challenging the deletion of TP adjustment by the CIT(A) for both the AYs under consideration.

Assessment Year 2017-18:

Assessee’s appeal – ITA No.3462/CHNY/2025

3. The assessee is a company engaged in the business of designing manufacturing and sale of watches, jewellery and eye wear. The assessee filed a return of income for AY 2017-18 on 30.11.2017 declaring total income of Rs.862,47,59,640/-. The case was selected for scrutiny and the statutory notices were duly served on the assessee. Since the assessee had Specified Domestic Transactions (SDP), the A.O made a reference to the Transfer Pricing Officer (TPO) to complete the Arm’s Length Price (ALP) of SDP. The TPO proposed an adjustment towards deduction claimed u/s. 80IC of the Act to the tune of Rs.68,27,55,035/-. The A.O passed draft assessment order incorporating the TP adjustment. The A.O also made disallowance of deduction claimed u/s. 35(2AB) of the Act to the tune of Rs.16,98,45,034/-and also disallowance of provision made on customer loyalty programme amounting to Rs.2,23,74,072/-. The CIT(A) deleted the TP adjustment by placing reliance on the decision of the Coordinate Bench in the assessee’s own case and also based on the decision of the Kolkata Tribunal in the case of Dy. CIT v. Deepak Industries Ltd. (Kolkata – Trib.). On the issue of disallowance u/s. 35(2AB) of the Act, the CIT(A) directed the A.O to provide an opportunity to the assessee to produce Form-3CL and allow the claim as per the amount certified by the DSIR. The CIT(A) also allowed the provision towards customer loyalty programme by placing reliance on the decision of the Hon’ble Supreme Court in the case of Rotork Control Systems Ltd. and the decision of the coordinate bench in assessee’s own case in earlier AYs. Both the assessee and the revenue are in appeal against the order of the CIT(A),

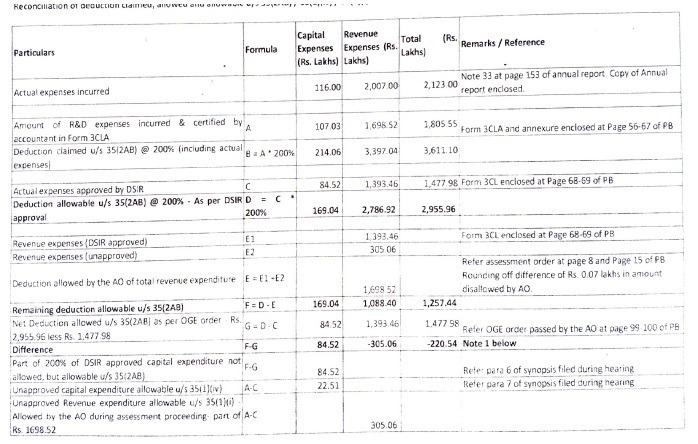

Disallowance of deduction U/s. 32(2AB):

4. The Ld. Authorized Representative (AR) of the assessee submitted the assessee in the return of income has claimed Rs.2.146 Crores towards capital expenditure being 200% of the actual expenditure incurred u/s. 35(2AB) of the Act. In the absence of approval in Form-3CL, the A.O disallowed the entire claim of the assessee. However, the A.O has allowed Rs.16.9852 Crores being 100% of the revenue expenditure claimed by the assessee. The Ld. AR further submitted that DSIR approved in Form-3CL an amount of Rs. 0.8452 Crores towards capital expenditure and a sum of Rs. 13.9346 Crores towards Revenue expenditure and the CIT(A) directed the A.O to allow the deduction claimed as per amount certified in Form-3CL. The Ld. AR also submitted that the A.O in the order giving effect (page 99 & 100 of paper book) has allowed only 100% of the amount as approved by DSIR instead of 200% as per the provisions of Section 35(2AB) of the Act. The Ld. AR drew our attention to the table containing the actual claim, amount certified, amount disallowed and the amount allowed in the order giving effect to submit that the assessee is now contending 100% deduction allowed towards certified capital expenditure instead of 200% which ought to have been allowed as per the provisions of Section 35(2AB) of the Act. The ld. AR also contended that the uncertified amount towards capital expenditure is to be allowed as a deduction u/s. 35(1)(

iv) of the Act and in this regard placed reliance on the decision of the Coordinate Bench in the case of

Ashok Leyland Ltd. v.

ACIT [2025] (

Chennai –

Trib.).

5. The Ld. Departmental Representative (DR), on the other hand, relied on the orders of the lower authorities.

6. We have heard the parties, and perused the material available on record. The assessee has incurred expenditure to the tune of Rs. 1.073 Crores towards scientific research for the year under consideration and has claimed the weighted deduction 200% i.e., Rs.2.146 Crores u/s. 35(2AB) of the Act in the return of income. Out of the amount actually incurred by the assessee a sum of Rs.0.8452 Crores was approved by DSIR in Form-3CL along with the revenue expenditure of Rs.13.9346 Crores towards revenue expenditure. From the perusal of the order giving effect passed by the A.O (page 99 & 100 of paper book), we notice that the A.O while allowing the amount certified by DSIR has only allowed 100% of the amount i.e., Rs. 14.7798 Crores instead allowing 200%. We further notice from the perusal of the table submitted by the assessee which is extracted as below that with regard to the Revenue expenditure the assessee has already been allowed the deduction in excess of the amount allowable u/s. 35(2AB) of the Act.

7. However, with regard to the capital expenditure we notice that the A.O initially had disallowed the entire claim of the assessee and in the order giving effect ought to have allowed 200% of the amount certified i.e, Rs. 0.8542 x 2 = Rs. 1.6904 Crores. Since the A.O in the order giving effect has allowed deduction only to the tune of Rs.0.8452 Crores, we see merit in the contention of the assessee that the A.O has not allowed the deduction at 200% of capital expenditure as per the provisions of the Section 35(2AB) of the Act. Accordingly, we direct the A.O to allow the claim of additional 100% towards capital expenditure as per the amount certified by DSIR in Form-3CL.

8. Now we will consider the issue of the uncertified amount excess claimed towards revenue expenditure and capital expenditure to be allowed u/s. 35(1)(iv) of the Act. In this regard, we notice that the Coordinate Bench in the case of Ashok Leyland (supra) has considered an identical issue where it has been held that:

“4.1 The facts as discernible from the records are that, the assessee had incurred scientific research expenditure, both revenue and capital, at its approved in-house R&D facility. According to the AO, the assessee had claimed weighted deduction of Rs.731,68,77,636/- being 200% of the aggregate expenditure u/s 35(2AB) of the Act. The AO in the course of assessment, had required the assessee to submit the Form 3CL issued by the DSIR, to which the assessee is noted to have submitted that, the DSIR was yet to issue Form 3CL. According to the assessee however, the non-availability of Form 3CL would not prevent it from claiming weighted deduction u/s 35(2AB) of the Act. After considering the submissions of the assessee, the AO is noted to have held that, in absence of Form 3CL, the assessee cannot claim weighted deduction u/s 35(2AB) of the Act.

4.2 The AO thereafter observed that, the assessee had incurred revenue expenditure of Rs.387,57,96,408/-, in relation to which weighted deduction of 200% being Rs.775,50,92,814/- had been claimed as deduction u/s 35(2AB) of the Act. The AO is noted to have held that normal deduction for the revenue expenditure was allowable and therefore disallowed the weighted component of deduction claimed u/s 35(2AB), which was ascertained at Rs.387,57,96,408/-. With regard to the balance R&D expenditure of capital nature of Rs.100,21,22,016/-, the AO noted that, the assessee had claimed weighted deduction at 200% being Rs.200,42,44,032/-. According to the AO, this entire claim was to be disallowed. The AO is noted to have specifically denied the alternate claim raised by the assessee in respect of 100% of capital expenditure u/s 35(1)(iv) of the Act and instead allowed depreciation @ 15% on the capital expenditure being Rs.30,06,36,605/-[Rs.100,21,22,016 X 15%]. The AO accordingly disallowed sum of Rs.557,94,03,835/- (Rs.387,57,96,408/- + Rs.170,36,07,427) u/s 35(2AB) of the Act. Being aggrieved by the order of the AO, the assessee carried the matter in appeal before the Ld. CIT(A).

4.3 It is noted that the Ld. CIT(A) has in principle upheld the action of the AO. However, before the Ld. CIT(A), the assessee brought to his notice that, the AO had made the disallowance u/s 35(2AB) on the erroneous presumption that, the assessee had claimed weighted deduction @ 200%, whereas the assessee had actually claimed weighted deduction @ 150%. The assessee accordingly pointed out that, the AO had made excessive disallowance of Rs.314,04,44,623/-. The Ld. CIT(A) is noted to have found this contention of the assessee to be factually correct and accordingly directed the AO to make necessary correction and modify the disallowance figure to Rs.243,89,59,212/-(Rs.557,94,03,835/- minus Rs. Rs.314,04,44,623). Being aggrieved by the order of the Ld. CIT(A), the assessee is now in appeal before us.

4.4 Having considered the submissions of the assessee, in light of the findings of the lower authorities, we note that, Section 35(2AB) of the Act, provides that, an assessee shall be allowed weighted deduction in relation to expenditure incurred on the in-house R&D facility as approved by the prescribed authority, i.e. DSIR. Sub-clause (4) of Clause (2AB) of Section 35 provides that, the prescribed authority, i.e. DSIR shall submit its report in relation to the approval of the research facility in such Form as prescribed. Rule 6(7A)(b) of the Income-tax Rules, 1962 as amended by the IT(10th Amendment) Rules, 2016 applicable with effect from 01.07.2016 provides that, the approval of expenditure under 35(2AB) of the Act shall be subject to the condition that, the prescribed authority, i.e. DSIR, shall submit its report in Form 3CL to the PCCIT or CCIT. The relevant Rule is reproduced hereunder:

“(7A) Approval of expenditure incurred on in-house research and development facility by a company under sub-section (2AB) of section 35 shall be subject to the following conditions, namely :—

| (a) |

|

The facility should not relate purely to market research, sales promotion, quality control, testing, commercial production, style changes, routine data collection or activities of a like nature; |

| (b) |

|

The prescribed authority shall furnish electronically its report,— |

| (i) |

|

in relation to the approval of in-house research and development facility in Part A of Form No. 3CL; |

| (ii) |

|

quantifying the expenditure incurred on in-house research and development facility by the company during the previous year and eligible for weighted deduction under sub-section (2AB) of section 35 of the Act in Part B of Form No. 3CL; |

| (ba) |

|

The report in Form No. 3CL referred to in clause (b) shall be furnished electronically by the prescribed authority to the Principal Chief Commissioner of Income-tax or Chief Commissioner of Income-tax or Principal Director General of Income-tax or Director General of Incometax having jurisdiction over such company within one hundred and twenty days,— |

| (i) |

|

of the grant of the approval, in a case referred to in subclause (i) of clause (b); |

| (ii) |

|

of the submission of the audit report, in a case referred to in subclause (ii) of clause (b); |

| (c) |

|

The company shall maintain a separate account for each approved facility; which shall be audited annually and a report of audit in Form No. 3CLA shall be furnished electronically to the Secretary, Department of Scientific and Industrial Research on or before the due date specified in Explanation 2 to subsection (1) of section 139 of the Act for furnishing the return of income, for each succeeding year.” |

4.5 In light of the above Rule, as introduced by the IT (10th Amendment) Rules, 2016 applicable with effect from 01.07.2016, the position of law as prevailing in AY 2018-19 is that, furnishing of Form 3CL by DSIR is a pre-requisite to claim the weighted component of deduction u/s 35(2AB) of the Act. The reliance placed by the assessee on the decisions rendered by this Tribunal in their own case in earlier AY 201112 is found to be distinguishable as the AY involved was prior to the insertion of the aforementioned Rule. Accordingly, due to the change in position of law, the aforesaid decision is no longer applicable in the relevant AY 2018-19. For the aforesaid reasons therefore, since the expenditure incurred at the R&D facility was not approved by DSIR in Form 3CL, in light of the restriction set out in Rule 6(7A)(b) of the Income-tax Rules, 1962, the Ld. CIT(A) had rightly denied weighted deduction u/s 35(2AB) of the Act.

4.6 We now come to the alternate claim raised by the assessee for deduction of the capital R&D expenditure of Rs.100,21,22,016/- u/s 35(1)(iv) of the Act. It is noted that, the lower authorities have denied this alternate claim on the ground that, no evidence was provided by the assessee in relation thereto. Before adverting to the facts of the present case, it is noted that Section 35(1)(iv) of the Act, provides that any expenditure of a capital nature on scientific research, related to the business of the assessee shall be admissible as deduction in terms of provision of Section 35(2) of the Act. It is further noted that sub-clause (ia) of Section 35(2) of the Act provides that, where the capital expenditure has been incurred after 31.03.1967, the entire value of capital expenditure is eligible for deduction from the profits of the business. Hence, in our considered view therefore, an assessee is entitled for normal deduction i.e. 100% of the capital expenditure incurred at its R&D facility in terms of Section 35(1)(iv) read with Section 35(2)(ia) of the Act, irrespective whether such capital expenditure is eligible for weighted deduction u/s 35(2AB) of the Act or not.

4.7 Our view finds support from the decision of the Hon’ble jurisdictional Madras High Court in the case of CIT v. Rajapalayam Mills Ltd. In the decided case, the assessee had claimed deduction u/s 35(2AB) of the Act in respect of the expenditure, both revenue and capital, incurred at its R&D facility. Since the assessee was unable to fulfill the conditions prescribed in Section 35(2AB) of the Act, the claim for weighted deduction was denied to it. The assessee had alternatively claimed normal deduction us 35(1)(i) and 35(1)(iv) of the Act in respect of the revenue and capital expenditure respectively. On appeal, this tribunal is noted to have upheld the allowance of deduction at normal rate u/s 35(1) of the Act. On further appeal by the Revenue, we find that the Hon’ble High Court upheld the order of this Tribunal, by holding as under:

“2. The present Appeal has been filed by the Revenue under Section 260-A of the Income Tax Act by raising the following purported substantial questions of law arising from the order passed by the Income Tax Appellate Tribunal dated 31.7.2008, by which the learned Tribunal upheld the order of the learned Commissioner of Income Tax (Appeals) and held that the expenditure incurred by the Assessee on Scientific Research was not entitled to weighted deduction of 1.5 times under Section 35(2AB) of the Act as the Project in question was not duly approved by the Competent Authority, however, the Assessee, was entitled to normal deduction of 100% of expenditure incurred only under Section 35(1)(i) of the Act.

3. The learned Commissioner of Income Tax (Appeals) had discussed the above aspect in his order dated 31.10.2006 as hereunder: —

3.2 After considering the submissions I find that the assessing officer has rightly rejected the claim of the appellant u/s. 32(2AB) as there was no approval from the prescribed authority as on the date of completion of assessment. Having regard to alternative claim, I find that the assessing officer had no occasion to consider the claim of the appellant. In the circumstances, the assessing officer is directed to consider the claim of deduction u/s. 35(1)(i) for Rs. 55,12,558/- representing R&D Revenue Expenditure and deduction u/s. 35(1)(iv) for Rs. 46,387/- representing expenditure incurred for the purchase of Camera used in R&D unit.”

4. However, the Revenue took up the matter before the Tribunal which held against the Revenue on the said aspect of the matter in the following manner:—

“4. After considering the rival submission carefully, we agree that Sec.35(1) as well as Sec.35(2AB) deal with the same expenditure i.e., scientific expenditure consisting of revenue and capital expenditure and only difference is that Sect.35(1) provides for allowance at normal rate i.e., actual expenditure whereas Sec.35(2AB) allows deduction to be claimed at weighted rate of 150% subject to fulfilment of certain conditions. Therefore, we find nothing wrong with the directions of the CIT(Appeals) to the Assessing Officer to allow normal deduction under Sec.35(1) particularly in view of the fact that the Assessing Officer himself has allowed deduction for the Asst. Year 2005-06.”

5. Though there was no issue about the claim of weighted deduction, the Revenue has still preferred the present Appeal under Section 260A of the Act which was admitted by a coordinate Bench of this Court by order dated 9.1.2009, by framing the following substantial questions of law:—

| “(i) |

|

Whether, on the facts and circumstances of the case, the Tribunal was right in law in entertaining a change of claim of deduction by the assessee from 35(2AB) to 35(1) of the Income Tax Act? |

| (ii) |

|

Whether, on the facts and circumstances of the case, the Tribunal was right in granting relief under Section 35(1) when the Assessee has not produced the relevant approval from the prescribed authorities for the claim of deduction?” |

6. Having heard the learned Senior Standing Counsel for the Revenue, we are satisfied that there is no substance in the present Appeal, since the claim of weighted deduction at 1.5 times of the expenditure incurred by the Assessee on Scientific Research was not even decided against the Revenue by the Appellate Authorities, viz., the Commissioner of Income Tax (Appeals) and the Tribunal and therefore, there was no occasion for the Revenue to prefer any further appeal, as the expenditure was allowed only under Section 35(l)(i) of the Act which does not require any approval by the Competent Authority.

7. Since the spending of the amount on Scientific Research itself was not even disputed by the Revenue, in our opinion, the Appellate Authorities have rightly allowed the claim under Section 35(1)(i) of the Act. The Assessee has not preferred any Appeal against that finding and therefore, the question of approval by the Competent Authority for making such claim becomes irrelevant. Therefore, we do not find any substantial question of law to be arising in the present Appeal.

8. We do not find any merit in the present Appeal filed by the Revenue and the same is liable to be dismissed and accordingly, it is dismissed. No order as to costs. A copy of this judgment may be sent to the Assessee forthwith.”

4.8 In view of the above decision supra, the legal position which emerges is that, the denial of weighted deduction u/s 35(2AB) will not disable the assessee from claiming normal deduction for the said R&D expenditure, both revenue & capital, u/s 35(1)(i) and 35(1)(iv) of the Act respectively. Now reverting back to the facts of the present case, it is noted that the assessee had furnished the details of the expenditure incurred at its approved in-house R&D facility before the lower authorities, which was inter alia included in the audited accounts certified by the statutory auditor in Form 3CLA. It was brought to our notice that the assessee vide letter dated 05.03.2021 had furnished the Form 3CLA, which contained the details of R&D expenditure, including expenditure of capital nature, consolidated claim statement, details of disclosure of R&D expenditure in the notes to audited financial statements along with a reconciliation statement between the amount certified in Form 3CLA and the figures reported in notes to audited financial statements. Having perused these details, we find that the details evidencing incurrence of capital expenditure at the approved in-house R&D facility was duly disclosed in the notes to the audited financial statements and further the statutory auditor had verified and certified the same being relatable to scientific research in Form 3CLA. According to us therefore, these contemporaneous evidences sufficiently establish that the capital expenditure of Rs.100,21,22,016/-was incurred in relation to scientific research and was therefore eligible for deduction u/s 35(1)(iv) of the Act. Hence, the order of the lower authorities to that extent stands reversed.

4.9 In view of our above findings therefore, we direct the AO to further allow normal deduction for the capital R&D expenditure of Rs. 100,21,22,016/- u/s 35(1)(iv) of the Act, and resultantly delete disallowance to the extent of Rs.70,14,85,411/- (Rs.100,21,22,016/-minus Rs.30,06,36,605/-). This ground therefore stands partly allowed.”

9. The ratio laid down by the coordinate bench in the above case is that once it is not disputed that the actual expenditure incurred by the assessee is towards scientific research then the amount not certified to be eligible for weighted deduction need to be allowed as a deduction u/s. 35(1)(iv) of the Act. In the given case, the entire amount claimed by the assessee is incurred towards scientific research and this fact has not been disputed. Accordingly, when we apply the above ratio there is merit in the claim of the assessee that the uncertified amount towards capital expenditure and the excess amount allowed u/s. 35(2AB) of the Act is eligible for deduction u /s. 35(1)(iv) of the Act. We therefore directed the A.O to verify the impugned amounts and allow the claim u/s. 35(1)(iv) of the Act.

Revenue’s appeal in ITA No. 159/Chny/2026:

Disallowance u/s. 80IC of the Act:

10. The A.O during the course of assessment proceedings made a reference to TPO for determination of ALP with reference to SDT and the TPO proposed an adjustment of Rs. 78.9015 Crores towards the determination of ALP between the eligible 80IC units and non eligible 80IC units. Accordingly, the A.O disallowed the deduction claimed by the assessee u/s.80IC to the tune of Rs. 68.2755 Crores. The A.O/TPO did not accept the submissions made by the assessee that the profitability in 80IC of the Act eligible units were higher on account of product mix and gross contribution of specific type of jewellery or watch were similar irrespective of the fact whether the product was manufactured by 80IC unit or non 80IC unit. The A.O/TPO also did not accept the submission of the assessee that the inter unit transfers took place at Arm’s length. The CIT(A) deleted the disallowance by holding that:

“5.2.4 The appellant also raised various contentions summarised as follows:

1. TPSR maintained by the Appellant cannot be rejected without cogent reasons

2, The TPO, without finding any inappropriateness in the TP report as required under section 92C(3) of the Act, proceeded to make adjustment to the inter-unit transfers of semi-finished / unfinished products from non-tax holiday unit (Hosur Jewellery and Watch Unit) to tax holiday units (Dehradun Jeweliery unit, Pantnagar Jewellery unit and Pantnagar Watch unit).

3. The TPO has not followed any of the six methods prescribed under section 92C(1) of the Act for computing the arm’s length price.

4. The TPO could have carried out a fresh search only if the comparable drawn by the taxpayer was insufficient or had other deficiency or the data used in computation of ALP is not reliable. Similar views have also been expressed in Circular 12 dated 23 August 2001 issued by the CBDT.

5. The TPO has erred in not considering the economic analysis performed by the Appellant before proposing the above adjustments.

6. The Appellant charges a mark-up of 3% and 10% on the inter-unit transfer of semifinished jewellery and watch components from non 80-IC unit to 80-IC units in Jewellery and Watch segment, respectively.

7. Even if the margins earned on the inter-unit transfers of semifinished / unfinished products are compared with the margins earned by the broadly comparable independent companies from sale of finished products as identified by the Appellant in the respective segment, the inter-unit transfers are at ALP.

8. The profitability of non-80-IC units and 80-IC units depends primarily on product mix of each unit and therefore the profits of the 80-IC units and non 80-1C units could not be compared. Gross margin of various products fetches broadly gross margin in a similar range across all units (80-IC units or non 80-IC units). The reason for higher profitability in the 80-IC is that proportion of high gross margin fetching goods are manufactured in higher proportion and in non 80-1C units higher proportion of goods are manufactured which fetches lesser gross margin. The TPO has adjusted the alleged excess portion of the profit margin in Pantnagar and Roorkee units in line with profit margin of Hosur unit, without appreciating the explanation/submission of the Appellant that the profits of an undertaking is determined by the product mix and therefore there is no intention to shift profits.

9. The profitability from selling of finished goods to unrelated customers will be different from profit derived from selling semi-finished goods to other units.

10. The Ld. TPO has erred in comparing the profit margins of two different products, i.e., Sales of finished goods to third party customers; and Transfer of semi-finished goods to other units of the Appellant Company.

5.2.5 1 have considered the appellant’s submissions. On examination of the material on record, it is seen that the TPO has rejected the transfer pricing study of the appellant for the reason that the Tax Holiday Units have made more profits when compared to the appellant’s ineligible units, As heid in DCIT v. Deepak Industries Ltd (Kolkata-Trib), mere extraordinary profit cannot be criteria for adjustment in the transfer price. In the appellant’s own case in ITA No.393 and IT(TP)(A) No.89/Chny/2018 dated 19-09- 2025 for AY 2013-14 & 2014-15, the Hon’ble Tribunal held as under:

“It is an undisputed fact that the assessee had undertaken a detailed transfer pricing study and adopted the Transattional Net Margin Method (TNMM) as the Most Appropriate Method to benchmark its inter-unit transactions. The TPO has not pointed out any specific defects in the TP documentation as required under section 92C(3) of the Act before proceeding with the adjustment. The TPO’s approach of comparing net margins of tax holiday units with non tax holiday units, without considering differences in product mix. Production processes and market dynamics is not in accordance with established transfer pricing principles. It is well settled that comparability adjustments must be made where differences materially affect the profitability. The assessee has furnished segmental profit and loss accounts duly certified by an Independent Chartered Accountant, which demonstrale that the variation in profit margins is due to product mix and not due to profit shifting. This crucial evidence has been disregarded by the Ld.DRP. Further, the adjustment pertains to interunit transfers of semi finished and unfinished products, while the TPO has benchmarked these against margins earned on third party sales of finished goods, which are not comparable transactions. The Ld.DRP has simply followed the directions of the previous year without applying its mind to the facts of the current year, which is not acceptable in law.

In view of the above discussion and case law referred, we are of the considered opinion that the TP adjustment made by the TPO and sustained by the Ld. DRP is not sustainable. Accordingly, the adjustment of Rs.63,17,601/-for AY 2014-15 is deleted”.

11. We have heard the parties, and perused the material available on record. From the perusal of the above observation of the Coordinate bench as relied on the by the CIT(A), we notice that the Coordinate bench has been consistently deleting the disallowance on the ground that the segmental profits are duly certified by independent C.A and benchmarking done by the TPO against the margins earned on third party sale of finished goods is not correct. For the year under consideration, the Revenue did not bring any new material to contend that the facts for the year under consideration are different from earlier years. Therefore, in our considered view the ratio laid down by the Coordinate Bench in assessee’s own case for AY 2013-14 and 2014-15 are applicable for the year under consideration also. Accordingly, we see no infirmity in the decision of the CIT(A) in deleting the disallowance towards deduction claimed u/s. 80IC of the Act.

Assessment year 2019-20 in ITA No.159/CHNY/2026

12. The facts in Revenue’s appeal for AY 2019-20 are identical and therefore our above decision with regard to the issue of disallowance of deduction u/s. 80IC of the Act in AY 2017-18 (refer above finding) is mutatis mutandis applicable for AY 2019-20 also. We therefore see no reason to interfere with the decision of the CIT(A) in deleting the disallowance u/s. 80IC of the Act for AY 2019-20 also.

13. In the result, the appeal of the assessee for AY 2017-18 is allowed and the appeals of the Revenue for AY 2017-18 & 2019-20 are dismissed.