ORDER

Paresh M Joshi, Judicial Member.- These are two miscellaneous applications one bearing no. 29/IND/2025 which arises out of an order dated 08/02/2011 passed by ITAT Indore Bench in Appeal No. 188/IND/2010 for the Assessment Year 2007-08 (FY- 2006-07) and another bearing no. 30/IND/2025 which arises out of an order dated 08/02/2011 also passed by ITAT Indore Bench in Appeal No. 189/IND/2010 for the Assessment Year -2008-09 (FY- 2007-08). Hence both these appeals were disposed of by the ITAT Indore Bench as and by way of a consolidated order dated 08/02/2011.

2. These two miscellaneous applications bearing no. 29/IND/2025 and another bearing no. 30/IND/2025 supra in the aforesaid two appeals i.e., 188/IND/2010 and 189/IND/2010 were filed in the registry of ITAT Indore Bench on 05/12/2025.

3. These two miscellaneous applications (supra) have been filed under Rule 24 of Income Tax Appellate Tribunal Rules 1963 r/w section 254(2) of the Income Tax Act, 1961 respectively seeking recalling of order dated 08/02/2011(as prayed). It is also stated in paragraph no. 1 of these miscellaneous applications that both the aforesaid appeals were dismissed and decided ex-parte without merits owing to the non-appearance of assessee’s taxation manager who was pursuing and representing the assessee before the ITAT Indore Bench.

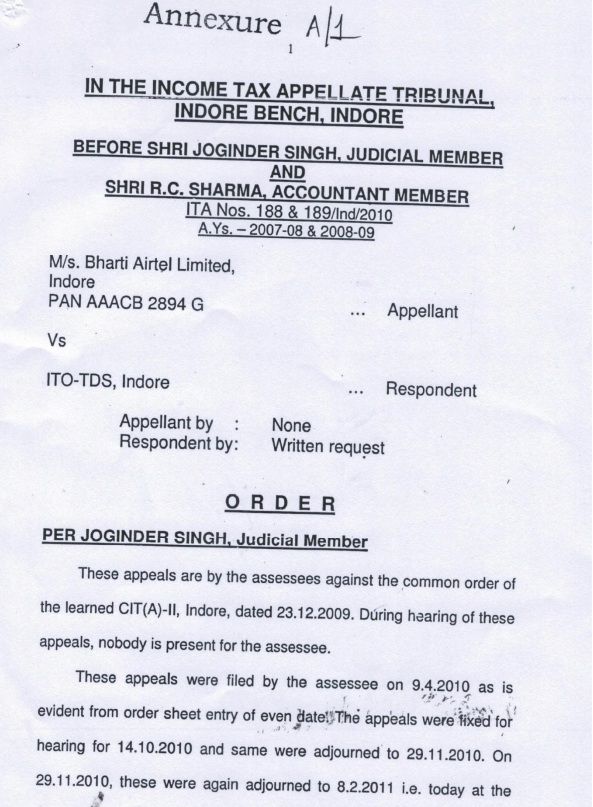

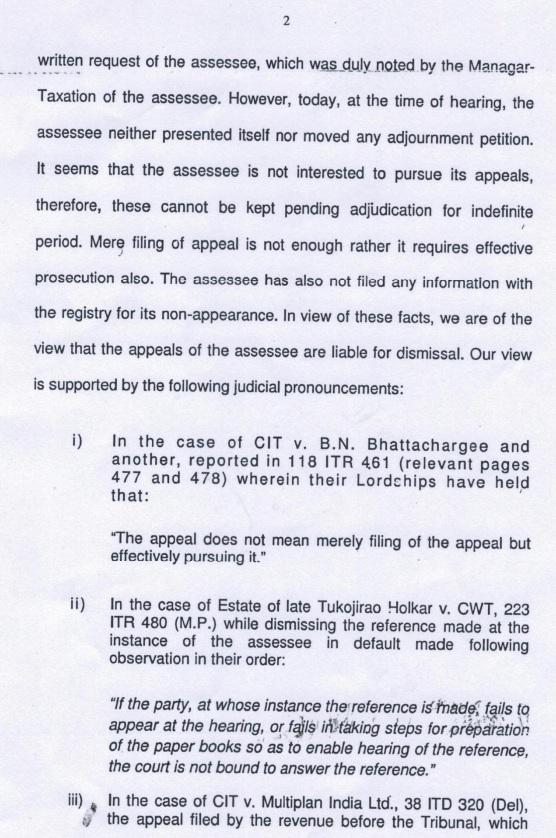

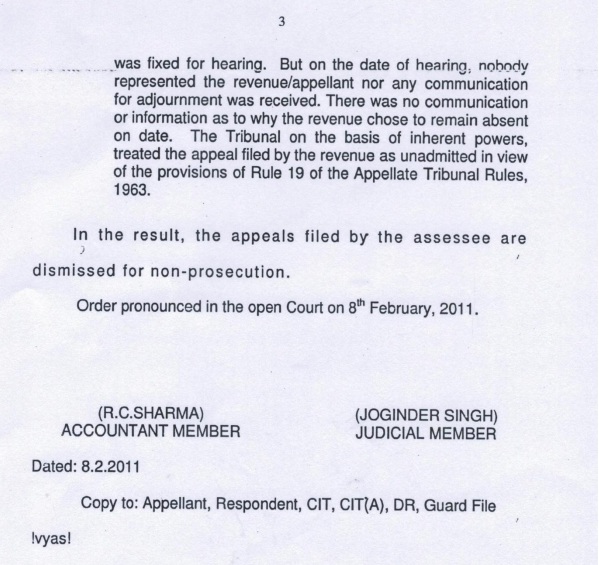

4. That the aforesaid order dated 08/02/2011 passed in the above mentioned appeals is reproduced by us below:-

5. In these two miscellaneous applications it has been averred that :-

“PRAYER

It is humbly prayed that the order dated 08.02.2011 passed by this Hon’ble Bench in ITA No. 188/IND/2010 (A.Y 2007-08) & ITANo.189/Ind/2010 (A.Y.2008-09) may kindly be recalled and restored to its original number in the larger interest of justice.

LIMITATION

That Rule 24 of the Income Tax (Appellate Tribunal) Rules, 1963 does not prescribe any limitation period for filing an application for rectification. The Appellant Company came to know about the impugned order dated 08.02.2011 only in October 2021. On the advice of the senior Advocate, the Company awaited filing of revival/restoration applications, as immediate relief was not feasible while the issue was pending before the Hon’ble Supreme Court. Therefore, the present application is being filed in November 2025, after the final adjudication by the Hon’ble Supreme Court in Civil Appeal No. 7257/2011 (Bharti Airtel Limited v. Assistant Commissioner of Income-tax, Circle- 57, Kolkata).”

6. Further, it has also been averred that :-

“18. That the Present Application for Revival/Restoration application is preferred on the following grounds/Reasons :-

18.1. That the impugned order is illegal, void and unsustainable in the eyes of law, as this Hon’ble Tribunal is duty-bound under Section 254(1) of the Act to decide the appeal on merits even in the absence of the appellant. The ex parte dismissal, without examining the merits, is contrary to the binding precedents laid down in Radheshyam Patel v. Union of India (MP), Balaji Steel Re-Rolling Mills v. CCE & Customs (Civil Appeal No. 10265/2014,

SC), CIT v.

S. Chenniappa Mudaliar [1969] 74 ITR 41 (SC)

and Dolphin Metal (India) Ltd. v.

ITO (Guj.) Cool Mind Technologies (P.) Ltd. v.

Assistant Commissioner of Income-tax (Kerala) [04.06.2024].

18.2 That the impugned order dated 08.02.2011 was never communicated to or served upon the Appellant Company, and at every stage of the penalty proceedings before the AO, CIT(A) and even before this Hon’ble Tribunal the Appellant consistently stated that the quantum appeal was still pending. It was only in October 2021, for the first time, that the Appellant discovered that the quantum appeal had already been dismissed. Thus the order was in breach of principles of natural justice on the ground of its non-service as well.

18.3 That the foundational issue involved now stands conclusively settled by the Hon’ble Supreme Court on merits & thus principles of equity & judicial disciple requires aligning the order of this Hon’ble Tribunal with that of the Hon’ble Supreme Court.”

7. Further, it has also been averred that :-

“3. That though the appeal was dismissed on 08.02.2011, the Appellant Company was neither served with nor made aware of the impugned order. Consequently, the Company remained unaware of the ex-parte dismissal of its appeal.”

8. Furthermore, it has been that:-

“12. Thereafter Appellant preferred further appeals before this Hon’ble Tribunal (ITA Nos. 407/IND/2018 to 410/IND/2018) qua penalty, and initially, even before this Hon’ble Tribunal, the Appellant continued under the bona fide belief that the quantum appeals were pending. It was only during the hearing of the penalty appeals in October 2021 that the Appellant, for the first time, came to know that the quantum appeals had already been dismissed, and this fact was immediately brought to the notice of this Hon’ble Tribunal by filing a status report regarding the quantum proceedings. Copy of Status report filed before this Hon’ble Tribunal on 08.10.2021 during the Course of hearing of penalty appeal for A.Y 2007-08 is marked as Annexure (A/4).”

9. In the above factual backdrop this tribunal is required to decide the present two applications in accordance with statutory provisions of law as contained in Income Tax Act, 1961 and Income Tax Appellate Tribunal Rules, 1963.

10. In this regard, firstly we reproduce section 254(2) of Income Tax Act, 1961 and the Rule 24 of the Income Tax Appellate Tribunal Rules, 1963 as the same is the basis of the above two miscellaneous applications:-

Orders of Appellate Tribunal

254(2):- ” The Appellate Tribunal may, at any time within (six months from the end of the month in which the order was passed) *with a view to rectifying any mistake apparent from the record, amend any order passed by it under sub-section (1) and shall make such amendment if the mistake is brought to its notice by the assessee or the (Assessing) Officer….”

*substituted “for four years from the date of order” by the Finance Act 2016 w.e.f. 01.06.2016″

Rule 24: “Hearing of appeal ex parte for default by the appellant [Substituted by the Income-tax (Appellate Tribunal) Amendment Rules, 1987 (w.e.f. 1st August, 1987)]-

“Where, on the day fixed for hearing or on any other date to which the hearing may be adjourned, the appellant does not appear in person or through an authorised representative when the appeal is called on for hearing, the Tribunal may dispose of the appeal on merits after hearing the respondent :

Provided that where an appeal has been disposed of as provided above and the appellant appears afterwards and satisfies the Tribunal that there was sufficient cause for his non-appearance, when the appeal was called on for hearing, the Tribunal shall make an order setting aside the ex parte order and restoring the appeal.”

10.1 Basis above statutory provisions i.e., 254(2) we observe that at the material time i.e., 08/02/2011 the date of the above ITAT Order (supra) the statutory time limit was “four years from the date of the order” was passed with a view to rectifying any mistake apparent from the record…..” (Note: this time limit was amended with effect from 01/06/2016 as within six months from the end of the month in which the order was passed). Keeping the aforesaid statutory provision in view, the invocation of section 254(2) on 05/12/2025 in the present miscellaneous application(s) is after a lapse of approximately 14 years is not at all justified in the law. There is no provision in the statute i.e., section 254(2) giving this tribunal power to relax &/or condone the aforesaid time limit. Therefore, on this limited ground these miscellaneous applications are not maintainable and are dismissed on the above ground alone.

11. In so far as, Rule 24 of ITAT, Rules, 1963 is concerned in proviso thereto there is a use of the word “afterwards”. The word “afterwards” in the Rule 24, in our considered view cannot be stretched and or expanded to such an extent so as to allow the relaxation &/or condonation for approximately 14 years in approaching this Tribunal for recalling of order dated 08/02/2011(as prayed) and/or for setting aside the order and restoring the appeal. Further we observe that there are no averments and contentions made with regard to the nonappearance of the assessee on 08.02.2011 as and byway of an explanation with sufficient cause when the appeals were called for hearing on 08.02.2011 and the ITAT passed the order. “In the absence of anything” in the miscellaneous application with regard to non-appearance on 08.02.2011 when the appeals were called for hearing these two miscellaneous application per se are not maintainable under proviso to the to rule 24 of ITAT, Rules 1963. Therefore, we are of the considered view that these two miscellaneous applications even under Rule 24 and its proviso are just not maintainable and are dismissed. The proviso to rule 24 contemplates an explanation as it mentions “satisfies the Tribunal that there was sufficient cause for his non appearance when the appeal was called on for hearing”. There is thus no explanation on this aspect.

12. We further hold that, the aforesaid order of ITAT Indore Bench dated 08/02/2011 was dispatched to the assessee by the registered post (Rule 35 of ITAT, Rules 1963-communication mode) by the ITAT, registry and the necessary report in this regard was called for by this tribunal from the registry and the copy thereof with annexures/extracts were given to the assessee. The assessee during the course of the proceedings before this tribunal by an affidavit dated 20/02/2026 and so also in the miscellaneous applications have denied the receipt of order dated 08/02/2011 of ITAT Indore Bench which was admittedly dispatched by Registered Post by ITAT Registry. The ITAT Registry has in-fact during the course of the proceedings by a report with enclosures therein have proved this fact. Per contra we observe and notice that assessee has pleaded bare denial of receipt of order dated 08/02/2011 and no evidence of delivery to assessee is on record. In this regard, we gainfully refer to of General Clauses Act, 1887 (section 27) which deals with service by post which provides that if services are made through registered post it is deemed to have been made in accordance with law. While on one pretext the assessee does not dispute dispatch of order dated 08/02/2011 of the ITAT Indore Bench by the ITAT, registry on 21/02/2011 by registered post and on the other pretext the assessee is denying its receipt as bare denial only.

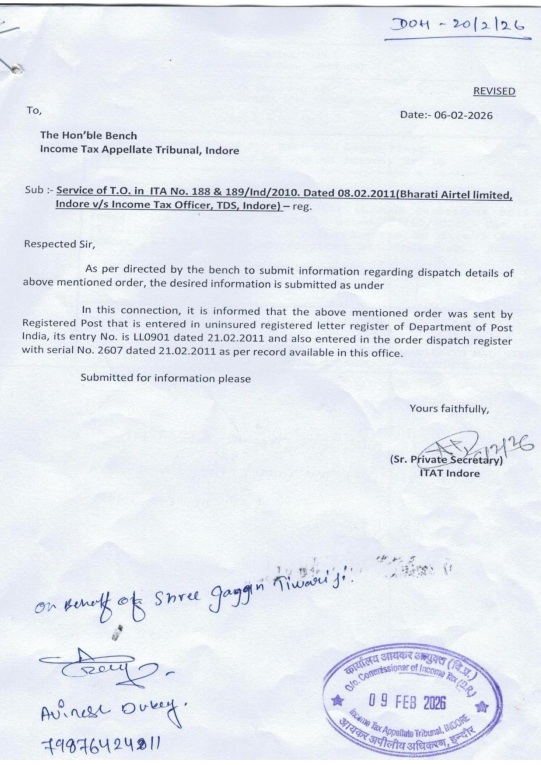

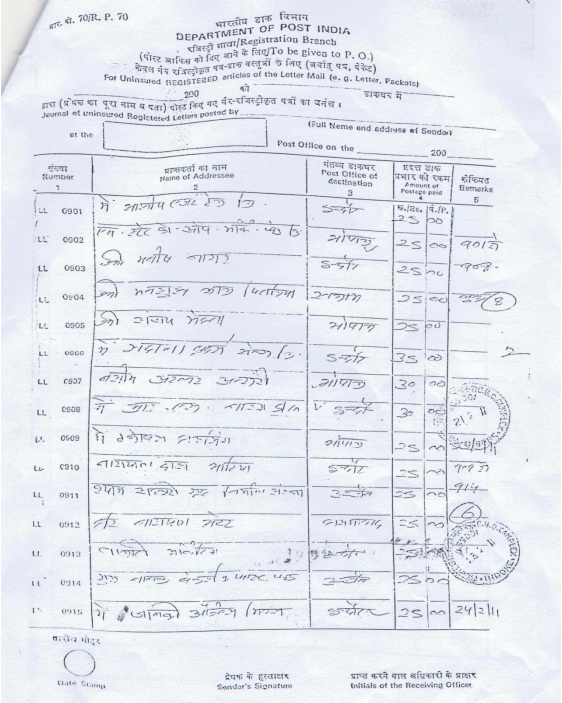

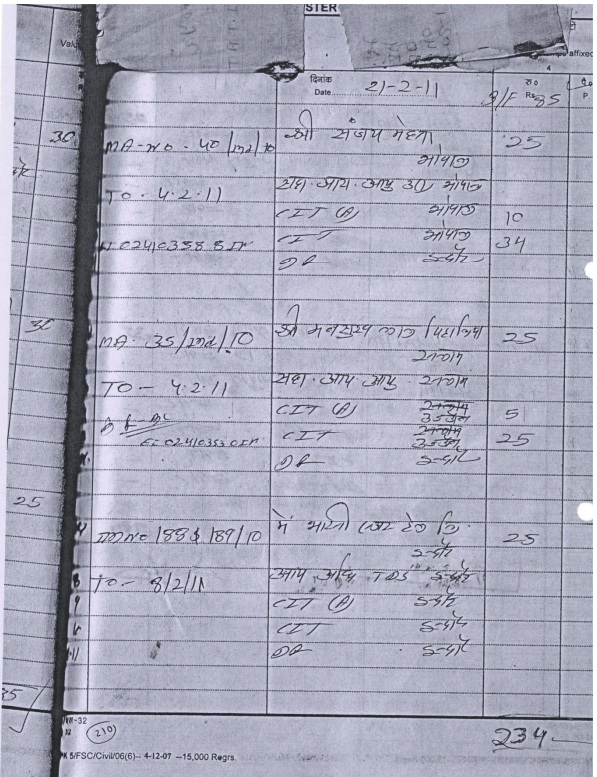

13. The report of the Registry of ITAT, Indore Bench is reproduced below along with relevant enclosures/extracts:

14. The contents of the above report and its enclosures/extracts are not disputed by the assessee in any manner whatsoever save and except that the order dated 08/02/2011 was not received by the assessee and that there is no proof of delivery of order (affidavit dated 20.02.2026). The assessee has failed to rebut by any evidence the material ingredients as mentioned in the General Clauses Act, 1887 (section 27) despite furnishing the report of the Registry of the ITAT with enclosures/extracts therein.

15. We also gainfully refer to the below judgments of the Hon’ble Bombay High Court, Apex Court and ITAT Orders:

15.1 The Hon’ble Bombay High Court in the case of

Bharat Petroleum Corpn. Ltd. v.

ITAT [2014] /[2013] 359 ITR 371 (Bombay) following its earlier decision in the case of

Khushalchand B. Daga v.

T.K Surendran, 4th ITO [1972] 85 ITR 48 (Bom.) held that where there had been a dismissal on default for non prosecution, it is a mistake which can only be rectified by an application under section 254(2) of the Act. Application under section 254 of the Act should have been filed within four years (as the law then stood) from the date of the order. However in this case as the application was made after the statutory time limit of four years from the date of the order of the Tribunal, the Hon’ble High Court was constrained to dismiss the appeal even though applying the principles laid down by the Hon’ble Supreme Court in the case of

CIT v.

S. Chenniappa Mudaliar [1969] 74 ITR 41 (SC) it observed that ” the Tribunal has no power to dismiss an appeal on ground of non-prosecution.” section 254(2) expressly have been strictly construed.

16. With regard to period of limitation in seeking cancellation of the earlier order passed by the Tribunal in violation of Rule 24 of ITAT Rules this is what the Hon’ble High Court observed at para.18 of its order—

” Para 18. Before concluding, we would like to make it clear that an order passed in breach of Rule 24 of the Tribunal Rules, is an irregular order and not a void order. However, even if it is assumed that the order in breach of Rule 24 of the Tribunal Rules is an void order, yet the same would continue to be binding till it is set aside by a competent Tribunal. In fact, the Apex Court in the Sultan Sadik v. Sanjay Raj Subba [2004] 2 SCC 277 has observed as under: —

‘Patent and latent invalidity

In a well-known passage Lord Radcliffe said:

“An order, even if not made in good faith, is still an act capable of legal consequences. It bears no brand of invalidity upon its forehead. Unless the necessary proceedings are taken at law to establish the cause of invalidity and to get it quashed or otherwise upset, it will remain as effective for its ostensible purpose as the most impeccable of orders.”

This must be equally true even where the brand of invalidity is plainly visible, for there also the order can effectively be resisted in law only by obtaining a decision of Court.

Further the Hon’ble Supreme Court in Sneh Gupta v. Dev Sarup [2009] 6 SCC 194 has observed—

“We are concerned herein with the question of limitation. The compromise decree, as indicated herein before, even if void was required to be set aside. A consent decree as is well known, is as good as a contested decree. Such a decree must be set aside if it has been passed in violation of law. For the said purpose, the provisions contained in Limitation Act 1963 would be applicable. It is not the law that where the decree is void, no period of limitation shall be attracted at all.”

Therefore, in this case also the period of four years from the date of order sought to be rectified/recalled will apply as provided in Section 254(2) of the Act. This is so even if it is assumed that the order dated 6 December 2006 is a void order.”

In view of above section 254(2) triumphs. It is correct section in law.

17. We gainfully also refer to the order of ITAT Hyderabad in the case of

Paresh Dhanji Chedda v.

Dy. CIT (Asst.) 160 ITD 656 (Hyd. –

Trib.), following precedents on this issue, held that the miscellaneous application filed by the assessee was not maintainable when the same was filed after the limitation period of four years (as the law stood then and) as prescribed under section 254(2) of the Act against dismissal of the order passed earlier by the Bench for want of prosecution. The Tribunal observed that dismissal of appeal for want of prosecution though may be illegal or contrary to law, should be considered as an order under section 254(1) of the Act and, therefore, time-limit prescribed under section 254(2) of the Act would apply.

18. We also say gainfully that following the decision of the Bombay High Court in the case of

Bharat Petroleum Corpn. Ltd. (

supra) the Bangalore Bench of ITAT in the case of

Ms. Shamsunissa Begum v.

Dy. CIT 165 ITD 557 (Bang-

Trib) held that where petition for recalling Tribunal’s (ex-parte) order was filed beyond the statutory period of six months(as the law stands now) from the date of Tribunal’s order (end of the month) in absence of any provision to condone any delay under Act, the same would be barred by limitation under section 254(2) of the Act. Similar view was expressed by a subsequent Bench of ITAT Bangalore in the case of

Smt. Padma K. Bhat v.

Asstt. CIT [2017] 166 ITD 172 (Bang. –

Trib.).

19. We gainfully also refer to The Hon’ble Madras High Court in the case of

S.P. Balasubrahmanyam v.

Asstt. CIT (Mad.) after analysing the provisions of section 254 of the Act as also Rules 24 and 25 of the ITAT Rules and by following the decision of the Hon’ble Bombay High Court in the case of

Bharat Petroleum Corpn. Ltd. (

supra) held as under—

“Even assuming that the period of limitation of four years for filing an application for recalling an order filed under section 254(2), has to be computed from the date of service of the order, averments made in the petition, filed in the year 2015, are bereft of details, as to when the order was served in the address, where the office of the appellant is situated. Order of the Tribunal has been passed on 18-7-2011, whereas, the assessee has filed the petition on 24-7-2015, which is beyond four years from the date of passing of the order by the Tribunal on 18-72011. Though assessee submitted that in the normal course, service of order, on the party would take some time, and therefore the miscellaneous application filed on 24-7-2015 was just six days exceeding the four years period from the date of passing the order and therefore, the Tribunal ought to have considered the time taken for service of the impugned order and allowed the application for rectification, the said contention cannot be accepted for the reason that, there are no averments in the miscellaneous petition, as to when the order was served on the appellant”

20. We have perused the judgment of Hon’ble MP High Court dated 09.02.2023 in case of Radheshyam Patel v. UOI (Madhya Pradesh) were in under a different set of facts including by placing the reliance on Apex Court decision in case of S. Chenniappa Mudaliar (supra), the ITAT order in Radheshyam Patel v. ITO [ MA No 13(Ind) of 2021, dated 26-9-2022] Radheshyam Patel Indore v. ITO [ITA No: – 206/Ind/2013, dated 13-07-2015] was set aside and the matter was remanded back to ITAT to decide the appeal on merits.

In the above case there was a delay of 5 years, 06 months and 23 days in preferring the miscellaneous application. The cause of delay was attributed to death of the lawyer after long illness, unavailability of documents, miscommunication from Dept. etc. which prevented the appellant therein to appear and same was pleaded as sufficient cause to restore the appeal and hear the same on merits [pleadings made by counsel recorded in Para 5 of the judgment of Hon’ble MP High Court dated 09.02.2023 in Radheshyam Patel (supra). It is also recorded in Para 4 of the Re Radheshyam Patel (supra) that earlier the appeal was adjourned “sine die” and no notice for next hearing was received by the appellant. WHEREAS in the instant case it is recorded in the ITAT order dated 08.02.2011 that “the appeals were fixed for hearing for 14.10.2010 and same were adjourned to 29.11.2010. On 29.11.2010 these were again adjourned to 08.02.2011 i.e. today at the written request of the assessee which was duly noted by the manager taxation of the assessee. However today, at the time of hearing the assessee neither presented itself nor moved any adjournment petition”. Hence even factually in the instant miscellaneous applications facts are different than Re Radheshyam Patel (supra). In Re Radheshyam Patel appellant had no notice for hearing as appeal earlier were adjourned sine die whereas in the instant case assessee had knowledge of hearing date as same was noted on 29.11.2010 for 08.02.2011 by manager taxation of the assessee.

In the instant case the ITAT order is dated 08.02.2011 whereas the miscellaneous applications were filed on 05.12.2025 with delay of approximately 14 years with no explanation with sufficient cause for non-appearance on 08.02.2011 when the appeals were called hearing. Hence with due respect we do not find any reason to apply in instant case the findings as laid down as the facts are distinguishable. Further we are of the considered view that this tribunal is creature of statute and we are bound by strict timeline as is stipulated in law. We have no statutory power to condone the huge delay of nearly 14 years under the Income Tax Act and ITAT rules 1963.

21. We have also perused the judgment of Hon’ble MP High Court dated 14.11.2014 in case of

Anil Kumar Agrahari v.

CIT [2010] 323 ITR 260 (Madhya Pradesh) were in the following question of law was framed u/s 260 A of the Income Tax Act 1961

” Whether the Tribunal has committed a grave error in rejecting the adjournment application filed by counsel of the appellant/assessee and thereby dismissing the appeal preferred by the appellant/assessee ex parte without adjudicating on the merits of the case and without affording another opportunity of hearing to the appellant/assessee when the paper book filed by counsel of the appellant/assessee already contained the written submissions and the relevant documents were on record before the Tribunal “

WHEREAS in the instant case the assessee has invoked the section 254(2) of the Act and proviso to the rule 24 of the Income Tax Appellate Tribunal Rules 1963. In Re Anil Kumar Agrahari an adjournment application filed by the assessee was rejected by the tribunal and so also the appeal ex-parte. Whereas the issue in these two miscellaneous applications is whether the assessee in respect of ITAT order dated 08.02.2011(supra) can present the miscellaneous applications on 05.12.2025 for setting aside the ex-parte order due to non-prosecution despite notice(s), after a lapse of nearly 14 years approximately when by virtue of section 254(2) the limitation period is six months post 01.06.2016 and four years prior to 01.06.2016 and that ITAT has no power to condone the delay at all further the expression “afterwards” appearing in proviso to Rule 24 of Income Tax Appellate Tribunal Rules 1963 can be expanded and/or stretched to such an extent so as to allow the relaxation/condonation for approximately 14 years in approaching this tribunal which we have answered (supra) as “NO”. We once again repeat and reiterate that this tribunal has no power to condone the delay of approximately 14 years under Section 254(2) of the Income Tax Act 1961. We also say that under proviso to Rule 24 of Income Tax Appellate Tribunal Rules 1963 the expression “afterwards” cannot be expanded and or stretched to such an extent so as to relax the delay of 14 years approximately as held by us aforesaid. Re Anil Kumar Agrahari respectfully is clearly on different set of fact whereas the issues in these two miscellaneous applications are materially different.

22. We also make it clear that both sides have cited catena of judgments during the hearing including clarificatory hearing but we have gone purely by the facts and circumstances of the case in hand and have given our findings basis the statutory provisions of law which being fiscal statute is required to interpreted strictly as per the plain language used in it. In this regard keeping ourselves restricted to the provision of section 254(2) and the Rule 24 of Income Tax Appellate Tribunal Rules 1963, we gainfully refer to the judgment of Hon’ble Bombay High Court cited by Ld. DR in case of Leena Power Tech Engineers (P.) Ltd. v. Dy. CIT (Bombay). Wherein in Para 15, 16, 17, 18 it has been held as under:-

“15. Insofar as the second contention is concerned, the issue of sufficient cause is not quite relevant. Section 254 of the IT Act does not contain any provision that enables the ITAT to condone a delay beyond 6 months. This is so held by the coordinate bench in Ram Baburao Salve (supra).

16. Given the above position, sufficient cause, if any, would be irrelevant. The ITAT has also not gone into the issue of sufficient cause but by relying on the decision of the Karnataka High Court Karuturi Global Ltd. v. Dy.CIT (Karnataka) held that it has no power to condone the delay in entertaining an application under Section 254(2) of the IT Act.

17. Since the ITAT’s view aligns with that of our coordinate bench in Ram Baburao Salve (supra) and the decision of the Karnataka High Court in Re. Karuturi Global Ltd. (supra), we see no good ground to interfere with the impugned order.

18. For all the reasons stated above, we dismiss this petition and discharge the Rule without imposing any cost orders.

23. We thus concur with the views of Hon’ble Bombay High Court (supra). The Ld. DR has placed reliance on the judgment of Karnataka High Court in case of Smt. Shobha Lakshman v. CIT(Appeal) (Karnataka) which has been urged by him to be parimateria with facts of present case and reliance was placed on Para 6 which is reproduced byus as below :-

“6. The appeal filed by the assessee before the ITAT against the order passed by the Commissioner of Income Tax (Appeals) dated 22.12.2017 was numbered as ITA No.228 of 2018 and the assessee was informed the date of hearing as 19.11.2018. As on the date of hearing the assessee failed to appear before the Tribunal nor was there any representation before the Tribunal. The Tribunal noting the absence of the assessee and observing that the assessee is not interested in prosecuting the case dismissed the appeal for non-prosecution. It is the case of the assessee that the assessee was out of country and she returned to India only on 08.01.2019 and as such she could not be present before the Tribunal on the date of hearing. If that is so, the assessee could have made arrangements to represent her before the Tribunal by any authorized representative or she could have addressed a letter seeking for another date of hearing as she was out of country.

The assessee failed to make arrangement to represent her before the Tribunal and failed to seek for another date of hearing. When there was no representation on behalf of the assessee, the Tribunal had no option but to dismiss the appeal for non-prosecution observing that the assessee had no interest in prosecuting the case. Looking to the conduct of the assessee before the Commissioner of Income Tax (Appeals) and before the ITAT, it could be said that the assessee was not interested in prosecuting the case. Before the Commissioner of Income Tax (Appeals), even though it was brought to the notice of the assessee that appeal is required to be filed in e-mode, the assessee failed to file appeal through e-mode. Before the ITAT also the assessee failed to make arrangements for representation on the date of hearing. Even though delay is considered liberally, in the facts of this case, there are no bonafides and the appellant cannot take benefit of ones own inaction. Hence, we are of the view, that the orders passed by the ITAT is neither perverse nor erroneous. No substantial question of law would arise. Accordingly, the appeal is dismissed.”

We concur with the view of the Ld. DR that the order of the ITAT dated 08.02.2011 was correct & proper and the assessee failed to represent before tribunal on 08.02.2011 despite knowledge of posting of hearing as is recorded in the order itself and no explanation for non-appearance with the sufficient cause has been given for 08.02.2011 when the appeals were called for hearing in these miscellaneous applications.

24. We hold that the power to condone the delay is prescribed by the statute. If the law and the procedure does not provide for the condonation of the delay & for relaxation, the same cannot be allowed.

25. We also hold that decision rendered by the courts should be read in the context in which it was rendered. Therefore decisions relied upon by the Ld. AR cannot be applied to facts of the present case, facts of the case herein are very peculiar & so also the circumstances.

26. We also hold that the Income Tax Act 1961 is self contained code. Wherever the legislature intended to condone the delay the provision have been incorporated in the statute itself. Such provisions are absent in respect of applications u/s 254(2) which is correct section. Further Provisio to Rule 24 of ITAT Rules 1963 the word “afterwards” cannot be interpreted that unlimited period of time is provided for setting aside the exparte order & recalling the appeal. It cannot be said that since no period of limitation is provided for the in the proviso to the Rule 24, the delay of 14 years approximately should be condonable. We hold that the delay of 14 years is a huge delay not liable to be condoned as in the miscellaneous applications nothing is mentioned about “sufficient cause” for non appearance when the appeals were as called on for hearing on 08.02.2011. Hence these two MA’s fails on both counts I.e u/s 254(2) & under proviso to Rule 24 of ITAT Rules 1963. Accordingly both MA’s are dismissed as non-maintainable in law.

27. It is settled legal position that even if an order is void /improper/illegal it requires to be so declared & it is not permissible for any person to ignore the same merely because in his opinion the order is void/improper/illegal. Whether an order is valid or void cannot be determined by the parties and for the purpose of setting aside of such an order even if void, the party has to approach within the time stipulated by law and/or within a reasonable time with a plausible explanation with sufficient cause for non-appearance when the appeals were called for hearing.

28. We say that even assuming that hypothetically the order of the ITAT dated 08.02.2011 is void, not proper, illegal, a nullity and its invalidity is challenged the courts, tribunals, authorities, bodies, forums may refuse to quash the same or interfere with it on the various grounds including the ground of delay or doctrine of waiver or any other legal reason. The order may be void, illegal, not proper for one purpose or for one person, it may not be so for another purpose or another person. The limitation of time has a purpose in law. The limitation point goes to the root of the matter. The limitation has several purpose in law in order to ensure timeline which is essential criteria in our judicial system.

29. Whether the present two miscellaneous applications filed on 05.12.2015 are maintainable in law for setting aside the exparte order of ITAT dated 08.02.2011 for non-persecution u/s 254(2) of the Income Tax Act 1961 r.w. Rule 24 and its proviso, after a lapse of 14 years ? The answer to the above question is no for the simple reason that the section 254(2) contemplates time limit of six months (supra) while the proviso to Rule 24 uses the expression “afterwards” which in our considered view cannot be expanded and/or stretched to such an extent so as to allow relaxation of 14 years in approaching this Tribunal. The Miscellaneous applications are silent on exact date of receipt of ITAT order dated 08.02.2011. It states that in October 2021 (para 12 of MA’s) that the assessee’s came to know of the passing of the ITAT order dated 08.02.2011. These MA’s are filed on 05.12.2025 are therefore clearly time barred u/s 254(2) of the Act 1961 [the correct section] and that same are also not maintainable under the proviso to Rule 24 as the word “afterwards” does not mean and cannot be construed so as to give relaxation of 14 years approximately in law particularly so when no sufficient cause is shown for non-appearance on 08.02.2011 when the appeals were called for hearing. There are no averments and contentions in this regard. Further it is equally hard to believe about the non-service of order dated08.02.2011 when the order of ITAT dated 08.02.2011 was communicated by mode of registered post to the assessee. The registry of ITAT in this regard has established beyond doubt and proved this fact of the dispatch and the contrary is not proved by the assessee except the bare denial of receipt. The presumption under general clauses act (section 27) have not been rebutted at all despite service of ITAT order by registered post, registry’s report in this regard on the assessee. Therefore these above facts are peculiar and so also the circumstances. We therefore, hold that the precedents cited by the Ld. AR are not on these peculiar facts and circumstances & consequently are not applicable.

30. In order to determine the application under proviso to rule 24 of the ITAT rules 1963 the test has to be applied is whether the assessee honestly and sincerely intended to remain present when the appeal was called on for hearing and did his best to do so. “Sufficient cause” is thus the cause, for which the assessee could not be blamed for his absence. Therefore the assessee must approach the tribunal with a “Reasonable Defence”. The most peculiar feature of the present two MA’s is that no reasons are provided for the absence on 08.02.2011 when the appeals were called for the hearing for which the assessee had a prior notice as the order dated 08.02.2011 has recorded this fact. The issue of the prior notice/ knowledge of the hearing for 08.02.2011 is not disputed by the assessee in any manner, whatsoever. Hence the “test” laid down under the proviso to the rule 24, the assessee herein has failed miserably. Hence even under the rule 24 proviso there is thus a total absence of material particulars by the assessee on the issue of “sufficient cause”. The statutory requirement of the proviso to the rule 24 has not been met by the assessee in any manner whatsoever. The real test is of “sufficient cause” for the “non-appearance” when the appeals were called for the hearing and nothing else. The assessee in the MA’s has “miserably failed” to address this cause. The letter and the spirit of the proviso to the rule 24 of the ITAT rules 1963 has not been followed and strictly adhered to obviously for the simple reason that there was “no cause” much less a “sufficient cause” for non-appearance on 08.02.2011 when the appeals were called for the hearing. Therefore no cause under the proviso to the rule 24 of ITAT rules 1963 is made out for the purpose of setting aside the ITAT order dated 08.02.2011 by the assessee.

Even under civil jurisprudence code a strict time line is provided for setting aside of an exparte order.

A plain and simple perusal of MA’s filed shows that there are no material averments with regard to non-appearance on 08.02.2011 when the appeals were called for hearing much less “sufficient cause” which per se makes MA’s non-maintainable statutorily.

31. The above ITA Nos. 188 & 189/Ind/2010 were filed in the year 2010 for A.Y.2007-08 & 2008-09 respectively & that fate of such i.e. appeals came to be known to a corporate assessee only in October 2021. This aspect speaks that right from the beginning i.e. 09.04.2010 [date of filing of appeals] till ‘end’ i.e. 05.12.2025 [date of filing of MA’s] the assessee was in a slumber mode an approach wholly untenable in law & not acceptable in fiscal statutes where strict time line are laid down under the Act. It shows negligence of the assessee not to take proceedings seriously & to pursue the same effectively & further to take time basis whims & fancy. The assessee was not vigilant, law helps those who are vigilant & not those who sleep over on their rights. Assessee herein is asserting right not realising a fact that he had a corresponding obligation to pursue remedy available in law within a time limit.

32. It is avered in the MA’s that the assessee company came to know of about the impugned order dated 08.02.2011 only in October 2021. Further on advice of senior advocate the assessee company awaited filing of revival/restoration applications as immediate relief was not feasible while the issue was pending before the Hon’ble Supreme Court. Therefore the present application is being filed in November 2025 after the final adjudication by the Hon’ble Supreme Court in civil appeal no.7257/2011Bharti Cellular Ltd. v. Asstt. CIT (SC). It is also avered that the Rule 24 of the ITAT Rules 1963 does not prescribe any limitation period for filing an application for rectification. In this regard we hold that even assuming but without conceding that the assessee came to know of the impugned order dated 08.02.2011 on October 2021 & did not take any steps either u/R 24 &/or section 254(2) as no favourable relief was possible from this Tribunal as the larger issue was pending before the Hon’ble Supreme Court (as stated aforesaid) that ipso facto does not mean that the assessee company should not take any steps in law either under Rule 24 &/or 254(2) & /or both. Mere expectation that a favourable relief would not be granted by the tribunal due to aforesaid reason of pendency before the Hon’ble Supreme Court does not mean that the assessee should not take any steps whatsoever as aforesaid. The assessee company ought to have taken steps as per law within time limit statutorily fixed by law but they choose not to exercise their rights for which law cannot be moulded & stretched to such an extend so as to allow these MA’s as the consequences would not only be against the law but would lead to the unprecedent situations whereby each & every the assessee would say that they choose not to file an application because of advice that no relief would be possible as the matter is pending in the Hon’ble Supreme Court. In our considered view the assessee company ought to have filed these MA’s within the time stipulated by the law only u/s 254(2) (supra). With regard to the assessee’s plea that the Rule 24 of the ITAT Rules 1963 does not stipulate any limitation period we hold clearly that just because there is no period of limitation is mentioned that “ipsofacto” does not mean that the assessee company can come any time of it’s choice for the revival of any ex-parte order if such an approach is allowed then each & every assessee would come to this Tribunal under Rule 24 at time chosen by them on their whims & fancy. The law of limitation u/s 254(2) is strict & u/s 24 the use of the words afterwards” does not mean that the assessee company can knock the door of this tribunal after a lapse of 14 years. We hold that the stale matters cannot be revived in law in such a manner as this Tribunal is a creature of a statute & we have to adhere to the strict time line provided by the statute. We cannot give any extension of time limit provided by law in the absence of any provision of law with regard to the condonation of delay in this regard. If we give any leeway we would be doing violence to the plain & simple meaning of the statute on time line & would render the law redundant & otiose. The unintended result & consequences would result in such a situation. It would open flood gates for MA’s resulting in chaos. The finality of order would suffer. Equity & justice would suffer too. To sum up we also hold that there is a fixed period of time u/s 254(2) for the assessee to take steps which they did not do so & that there is no provision in law to condone the delay u/s 254(2) of the Act.

Order

33. In the premises drawn up by us both these miscellaneous applications are not maintainable and are dismissed.