ORDER

Sudhir Kumar, Judicial Member.- This appeal is preferred against the order dated 30-012025 passed u/s 10(3) of the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (herein after referred “the Act”) by the Commissioner of Income Tax (Appeals) -3 Gurgaon in short “Ld. CIT(A)) pertaining to the assessment order dated 17-02-2022 for A.Y.2018-19.

2. The assessee has raised the following legal ground in appeal:

| 2. |

|

That the Ld. CIT(A) erred in law and on facts in upholding the assessment order dated 17-02-2022 passed under section 10(3) of the Black Money Act, without appreciating that the proceedings initiated by AO, under section 10 of the BMA vide notice dated 10-04-2018 were barred by limitation as having been initiated after inordinate delay, post receipt of alleged information from FT& TR reference. |

3 The brief facts of the case are that the assessee is a individual. The assessee is a proprietor of M/s Jade Knits having residence at A064 ICON Apartment DLF Phase V. Gurgaon Haryana. The assessee along with other namely Mr. Brijesh Kumar Agarwal and Mr. Harish Kumar were directors of the company M/s Woodstock Universal Ltd. (WUL) located Britsh Virgin Islands and was incorporated on 10-04-2007 and was struck off on 01-11-2014. The company M/s Woodstock Universal Ltd. 18-00 Suntech City Towers Singapore was authorized to issue 50,000 shares of a singles class out of which one share was issued to the assessee by the company on 03-08-2007 having value of USD 1.00. There were certain credits in the bank account of the assessee which was not disclosed in the return of income. Therefore, proceedings of the Act were initiated by issuing the notice u/s 10(1) of the Act. During the assessment proceedings the Assessing Officer collected the evidence by making the reference to the Singapore authority and completed the assessment after making the additions of Rs. 15,66,870/-under the Act. According to AO the WUL made the payment to the assessee which was not disclose in the return of income as follows:

| Sr. No. |

Date |

Amount |

Estimated amount in Rs. (estimated dollar rate 43.5 in 2008) |

| 1 |

28-05-2008 |

USD 11.020 |

4,79,370 |

| 2 |

31-07-2008 |

USD 25,000 |

10,87,500 |

|

TOTAL |

|

15,66,870 |

4. Aggrieved the order of the Assessing Officer the assessee preferred the appeal before the Ld. CIT(A) who vide his order dated 30-01-2025 dismissed the appeal. Being aggrieved the order of the Ld. CIT(A), the assessee is in appeal before the Tribunal.

5. The Ld. AR of the assessee submitted that the assessment is barred by limitation. In this regard chart of date enumerating the relevant facts pertaining to the issue has filed which is reproduce as under:

| Date |

Event |

| 10-04-2007 |

M/s wood stock Universal Limited was incorporated in British Virgin Island. The said company was struck off on 01-11-2024 before the promulgation of the Black Money Act. (pg 1 of the AO Para 1.1) |

| 02-09-2014 |

The FT & TR reference was made to authorities in BVI to documents pertaining to M/s Woodstock Universal Limited (Pg 3 of AO para 4.1) |

| CBDT notification No. 73/2015 dated 24-08-2015 |

The relevant ACIT/DCIT or JCIT having jurisdiction over assessee under the Income Tax Act were also empowered to exercise such jurisdiction under BMA |

| 23-09-2015 |

The FT & TR reference was made to authorities in Singapore to obtain documents pertaining to M/s Woodstock Limited. (pg.3 of AO, Para4.1) |

| Notification dated 16-05-2017 |

CBDT empowered DGIT (Inv.) / Pr. DIT(Inv.) to issue orders in writing for the exercise of the concurrent powers and performing the function of AO to ADIT/DDIT |

| 08-09-2017 |

PDIT(Inv.) Chandigarh vide his office order F.No. Pr. DIT/INV/CHD/2017-18 assigned concurrent jurisdiction to DDIT (Investigation)/ ADIT Investigation -1 Gurgaon (pg. 2 of AO para 2.21 |

| 29-11-2017 |

Statement of the assessee was recorded where the alleged information received from the aforementioned references were confronted to the assessee |

| 27-03-2018 |

Investigation carried out by DDIT(Inv)-II Gurugram and report thereof sent by DDI(Inv) -II to DDIT (Investigation)/ADIT Investigation-1 Assessing Officer (pg 2 of AO para 2.3) |

| 10-04-2018 |

Notice u/s 10(1) of BMA |

| 31-03-2021 |

Expiry of limitation for passing order u/ s 10(3) in terms of limitation prescribed u/s 11 of BMA |

| 17-02-2022 |

Order u/s 10(30 of BMA |

6. He further submitted that the assessment order is barred by limitation and the assessment can be framed by 31-032021 because the notice u/s 10(1) Of the BMA was issued on 10-04-2018. As per the section 11 of the Black Money Act the assessment shall be framed after the expiry of two years from the end of the financial year in which the notice under sub section (1) of the section 10 of the Act was issued by the Assessing Officer. In this case notice under section 10(1) of the BM Act was issued on 10-04-2018 then assessment can be framed by 31-03-2021 after the expiry of two years of the financial year. The assessment order was passed on 17-022022 which is time barred.

7. The section 11 of the BM Act reproduce as under:

11.Time limit for completion of assessment and reassessment.—

(1) No order of assessment or reassessment shall be made under section 10 after the expiry of two years from the end of the financial year in which the notice under sub-section (1) of section 10 was issued by the Assessing Officer.

(2) Notwithstanding anything contained in sub-section (1), an order of fresh assessment in pursuance of an order passed under section 18 setting aside or cancelling an assessment, may be made at any time before the expiry of the period of two years from the end of the financial year in which the order under section 18 is received by the Principal Commissioner or the Commissioner.

(3) The provisions of sub-section (1) shall not apply to the assessment or reassessment made in consequence of, or to give effect to, any finding or direction contained in an order under section 15 or section 18 or section 19 or section 22 of this Act or in an order of any court in a proceeding otherwise than by way of appeal under this Act and such assessment or reassessment may, subject to the provisions of sub-section (2), be completed at any time, before the expiry of the period of two years from the end of the financial year in which such order is received by the Principal Commissioner or the Commissioner.

Explanation 1.—In computing the period of limitation for the purpose of this section—(i) the time taken in reopening the whole or any part of the proceeding; or

(ii) the period during which the assessment proceeding is stayed by an order or injunction of any court; or

(iii) the period commencing from the date on which a reference or first of the references for exchange of information is made by an authority competent under an agreement referred to in section 90 or section 90A of the Income-tax Act or under section 73 of this Act and ending with the date on which the Principal Commissioner or the Commissioner last receives, the information so requested or a period of one year, whichever is less, shall be excluded:

Provided that where immediately after the exclusion of the aforesaid time or period, the period of limitation referred to in sub-sections (1), (2) and (3) available to the Assessing Officer for making an order of assessment or reassessment, as the case may be, is less than sixty days, such remaining period shall be extended to sixty days and the aforesaid period of limitation shall be deemed to be extended accordingly.

Explanation 2.—Where, by an order referred to in sub-section (3), any undisclosed foreign income and asset is excluded from the total undisclosed foreign income and asset for an assessment year in respect of an assessee, then, an assessment of such undisclosed foreign income and asset for another assessment year shall, for the purposes of section 10 and this section, be deemed to be one made in consequence of, or to give effect to, any finding or direction contained in the said order.

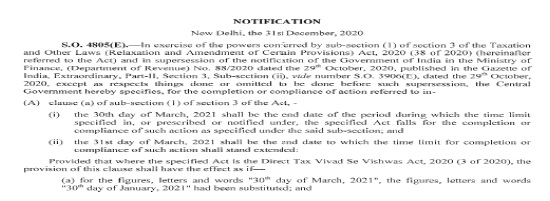

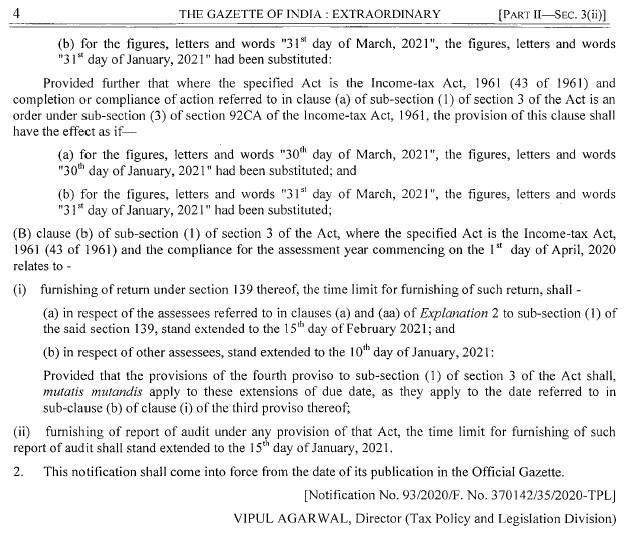

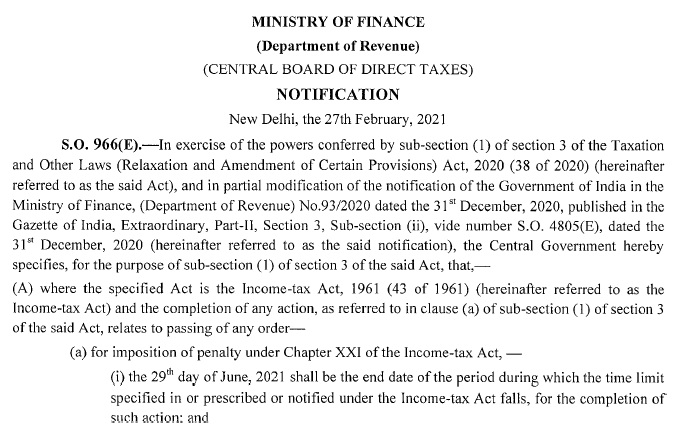

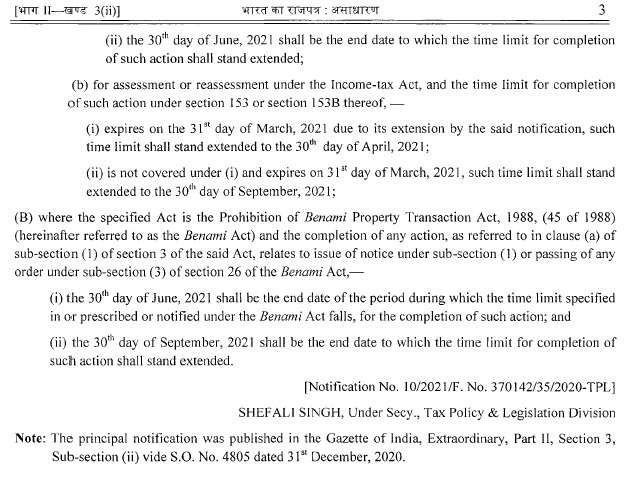

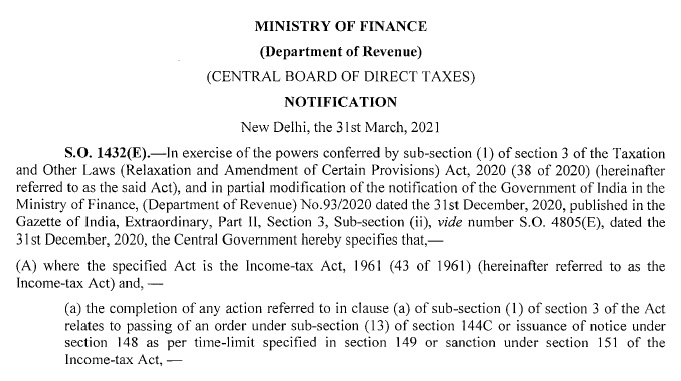

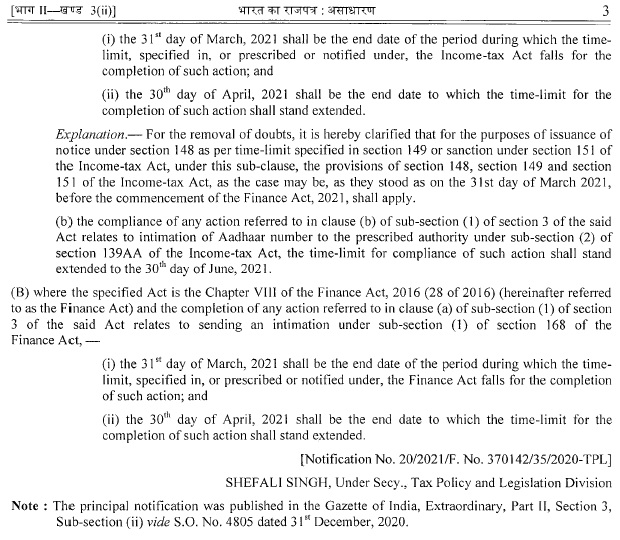

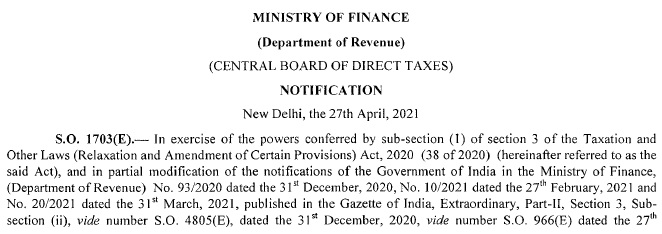

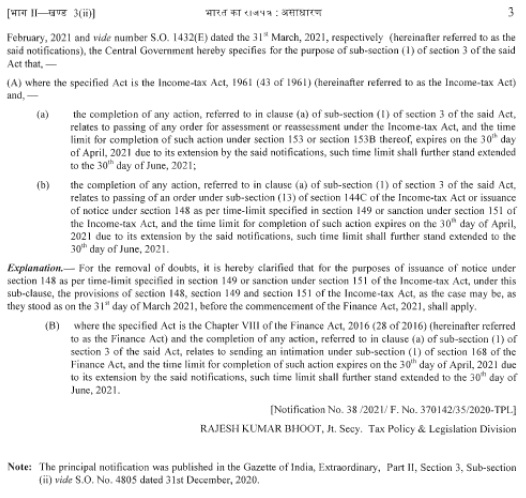

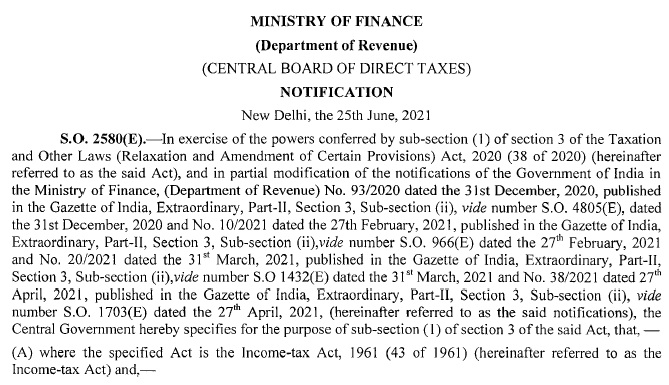

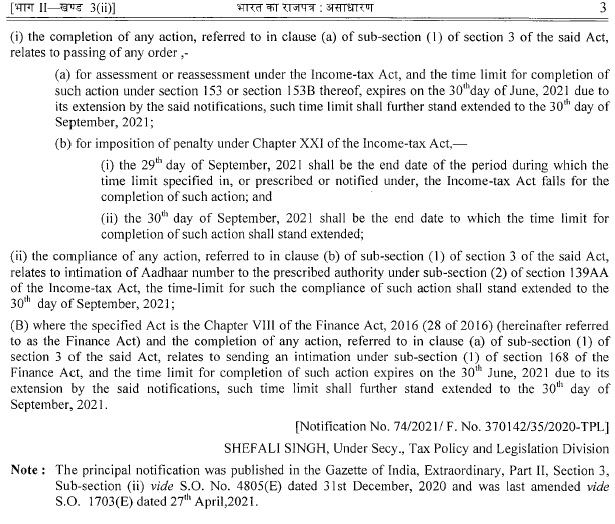

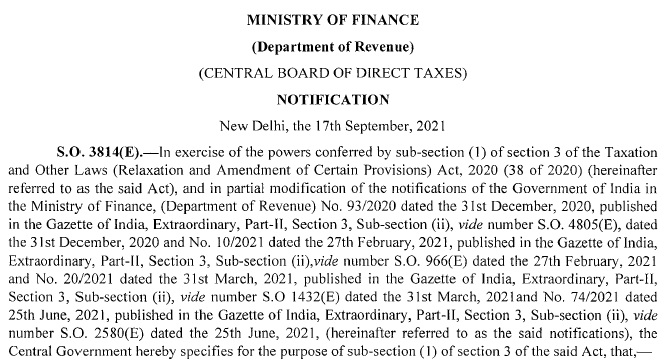

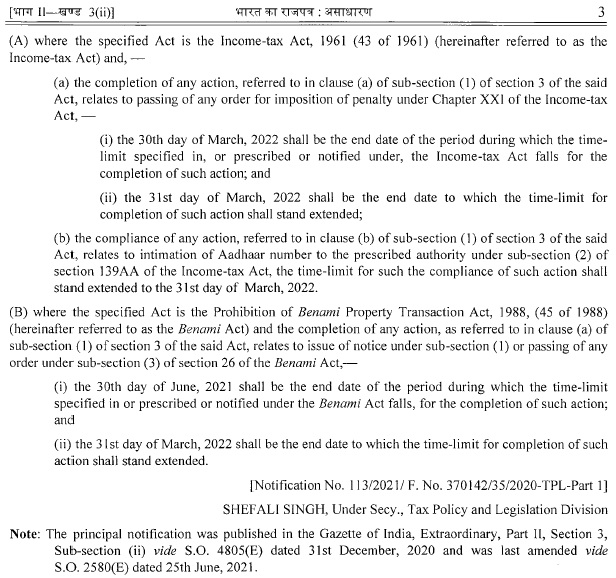

8. The Ld. Authorized Departmental Representative submitted as per section 11 of the BM Act no order of assessment shall be made after the expiry of two years from the end of the financial year in which the notice under section 10(1) of the Act was issued. In this case notice was issued in the financial year 2018-19 and the ends of the F.Y. was 31-03-2019 the assessment should be passed by 31-03 2021 in the normal circumstances. He also stated that the Parliament enacted the Act “The Taxation and Other Laws (Relaxation and Amendment of Certain Provisions) Act 2020 (in short “TOLA”) with effect from 31-03-2020 to extend the time limit for the assessment. He further submitted that by issuing the notifications on various dates the time limit of framing the assessment was extended. The last notification was issued on 17-09-2021 by which the time limit was extended by 31-03-2022. He further submitted that the assessment order was passed in the extended time which is within time. The Notifications issued by the Ministry of Finance are reproduced as under:

9. We have heard the parties and gone through the material available on record. The Ld. AR of the assessee submitted that in the Act TOLA the specified Act defined in section 2(b) and specified Act means (i) the Wealth -tax Act, 1957 (ii) the Income- tax Act, 1961 (iii) the Prohibition of Benami Property Transactions Act, 1988 (iv) Chapter VII of the Finance Act 2004 (v) Chapter VII of the Finance Act 2013 (vi) the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act 2015 (vii) Chapter VIII of the Finance Act, 2016 or (viii) the Direct Tax Vivad se Vishwas Act, 2020. He further submitted that the time period was extended for the above specified Act by the TOLA. After that, by the Notification No. 93/2020 dated 31-12-202 the limit for completion was extended by 31-03-2021, for all the specified Act defined in the TOLA. By the Notification No. 10/2021 dated 27-02-2021 the limit for completion was extended by 31-03-2021 for the specified Act the Income -tax Act. Further by notification No. 20 /2021 dated 31-03-2021, notification No. 38/2021 dated 27-04 2021and Notification no. 74/2021 dated 25-06-2021 extended the date for complication of the action for the specified Act the Income -tax Act. Lastly by notification no. 113/ 2021 dated 17-09-2021 the time limit was extended for the specified Act’ the Income tax Act by 3103-2022 not for the all the specified Act as defined in TOLA. He also submitted that the assessment was not framed within the time limit therefore the assessment is time barred.

10. We find that the TOLA was enacted by the Parliament with effect from 31-03-2020 to extend the time limit of the specified Act which was defined in the section 2(b) of the Act for completing the actions. This time limit was extended by issuing the various notification. The Ministry of Finance by issuing the Notification No.113/2021 dated 17-09-2021 extended the time limit for completion of any action for the specified Act i.e Income-tax Act and the Prohibition of Benami Property Transaction Act, 1988, not for all the specified Act as defined under section 2(b) of the TOLA. The time limit for completion the assessment under Black Money Act was not extended by this notification. The assessment should not be made after the expiry of two years from the end of the financial year in which the notice under section 10(1) of the Act was issued. The explanation provides relaxation in respect of the period commencing from the date on which a reference for exchange of information is made by an authority competent and ending with the date on which the Principal Commissioner or the Commissioner last receives, the information so requested or a period of one year, whichever is less shall be excluded. In the instant case the notice under section 10(1) of the Act was issued on 10-04-2018 and both the FT & FR references were made and received well before the intimation of proceedings under section 10(1) of the Act, and assessment should be made by 31-03-2021 but order was passed on 17-02-2022, which is time barred. Accordingly, the assessment proceedings liable to be quashed and quashed accordingly.

11. Since we have decided the legal ground in favour of the assessee the other grounds have become academic and keep them open for adjudication.

12. In the result, appeal of the assessee is allowed.