Adjustments retained in a final assessment order must be adjudicated on merits during appeals.

Issue

Whether the Commissioner (Appeals) is legally justified in refusing to decide the merits of a tax adjustment simply because the assessee did not file a separate appeal against the initial Section 143(1) intimation, even though that same adjustment was formally carried forward and retained in the final Section 143(3) scrutiny assessment order.

Facts

-

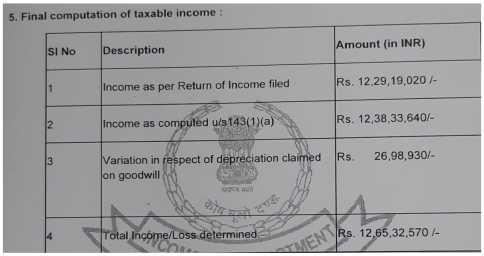

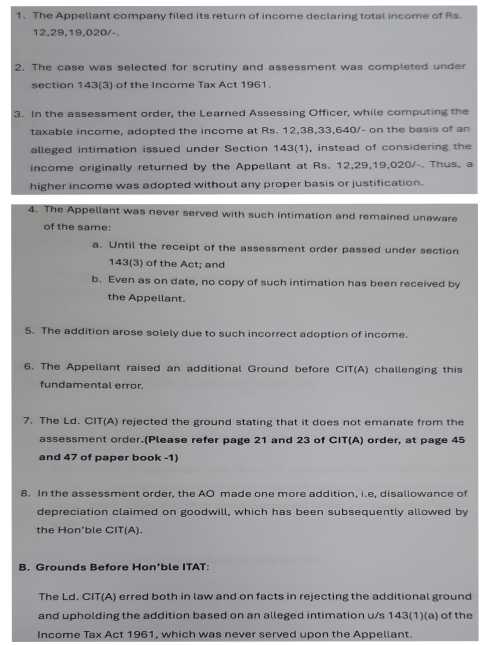

The case of the assessee was scrutinized for Assessment Year 2020-21.

-

An initial tax adjustment amounting to ₹9.14 lakhs was made against the assessee in the automated intimation issued under Section 143(1).

-

The assessee did not file an independent appeal against this initial Section 143(1) intimation.

-

Subsequently, the regular scrutiny assessment proceedings were completed, and the Assessing Officer formally retained the exact same ₹9.14 lakh adjustment in the final assessment order passed under Section 143(3).

-

The assessee filed an appeal challenging the final Section 143(3) assessment order before the Commissioner (Appeals).

-

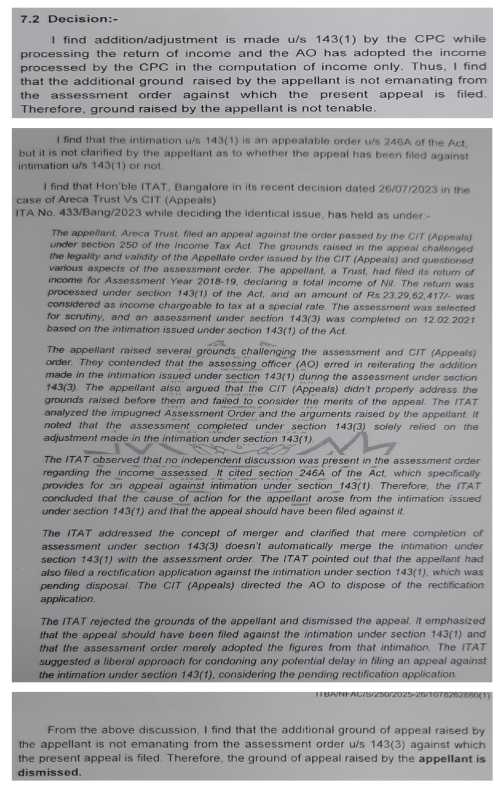

The Commissioner (Appeals) dismissed the challenge and declined to evaluate the merits of the ₹9.14 lakh addition, ruling that the issue was barred because no appeal had been filed against the original Section 143(1) intimation.

Decision

-

The order of the Commissioner (Appeals) is set aside, and the specific dispute regarding the ₹9.14 lakh adjustment is remanded back to his file.

-

Even if an assessee chooses not to appeal against an initial Section 143(1) intimation, they retain the full legal right to contest that adjustment if it is subsequently incorporated and sustained in a final Section 143(3) assessment order.

-

The Commissioner (Appeals) is legally required to examine and decide the dispute on its actual commercial and statutory merits.

-

The First Appellate Authority is directed to pass a comprehensive, reasoned speaking order on the merits after giving the assessee a fair and reasonable opportunity to present their case.

Key Takeaways

-

Scrutiny Orders Absorb Prior Intimations: A Section 143(1) intimation is a preliminary automated processing step. Once a formal scrutiny assessment is initiated and a final order is passed under Section 143(3), the preliminary findings merge into the final order. An omission to appeal at the preliminary stage does not strip a taxpayer of their right to contest the final assessment.

-

Appellate Authorities Cannot Avoid Merits on Technicalities: The First Appellate Authority is a court of fact and law. It cannot summarily dismiss a substantive grievance regarding tax additions based on procedural technicalities if the final, actionable tax demand arises out of a scrutiny assessment order.

and Anadee Nath Misshra, Accountant Member

[Assessment year 2020-21]

| (i) | Application for rectification of Intimation issued under section 143(1) of the Act; under section 154 of the Act. |

| (ii) | Appeal against the refusal to carry out rectification under section 154 of the Act. [If the assessee’s remedy exercised under (i) above is unsuccessful] |

| (iii) | Direct appeal against the intimation under section 143(1) of the Act, under Chapter-XXA of the Act. |

| (iv) | Appeal against the assessment order, under Chapter XXA of the Act; if the adjustment made under section 143(1) of the Act is retained in the assessment order. |

| (v) | Revision petition under section 264 of the Act. |