ORDER

Dr. Manish Borad, Accountant Member.- The captioned appeals at the instance of assessee pertaining to A.Yrs. 2018-19 and 2020-21 are directed against the separate orders dated 07.11.2025 & 20.11.2025 framed by National Faceless Appeal Centre, Delhi passed u/s.250 of the Income Tax Act, 1961 arising out of respective Assessment orders dated 15.03.2021 and 27.09.2022 passed u/s.143(3) r.w.s.143(3A) & 143(3B)/143(3) r.w.s.144B of the Income Tax Act, 1961.

2. Assessee has raised common grounds of appeal in both the assessment years. We will first take up the appeal for A.Y. 2018-19 as the lead case and the grounds of appeal raised by the assessee reads as under :

“In this regard, the Appellant wishes to raise the following grounds of appeal, which are independent and without prejudice to each other:

1. Ground 1: Challenging the addition imputed applying the provisions of Rule 8D of the Income Tax Rules, 1962

1.1 The learned AO and the learned CIT(A) grossly erred in applying the provision of Rule 8D to compute expenses in relation to exempt income under the provisions of section 14A of the Act.

1.2 The learned AO and the learned CIT(A) ought to have appreciated that the disallowance computed by the Assessee is after considering attributable direct and indirect expenses (including obtaining a certificate for allocation of indirect cost) and is most reasonable having regard to the minimal efforts involved in making and maintaining investments yielding exempt income, which are in the nature of long-term debt securities.

2. Ground 2: Imputing addition under Rule 8D without recording objective satisfaction

2.1 The learned AO and the learned CIT(A) has grossly erred in imputing disallowance as per Rule 8D without recording objective satisfaction as per the mandate of the provisions of section 14A(2) of the Act.

2.2 The learned AO and the learned CIT(A) ought to have appreciated that the application of Rule 8D is not automatic and essentially requires recording of objective satisfaction as to how the disallowance computed by the Assessee is unreasonable having regard to the accounts of the Assessee.

3. Ground 3: Challenging the reliance placed on earlier assessments without appreciating that the facts are distinguishable

3.1 The learned AO and the learned CIT(A) ought to have appreciated that application of Rule 8D in past years in Assessee’s own case does not affirm its application automatically in subsequent years, especially having regard to the fact that the manner in which disallowance is suo-motu computed by the Assessee for the year under consideration is more comprehensive as compared to the manner in which the same was being computed in the earlier years.

The Appellant prays that the addition sustained by the learned CIT(A) ought to be deleted.

The Appellant craves leave to add, alter, vary, omit, substitute or amend the above grounds of appeal, at any time before or at, the time of hearing of the appeal, so as to enable the Hon’ble Tribunal to decide this appeal according to the law.”

3. Since identical issues have been raised in both the assessment years under appeal, our decision taken in appeal for A.Y. 2018-19 would apply mutatis mutandis for A.Y. 202021.

4. At the time of hearing, ld. Counsel for the assessee requested for not pressing the common ground No.2 raised by the assessee in both the appeals and therefore the said ground is dismissed as ‘not pressed’.

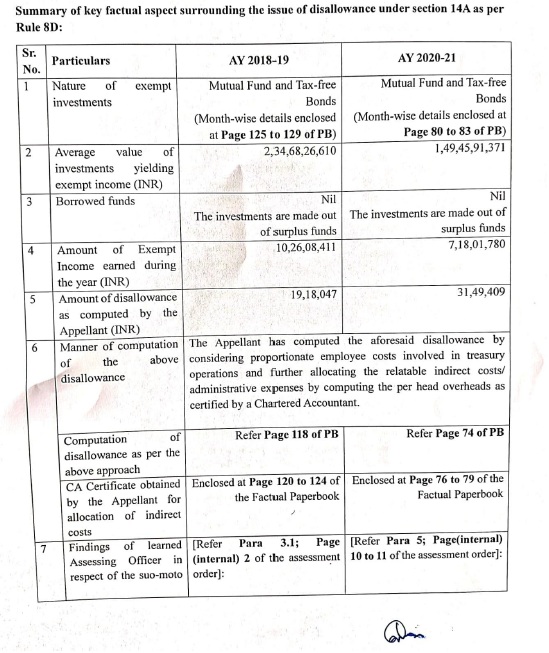

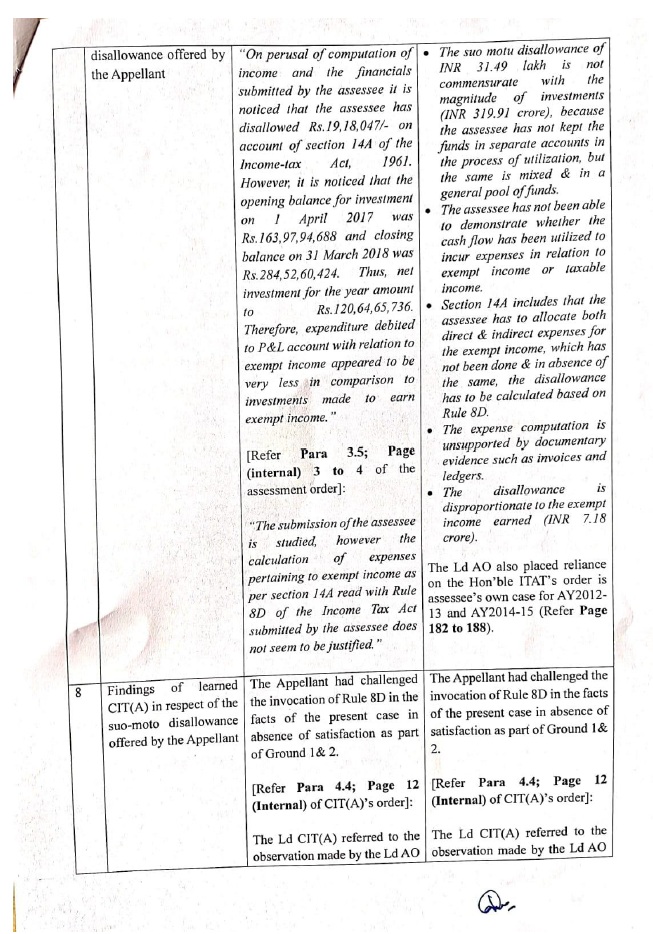

5. Brief facts of the case are that the assessee is a Limited Company. Income of Rs.116,39,31,340/- declared in the return of income for A.Y. 2018-19 e-filed on 31.03.2019. Case selected for Complete Scrutiny. Valid notices u/s.143(2) and 142(1) of the Act were served on the assessee. Ld. Assessing Officer on examining the issue of disallowance u/s.14A r.w. Rule 8D of the Income Tax Rules, 1962 observed that the assessee has suo motu disallowed Rs.18,18,047/-. Ld. Assessing Officer further examined details of average investments, referring to provisions of section 14A and also deal with calculation of suo motu disallowance by the assessee with regard to direct and indirect expenses. Ld. Assessing Officer also took note of Rule 8D(2)(ii) which provides for calculating the disallowance u/s.14A @1% of the Annual average of the monthly average of the opening and closing balances of the value of investment income and calculated the same at Rs.2,43,81,472/-. Further, ld. Assessing Officer gave the benefit of suo motu disallowance of indirect expenses at Rs.6,62,352/- against the disallowance calculated under Rule 8D(2)(ii) of the Act and concluded the assessment proceedings making disallowance u/s.14A at Rs.2,37,19,120/- and assessed the income at Rs.118,76,54,060/-.

6. Aggrieved assessee preferred appeal before ld.CIT(A) but failed to succeed. Now the assessee is in appeal before this Tribunal.

7. Ld. Counsel for the assessee vehemently argued referring to summary of key facts which also included the issues raised against non-recording of satisfaction which has not pressed during the course of hearing :

8. On the other hand, ld. DR supported the order of ld.CIT(A).

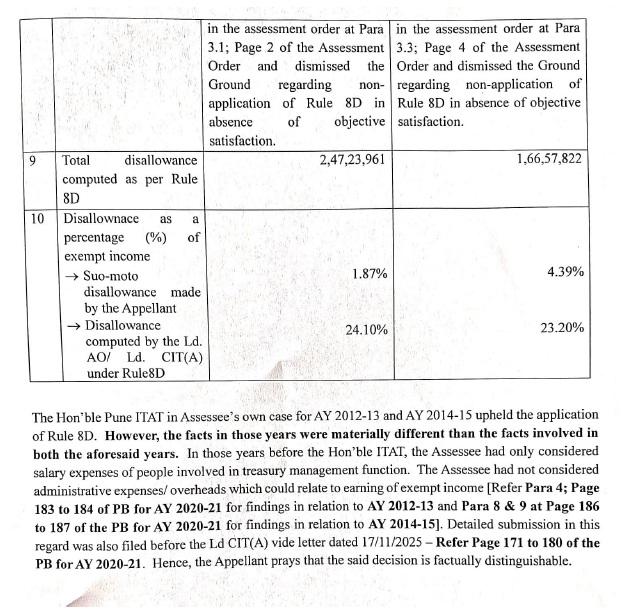

9. We have heard the rival contentions and perused the record placed before us. The common issue raised for A.Ys. 2018-19 and 2020-21 is against the disallowance u/s.14A of the Act. Though the assessee has referred to the decision of the Tribunal dealing with issue of disallowance u/s.14A of the Act for A.Y. 2012-13 and 2014-15, however, since Rule 8D has been amended w.e.f. 02.06.2016, the decisions rendered by this Tribunal for A.Y. 2012-13 and 2014-15 on the quantification of disallowance u/s.14A of the Act will not be applicable on the instant appeals.

10. So far as the A.Y. 2018-19 concerned, we note that the assessee has calculated the disallowance u/s.14A of the Act out of the direct expenses at Rs.12,55,695/- and indirect expenses at Rs.6,62,352/-. So far as disallowance out of direct expenses is concerned, there is no dispute at the end of both the parties. As regards the indirect expenses disallowance is concerned, Rule 8D(2)(ii) provides that an amount equal to 1% of the Annual average of the monthly average of the opening and closing balance of the value of investment, income from which does not or shall not form the part of total income needs to be disallowed u/s.14A of the Act. The amount so calculated under Rule 8D(2)(ii) of the Act takes care of the indirect expenses which have a bearing on the investments fetching exempt income.

11. Before us, ld. Counsel for the assessee submitted that major portion of the average investments is in Mutual Funds and Tax Free Bonds. It is an admitted fact that when the investments are made in the Mutual Funds the companies running the Mutual Funds charges the investors on a periodical basis and such charges are levied for taking care of the investments and switching them from one fund to another or one Equity to Another Equity so as to get the maximum return on the investments. In other words, the assessee had already incurred the expenses for making investment in Mutual Funds. Similar is the situation for Tax Free Bonds where the investments made does not require regular watch by an investor team because the Tax Free Bonds are there for a particular period and at the end of such period the bonds are redeemed and the Tax Free income is received. Therefore for the purpose of calculating the Annual average of the monthly average of the opening and closing balance of the value of investments the amount invested in Mutual Funds and Tax Free Bonds are to be excluded.

12. We therefore under the given facts and circumstances of the case are of the considered view that for the purpose of calculating the disallowance under Rule 8D(2)(ii) of the I.T. Rules for the indirect expenses incurred for earning the exempt income, ld. Jurisdictional Assessing Officer is directed to calculate @1% of the Annual average of the monthly average of the opening and closing balances of the value of investments excluding the investments made in Mutual Funds and Tax Free Bonds. Details to this effect for proper and correct calculation shall be placed by the assessee before the ld. JAO for necessary verification for which reasonable opportunity of hearing shall be provided to the assessee.

13. We also want to make it clear that in case the calculation under Rule 8D(2)(ii) of the I.T. Rules does not exceed the suo motu disallowance of indirect expenses made by the assessee, then no further disallowance deserves to be made under Rule 8D(2)(ii) of the I.T. Rules and in case it exceeds then the assessee should be allowed the deduction for the indirect expenses suo motu offered for disallowance. We order accordingly and allow Ground No.3 for statistical purpose. Appeal of the assessee for A.Y. 2018-19 is partly allowed for statistical purposes.

14. Now we take up ITA No.436/PUN/2026 for A.Y. 2020-21. Since facts and issues are identical to that ITA No.474/PUN/2026 of A.Y. 2018-19 Our decision taken hereinabove in for A.Y. 2018-19 shall hold good mutatis mutandis to the appeal for A.Y. 2020-21 as well.

15. In the result, both the appeals of the assessee are partly allowed for statistical purposes.