ORDER

Ravish Sood, Judicial Member.- The present appeal filed by the assessee company is directed against the order passed by the Assessing Officer (for short, “AO”) under section 143(3) r.w.s 144C(13) of the Income Tax Act, 1961 (for short, “the Act”), dated 30/06/2022 for the Assessment Year (AY) 2018-19. The assessee company has assailed the impugned order on the following grounds of appeal:

“Based on the facts and circumstances of the case and in law, the Ld. Assessing Officer (“Ld. AO”)/ Ld. Transfer Pricing Officer (“Ld. TPO”)/ Hon’ble Dispute Resolution Panel (‘Hon’ble DRP’) grossly erred in –

1. General Ground for TP adjustments

By not accepting the economic analysis undertaken by the Appellant in accordance with the provisions of the Act read with the Income Tax Rules, 1962 (“Rules”) and modifying /undertaking fresh analysis while determining the arm’s length price and in doing so making an adjustment of INR 8,10,59,589 to the international transactions.

Ground no 2 Adjustment of INR 5,07,10,089 pertaining to international transaction of provision of contract R&D services and of INR 45,77,985 pertaining to international transaction of provision of contract manufacturing services.

2. Ground against rejection of certified segmental financial information

| (a) |

|

Not considering certified segmental financials information submitted by the Appellant. |

| (b) |

|

Without prejudice, not considering segmental margins as per audited financial statements |

Ground no 3-11- Without prejudice grounds for adjustment of INR 5,07,10,089 pertaining to international transaction of provision of contract R&D services and of INR 45,77,985 pertaining to international transaction of provision of contract manufacturing services.

3. Ground against applying arbitrary filters without any rationale

Inter-alia use of the following additional/ modified filters in undertaking the comparative analysis and selecting dissimilar companies/ rejecting comparable companies:

| (a) |

|

Different financial year-end filter; |

| (b) |

|

25 percent export earnings filter; |

| (c) |

|

Related party transaction filter; |

| (d) |

|

Persistent losses filter; |

| (e) |

|

Super normal profits filter |

4. Ground against erroneous functional characterization of the Appellant in relation to contract R&D services.

Not appreciating the functional profile of the Appellant and drawing an erroneous conclusion that the Appellant is engaged in providing high-end research services.

5. Ground against selection of uncomparable companies for contract R&D services

Not undertaking an objective comparative analysis and inter alia selecting the following companies as comparable to the Appellant’s contract R&D services, which are functionally not comparable to the Appellant:

| (a) |

|

GVK Biosciences Private Limited; |

| (b) |

|

Veeda Clinical Research Private Limited |

6. Grounds against rejection of comparable companies for contract R&D services

Not undertaking an objective comparative analysis and inter alia rejecting comparable companies as not comparable to the Appellant’s contract R&D services, which are functionally comparable and/ or qualify all the filters and hence should not be rejected.

7. Ground against selection of uncomparable companies for contract manufacturing services

Not undertaking an objective comparative analysis and inter alia selecting companies as comparable to the Appellant’s contract manufacturing services, which are functionally different and/or do not qualify all the filters and hence should be rejected.

8. Grounds against rejection of comparable companies for contract manufacturing services

Not undertaking an objective comparative analysis and inter alia rejecting comparable companies as not comparable to the Appellant’s contract manufacturing services, which are functionally comparable and/or qualify all the filters and hence should not be rejected.

9. Ground against erroneous computation of margins

Not considering export incentives, scrap sales and reversal of provision for doubtful advances as operating item while determining margin of the Appellant.

10. Grounds pertaining to adjustments to risk differences.

Not adjusting the net margins of comparable companies for functional and risk differences in accordance with the provisions of rule 10B(1) (e) of the Rules.

11. Grounds pertaining to working capital adjustments

Not adjusting the net margins of comparable companies for differences in working capital in accordance with the provisions of rule 10B(1)(e) of the rules.

12. Grounds pertaining to mark-up on reimbursements Adjustment of INR 5,16,290

| (a) |

|

Imputing mark-up amounting to INR 5,16,290 at the rate of 5% on reimbursement of expenses by AEs without appreciating that the same were recovered on a cost-to-cost basis |

| (b) |

|

Without prejudice, not undertaking any analysis to determine the ALP of the reimbursement transaction and marking up at the rate of 5% on ad-hoc basis. |

13. Grounds pertaining to interest on ECBs – Adjustment of INR 55,38,762

| (a) |

|

Rejecting the benchmarking rate adopted by the Company without providing reasons and making an adjustment by considering the ALP rate of interest at LIBOR plus 200 bps (b) Considering the analysis more favorable to the Revenue, without substantiating reason, which is also resulted in cherry picking for determining the arm’s length price of the impugned transaction. |

| (c) |

|

Not following any statutorily prescribed method and without doing any comparability benchmarking as prescribed under Chapter X of the Act. |

| (d) |

|

Without prejudice, LIBOR + 300 bps rate of interest is also held to be at arm’s length by various judicial precedents. |

| (e) |

|

Without prejudice to our contention (against contradictory and inconsistent action of Ld. TPO in considering SBI rates to benchmark outstanding receivables) that SBI interest rates are not comparable to benchmark foreign currency loans/ receivables, we request that a uniform approach needs to be followed for benchmarking both the transactions. |

14 .Grounds against imputing interest on outstanding receivables due from AEs – Adjustment of INR 1,97,16,463

| (a) |

|

Not appreciating that outstanding receivables is not covered in the definition of international transaction as defined u/s 92B of the Act in the facts and circumstances of the case; |

| (b) |

|

Not appreciating that the receivables are consequential/closely linked to the principal transaction of contract R&D services and contract manufacturing services and hence have been aggregated for determination of ALP under TNMM, |

| (c) |

|

Not appreciating the fact that the working capital adjustments undertaken take into account the impact of outstanding receivables of the controlled transactions vis-a-vis the uncontrolled transactions in determining the arm’s length margin and no separate benchmarking is required; |

| (d) |

|

Not appreciating the facts and circumstances surrounding the receivables and re-characterising the outstanding receivables as unsecured loans advanced to AES: |

| (e) |

|

Not following any statutorily prescribed method and without doing any comparability benchmarking as prescribed under Chapter X of the Act. |

| (f) |

|

Not appreciating the fact that the Appellant does not to collect interest on outstanding receivables from customers (both AEs & Non – AEs). |

| (g) |

|

Not appreciating that the Appellant does not pay interest on outstanding payables to AEs. |

15 .Without prejudice grounds against imputing interest on outstanding receivables due from AEs – Adjustment of INR 1,97,16,463

| (a) |

|

Not appreciating that the receivables due from oversees AEs are in foreign currency and hence interest, if any, is to be benchmarked with the rates prevalent in the international market for foreign currency loans; |

| (b) |

|

Considering ad-hoc credit period of 30 days instead of the industry average credit period |

| (c) |

|

Not considering netting off of outstanding receivables and payables from/to AEs; |

| (d) |

|

Not following method of computation as held by Hon’ble ITAT in Assessee’s own case for AY 2013-14 and AY 2014-15 |

16 . Ground pertaining to brought forward business losses

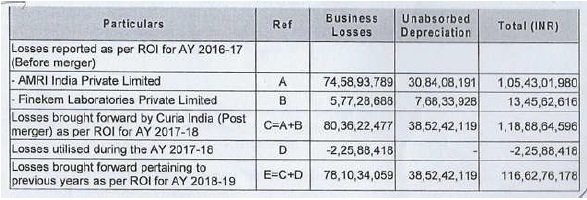

Not adjusting brought forward business losses pertaining to previous years of INR 116,62,76,178 against the business income computed after making the transfer pricing adjustment of INR 8,10,59,589

17 . Ground on erroneous initiation of penalty under section 270A of the Act

Ld. AO was not justified and rather grossly erred in law and in facts by initiating penalty proceedings under section 270A of the Act by falsely stating that the Assessee has under-reported the income.”

2. Succinctly stated, the assessee company, which is a wholly owned subsidiary of “Curia Group” that was set up to provide R&D services in the field of medicinal chemistry to the Associate Enterprises (AEs), had e-filed its return of income for AY 2018-19 on 30/11/2018, declaring NIL income. The case of the assessee company was selected for scrutiny assessment through CASS, and a notice under section 143(2) of the Act, dated 22/09/2019, was duly issued and served upon the assessee company.

3. During the course of the assessment proceedings, the AO made a reference under section 92CA(1) of the Act to the Transfer Pricing Officer (for short, “TPO”) for computing the Arm’s Length Price (ALP) in relation to the international transactions of the assessee company as detailed in its audit report in Form No.3CEB.

4. The TPO, vide his order passed under section 92CA3) of the Act, dated 31/07/2021, suggested the adjustment of Rs. 8,15,75,879/-, as under:

| SI. No. |

Particulars |

Amount (Rs.) |

| 1. |

Adjustment towards contract Research and Development services |

5,07,10,069/- |

| 2. |

Adjustment towards provision of contract manufacturing services |

45,77,985/- |

| 3. |

Adjustment towards interest on External Commercial Borrowings (ECBs) |

55,38,762/- |

| 4. |

Reimbursement of expenses received from AEs |

10,32,580/- |

| 5. |

Adjustment towards interest on outstanding receivables |

1,97,16,463/- |

5. Thereafter, the AO, based on the order received from the TPO under section 92CA(3) of the Act, dated 31/07/2021, wherein he proposed an adjustment of Rs. 8,15,75,879/-, passed a draft assessment order under section 143(3) r.w.s 144C of the Act, dated 31/08/2021.

6. Aggrieved, the assessee company objected to the draft assessment order passed by the AO under section 143(3) r.w.s 144C of the Act, dated 31/08/2021 before the Dispute Resolution Panel-1, Bangalore (for short, “DRP”), which upheld all the adjustments made by the TPO except for the transaction of reimbursement of expenses received from AEs wherein it gave a partial relief to the assessee company by directing the AO/TPO to adopt markup of 5% on reimbursement cost instead of the higher rate proposed by the TPO.

7. The AO, pursuant to the directions of the DRP under section 144C(5) of the Act, dated 16/05/2022, scaled down the TP adjustment of Rs. 8,10,59,589/- and vide his order passed under section 143(3) r.w.s. 144C(13) of the Act, dated 30/06/2022 determined the income of the assessee company at Rs.7,49,54,409/-.

8. The assessee company, aggrieved with the order passed by the AO under section 143(3) r.w.s 144C(13) of the Act, dated 30/06/2022, has carried the matter in appeal before us.

9. We have heard the Learned Authorized Representatives of both parties, perused the orders of the authorities below and the material available on record, as well as considered the judicial pronouncements that have been pressed into service by them to drive home their respective contentions.

10. Ms. Ananya Kapoor, Advocate, Learned Authorized Representative (for short, “Ld. AR”) for the assessee company, at the threshold of hearing of the appeal, took us to the respective issues based on which the impugned assessment order has been assailed before us.

11. Apropos the TP adjustment of the contract research and development services made by the AO pursuant to the directions of the TPO, the Ld. AR submitted that the AO/TPO had grossly erred in law and on the facts of the case by failing to consider the certified segmental financial information submitted by the assessee company in its Transfer Pricing Study Report (TPSR). Alternatively, the Ld. AR submitted that, even otherwise, the AO/TPO had erred in failing to consider the segmental margins as per the audited financial statements of the assessee company. Elaborating on her contention, the Ld. AR submitted that the assessee company had submitted the segmental results in its TP documentation, which is certified by a Cost and Management Accountant. Elaborating further on her contention, the Ld. AR submitted that, based on its aforesaid refined approach, the assessee company had prepared the segmental results which presented a true and fair view of its operations. The Ld. AR submitted that the assessee company had allocated the costs by identifying the same for the respective segments, while for the balance were allocated based on the most relevant allocation keys, viz., FTE hours for the R&D segment, machine hours for the API segment, and turnover basis for a few expenses. The Ld. AR submitted that the TPO had summarily rejected the segmental results provided by the assessee company in its TP documentation without pointing out any defect/deficiency. The Ld. AR submitted that the TPO, after rejecting the method adopted by the assessee company to allocate the cost, had thereafter allocated it on a revenue basis, which, thus, had resulted in the same profitability across all segments, leading to the incorrect conclusion that the non-AE segment and the AE segment were equated. The Ld. AR vehemently submitted that it is incomprehensible how the allocation of costs on a revenue basis, which would result in the same profitability for all segments, could lead to a correct view. The Ld. AR, to buttress her contention, took us through the TP documentation and the TPO’s observations on the aforesaid issue, which were thereafter upheld by the DRP. The Ld. AR submitted that the only reason given by the TPO for rejecting the method adopted by the assessee company was that the audited financial results did not match the segment results. Elaborating further on her contention, the Ld. AR submitted that the assessee company had given a detailed reason for the aforesaid impugned discrepancy, which, however, had been ignored by the TPO/DRP. The Ld. AR to buttress her contention had taken us through the reply filed by the assessee company in response to notice, dated 22/07/2021 with the TPO, wherein it had stated that the segment result provided in the TP documentation, certified by a Cost and Management Accountant are much detailed and accurate as business segment wise, AE and non-AE expenses are bifurcated, while for in the audited financials, the mandate of AS-17 has alone been followed, which refers to related party and non-related parties only without going into each business segment wise, Pages-480-481 of APB. The Ld. AR submitted that, even if it was to be assumed that the audited financials were incorrect, the segment result provided in the TP documentation, certified by a Cost and Management Accountant, could not have been rejected.

12. Alternatively, the Ld. AR submitted that if the TPO were to reject the segment provided in the TP documentation, the segmental margins as per the audited financial statements should have been considered. The Ld. AR to buttress her contention had relied upon various judicial pronouncements/orders, viz. (

i) Hon’ble High Court of Delhi order in

Pr. CIT v.

Nalwa Steel & Power Ltd. [2024] (Delhi)/ITA 725/2019, dated 06/03/2024; (

ii) the order of the ITAT,

Hyderabad in

TPSC (India) (P.) Ltd. v.

Dy. CIT [2024] (

Hyderabad –

Trib.)/ITA (TP) No.225/Hyd/2022, dated 18/03/2024; and (

iii) the order of the ITAT, Mumbai Bench in

Mylan Pharmaceuticals Private Ltd. v.

ACIT [IT Appeal No. 2209 (Mum) of 2017, dated 20-3-2020].

13. Coming to the second issue, i.e., TP adjustment regarding the payment of interest on External Commercial Borrowings (ECBs), the Ld.AR submitted that the assessee company had benchmarked the said transaction by considering the ALP rate of interest at LIBOR + 3%. However, the TPO had rejected the benchmarking of the assessee company and, on an ad hoc basis, taken it at LIBOR + 2%. The Ld. AR submitted that the ad hoc rejection of the benchmarking of ALP by the TPO/DRP is not permissible in law. Elaborating on her contention, the Ld. AR submitted that the TPO/DRP had not brought anything on record that substantiates that LIBOR + 2% would be the ALP of the subject international transaction. The Ld. AR, in her attempt to justify the ALP rate of interest at LIBOR + 3% adopted by the assessee company, submitted that as it was lower than the ceiling rate prescribed by the RBI, the transaction can safely be concluded to be at Arm’s Length. However, the Ld. AR to support her contention relied upon the judgment of the Hon’ble High Court of Karnataka in

CIT v.

GE India Technology Center Pvt. Ltd. [IT Appeal No. 282, dated 17-12-2020]. Apart from that, the Ld. AR had relied upon certain orders of the coordinate Benches of the Tribunal, viz.,

Dy. CIT v.

Devgen Seeds & Crop Technology (P.) Ltd. (

Hyderabad –

Trib.)/ITA No.399/Hyd/2016, dated 24/03/2017; (

ii)

Goodyear South Asia Tyres (P.) Ltd. v.

Asstt. CIT [2017] (Mumbai –

Trib.)/ITA No. 7715/Mum/2012, dated 26/10/2016; and (

iii).

Asstt. CIT v.

Firestone International (P.) Ltd. [2018] (Mumbai –

Trib.)/ ITA No.5471/Mum /2014, dated 13/04/2016. The Ld. AR, based on her aforesaid contention, submitted that the order passed by the AO/TPO substituting the ALP of the interest paid by the assessee company on ECBs from LIBOR + 3% to LIBOR + 2% on an ad hoc basis and without any justification be set aside.

14. Coming to the TP adjustment of interest on outstanding trade receivables relating to the provision of contract R&D services and contract manufacturing services by the assessee company to its AEs, the Ld. AR submitted that the TPO had grossly erred in imputing the interest without following the statutorily prescribed method and dispensing the mandatory comparability benchmarking as prescribed in Chapter-X of the Act. Apart from that, the Ld. AR submitted that, as the assessee company does not pay any interest on its outstanding payables to AEs, no notional interest rate is imputed on the receivables outstanding from the AEs. Alternatively, the Ld. AR submitted that though the outstanding receivables are not a separate international transaction, but if the same is to be so treated, then it should be benchmarked using a combined transaction approach, i.e., by combining the outstanding receivables with the main international transaction of provision of services, due to the fact that the receivables are a result of the international transactions of the assessee company. Alternatively, the Ld. AR submitted that the Tribunal in the assessee’s own case for the preceding years, i.e., AY 2010-11 to AY 2014-15, had directed the AO/TPO to adopt LIBOR + 200 basis points as the applicable ALP interest rate for the purpose of imputation of interest on outstanding receivables from AEs. The Ld. AR to buttress her aforesaid contention had taken us through the orders passed by the Tribunal in the assessee’s own case for AY 2010-11 to AY 2014-15 in Albany Molecular Research Hyderabad Research Center (P.) Ltd. v. Dy. CIT (Hyderabad – Trib.)/ITA No.425/Hyd/2015, 233 & 107/Hyd/2016, 2184/Hyd/2017 and 2376/Hyd/2018, dated 26/11/2020, Page 874 of APB.

15. Coming to the last issue, the Ld. AR submitted that the AO had erred in not adjusting the brought-forward business losses of previous years of Rs. 116,62,76,178/- against the business income of the assessee company, computed after making the TP adjustment of Rs. 8,10,59,589/-. Elaborating on her contention, the Ld.AR submitted that pursuant to the amalgamation of AMRI India and Finekem India (hereinafter referred to as amalgamating companies) with the assessee company, the latter had taken over the brought forward losses of the amalgamating companies and had duly filed “Form 62” stating that it had satisfied the conditions under section 72A of the Act to utilize the brought forward losses of the amalgamating company. The Ld. AR submitted that, as the assessee company is eligible to claim brought-forward losses of previous years of Rs. 116,62,76,178/, as disclosed in its return of income for AY 2018-19, an application for rectification of the subject mistake has been filed with the AO and is pending disposal.

16. Elaborating further on her contention, the Ld. AR submitted that the DRP on the aforesaid issue had directed the AO to verify the record and allow the claim of the assessee company for brought forward losses in accordance with law.

17. Per contra, Dr. Narendra Kumar Naik, Learned CIT-DR, relied upon the orders of the authorities below.

18. We have given thoughtful consideration to the contentions advanced by the Learned Authorized Representatives of both parties qua the multifaceted issues involved in the present appeal.

19. Apropos the Ld. AR’s contention that the TPO had erred in not considering the segmental financial information (with AE and transaction-wise segmentation) that was provided by the assessee company in TP documentation, which is certified by the Cost and Management Accountant, and had summarily rejected the same on an ad hoc basis, which is not permissible as per the mandate of law, we find substance in the same. As is discernible from the record, the assessee company which had adopted direct allocation of cost, i.e., by identifying the relevant cost for the respective segments and the balance on the most relevant allocation keys, viz., FTE hours for R& D segment, machine hours for API segment, turnover basis for few expenses in its TP documentation, which is duly certified by Cost and Management Accountant, had adopted a refined approach for preparation of segment results giving true and fair view of its international transactions. We find that the TPO rejected the segmental results provided by the assessee company in its TP documentation because, in his view, the audited financials did not match the segment results. We are unable to persuade ourselves to subscribe to the aforesaid observation of the TPO. As pointed out by the Ld. AR, and rightly so, the assessee company vide its letter, dated 23/07/2021 filed with TPO had given a detailed reason for the aforesaid impugned discrepancy, and had brought to his notice that the segment results for the TP purpose were detailed and accurate as per business segment wise, wherein AE and non-AE expenses were bifurcated whereas for audited financials, the mandate of AS-17 has alone been followed, which referred to related party and non-related party details only without getting into each business segment wise. In fact, on a conjoint perusal of the segmental information provided by the assessee company in its audited financials, Page 34 of APB, and in its TP documentation as certified by the Cost and Management Accountant, Page 483 of APB, the revenue from operations is duly reconciled. In our view, the TPO proceeded on the wrong premise and clearly overlooked the assessee company’s detailed reply. Apart from that, we find substance in the Ld. AR’s contention that the approach adopted by the TPO/DRP to allocate cost on revenue proportion will result in the same profitability for all the segments, leading to an incorrect conclusion of equating the non-AE segment and the AE segment. At this stage, we may herein observe, that the assessee company, vide its reply, dated 28/07/2021 filed with the TPO had submitted before him that for the purpose of TP billing and compliance, with a view to provide/evaluate the profitability in a more accurate manner, it had prepared segmental financials, wherein the economic analysis for international transactions of contract R&D services and contract manufacturing with AEs was prepared considering the operating margin earned by respective segment of the assessee company which was compiled on certain basis, viz., (i) segment revenue was directly identifiable to the respective segments; (ii) that as the assessee company was operating as three different entities viz., (a) Curia India (only providing contract R&D services); (b) AMRI India (only manufacturing of API); and (c) Finekem (only manufacturing of API), the cost pertaining to each activity of contract R&D services and manufacturing API has been maintained separately and was directly identifiable to the respective segments; and (iii) that within such segments, costs of the respective segments for both AE and non-AE segments were identifiable on basis of actuals and the balance had been allocated on the basis of the relevant allocation keys (such as FTE hours, machine hours etc.). Accordingly, the assessee company, based on its aforesaid segmental financials, had determined its operating margin (OP/OC) for each segment, i.e., (i) contract R&D services: 15.44%; and (ii) manufacturing of API: 17.26%.

20. We have given thoughtful consideration and are unable to concur with the rejection of the segmental results of the assessee company on an ad hoc basis by the TPO/DRP. Our aforesaid view that where expenses are allocated to eligible and non-eligible units on the basis of jointly accepted accountancy principles, on the basis of identified cost drivers and in a prudent manner by an assessee company, the AO/TPO/DRP are not justified in reallocating the expenditure in the ratio of turnover between eligible and non-eligible units without any investigation and without collecting any material as well as without pointing out any discrepancy on the part of the assessee company in relation to the method of allocation of cost as adopted is supported by the judgment of the Hon’ble High Court of Delhi in the case of Principal Commissioner of Income Tax v. NALWA Steel & Power Limited, (supra). Also, a similar view had been taken by the ITAT, Hyderabad “B” Bench in the case of TPSC (India) (P.) Ltd. (supra). It was observed that the assessee company had computed segmented operating margin on cost from rendering of design, engineering, and other related services to its AEs, but TPO used total revenue and total expenditure to determine ALP. The Tribunal remanded the matter for consideration of the details furnished by the assessee company regarding the computation of the margin for the provision of services to AEs. Further, we find that the ITAT, Mumbai “J” Bench in the case of Mylan Pharmaceuticals Private Limited(supra) has held that as there was no basis for the TPO/DRP to reject the duly certified segmental results, which were submitted by the assessee company, and, thus, such rejection of the segmental results by the authorities below was liable to be set aside.

21. We thus, in terms of our aforesaid deliberations on the facts involved in the case before us, read with the settled position of law, are of firm conviction that as both the TPO/DRP had failed to independently analyze the duly certified segmental financial results submitted by the assessee company and mechanically rejected the same, therefore, the matter requires to be restored to the file of the TPO for considering the said certified segmental financial results provided by the assessee company in its TP documentation.

22. We shall now deal with the Transfer Pricing adjustment of interest on External Commercial Borrowings (ECBs) suggested by the TPO, wherein the benchmarking of the interest on the ECBs borrowed by the assessee company @ LIBOR + 3% was rejected and substituted by the TPO for LIBOR + 2%, which thereafter had been upheld by the DRP.

23. As is discernible from the record, though the assessee company had undertaken a detailed benchmarking analysis in its Transfer Pricing Study Report (TPSR) for benchmarking the Arm’s Length Price (ALP) of the interest on ECBs borrowed (denominated in USD), the TPO, brushing aside the same, had summarily taken ALP of the said transaction at LIBOR + 2%.

24. In our view, there is substance in the Ld. AR’s contention that as the assessee company had obtained prior approval of the RBI for borrowing the loan from its AE, and the interest rate of LIBOR + 3% is lower than the ceiling rate prescribed by the RBI, therefore, on the said basis itself, the transaction of payment of interest on ECBs can be held to be at Arm’s Length.

25. Before proceeding further, we deem it apposite to cull out the payment of interest by the assessee company on ECBs taken from its AE, as under:

| FY in which the ECB was taken |

Rate of interest |

Amount of interest charged to P Co L Account (INR) |

| 2013-14 |

GBP LIBOR plus 3% |

15,22,598 |

| 2014-15 |

GBP LIBOR plus 3% |

48,69,917 |

| 2015-16 |

GBP LIBOR plus 3% |

16,00,495 |

| 2016-17 |

GBP LIBOR plus 3% |

45,72,842 |

| 2017-18 |

GBP LIBOR plus 3% |

55,07,130 |

| Total |

1,80,72,981 |

26. We find that it has been the claim of the assessee company that the TPO had erred in not appreciating that the loan borrowed from the AE after obtaining prior approval from RBI was well within the ceiling contemplated in the RBI circulars. In fact, we find that the RBI Master Circular on ECB and trade credits for FY 2013-14, FY 2014-15, and FY 2015-15 reveals that the interest paid by the assessee company at LIBOR + 300 basis points on ECBs borrowed from its AEs is less than the interest ceiling provided by RBI. We find that the Hon’ble High Court of Karnataka in the case of

CIT v.

M/s. GE India Technology Center Pvt. Ltd. ,

(supra) observed that the RBI’s approval of the rate of interest is a relevant factor in determining the ALP of that rate. Also, it was observed that, as per the settled position of law, the rate of interest should be determined on the basis of the rate of interest prevailing at the time of availing the loan. Also we find that the ITAT, Mumbai in the case of

Firemenich Aromatics Production (India) (P.) Ltd. v.

ACIT [2021] (Mumbai –

Trib.)/ITA No.7844/Mum/2019, dated 26/10/2021 had observed that the assessee company which had obtained a loan in the nature of External Commercial Borrowing (ECB) from its AEs had benchmarked the same at the interest rate of six months USD LIBOR rate + 350 basis points by relying upon the RBI Circular No.12/2012-13, which allowed the ECB loan on automatic route at those rates. However, the TPO had computed the benchmark rate as LIBOR + 143.62 basis points, based on the Bloomberg database. The Tribunal, relying upon its earlier order in the assessee’s own case for AY 2014-14, held that the ALP of such transactions would be more accurately determined by following the rate of interest fixed by RBI in respect of ECB loan. Also, we find that the ITAT, Mumbai Bench, in

Goodyear South Asia Tyres Private Limited (supra) had upheld the view taken by the assessee company by relying on its earlier order for AY 2006-07 in ITA No.143/pN/2010, dated 28/04/2014, and held that the rate of interest paid on ECB at the rate of LIBOR + 3% was as per the rate of interest notified by the RBI at the time of raising the said ECB loan, thus, the same was at Arm’s Length. Further, we find that the ITAT, Mumbai, in the case of Asst. Commissioner of Income Tax, Central Circle-39,

Mumbai v.

M/s. Firestone International Pvt Ltd, (supra) has held that the interest charged by the assessee company at LIBOR + 300 BPS as being at Arm’s Length.

27. At this stage, we may herein observe that there is substance in the Ld. AR’s contention that the TPO had erred by summarily rejecting the benchmarking of the interest paid on ECBs carried out by the assessee company at LIBOR + 3%, without following any comparability benchmarking analysis prescribed under Chapter-X of the Act. We thus, in terms of our aforesaid deliberations, are unable to persuade ourselves to concur with the view taken by the TPO/DRP and uphold the benchmarking of the interest paid on ECBs by the assessee company at LIBOR + 3%.

28. Coming to the benchmarking of the interest on the outstanding trade receivables relating to the provision of contract R&D services and contract manufacturing services to AEs, we are unable to concur with the Ld. AR that the same is not an international transaction. However, we find that as had been brought to our notice by the Ld. AR, the issue is squarely covered by the order passed by the Tribunal in the assessee’s own case for AYs 2010-11 to 2014-15 in ITA No.425/Hyd/2015, 233 & 107/Hyd/2016, 2184/Hyd /2017 and 2376/Hyd/2018, dated 26/11/2020. In the said order, it was observed that, as the assessee company had received its outstanding receivables from its AE in foreign currency, it would be just and fair to adopt LIBOR + 200 basis points as the applicable ALP interest rate for the purpose of imputing interest on outstanding receivables from AEs. Also, it was observed that the said imputation of interest is to be made on an invoice-to-invoice basis on outstanding receivables so that the period of delay in respect of each invoice could be actually worked out. For the sake of clarity, we deem it apposite to cull out the observations of the Tribunal in the aforesaid case of the assessee company for the preceding years, as under:

“5.7. It would be relevant to note in the aforesaid paragraph that assessee had to receive its outstanding receivables from its AE in foreign currency, it would be just and fair to adopt LIBOR rate + 200 basis points as the applicable ALP interest rate for the purpose of imputation of interest on outstanding receivables from AEs. Needless to mention that the said imputation of interest is to be made on invoice to invoice basis on outstanding receivables so that the period of delay in respect of each invoice could be actually worked out.

5.8. The ground raised by the assessee for both the years praying for netting of outstanding payables to AEs with outstanding receivables from AEs cannot be entertained in view of our direction that imputation of interest is to be made on invoice to invoice basis on supplies made / services rendered by the assessee to its AEs. In view of this direction and in view of the fact that date of raising of export invoice on AE would be different from date of purchase of goods or import of services from AE. Accordingly, the ground raised on netting of outstanding payable with outstanding receivable is hereby dismissed for both the years.

5.9. To sum up for the A.Yrs 2013-14 & 2014-15, we hold that the outstanding receivables from AEs would constitute a separate international transaction on which imputation of interest is to be made by applying LIBOR + 200 basis points as under:-

| a. |

|

In respect of invoices raised in earlier years by the assessee on its AEs, where the amounts were realized during the year under consideration but beyond the agreed credit period, imputation of interest is to be made from first day of April or from the expiry of the agreed credit period (i.e 30 days as accepted by Id DRP) whichever is later till the date of realization of debts. |

| b. |

|

In respect of invoices raised during the year on its AEs, where the amounts were realized during the year itself but beyond the agreed credit period, imputation of interest is to be made from the date of expiry of agreed credit period till the date of realization of debts.” |

29. We thus, in terms of our aforesaid observations, direct the AO/TPO to recompute the ALP of the interest on outstanding receivables following the view taken by the Tribunal in the assessee’s own case for the aforementioned preceding years, i.e., AY 2010-11 to AY 2014-15.

30. Coming to the last issue, we find that it is the claim of the Ld. AR that the AO had erred in not adjusting the brought forward losses pertaining to previous years, amounting to Rs. 116,62,76,178/- against business income computed after making the transfer pricing adjustment of Rs. 8,10,59,589/- for the year under consideration.

31. As is discernible from the record, it is the claim of the assessee company that pursuant to the amalgamation of AMRI India and Finekem India (hereinafter referred to as amalgamating companies) with the assessee company, the latter has taken over the losses of the amalgamating companies. Also, it is stated that the assessee company had duly filed “Form-62” and satisfied the conditions in section 72A of the Act to utilize the brought forward losses of the amalgamating company, as under:

32. The Ld. AR, based on the aforesaid facts, had submitted that the assessee company is duly eligible to claim adjustment of the brought forward losses of the above-mentioned amalgamating companies amounting to Rs. 116.62 crores (approx.) as disclosed in its return of income for the year under consideration. Elaborating further on her contention, the Ld. AR submitted that the assessee company had filed an application for rectification, which is pending before the AO for disposal. It is further stated that the DRP had directed the AO to verify the record and allow the claim for brought forward losses, if any, in accordance with the provisions of the Act.

33. We find that as the adjudication of the aforesaid issue involves verification of the facts and the DRP had already directed the AO to verify the record and allow the claim for brought forward losses, therefore, finding no infirmity in the directions of the DRP, we uphold the same.

34. In the result, the appeal filed by the assessee company is partly allowed in terms of our aforesaid observations.