Raw, unprocessed Psyllium seeds sold via APMC directly from farmers are exempt from GST.

Issue

-

Whether raw, unprocessed Psyllium (Isabgol) seeds procured from farmers via APMC auctions and supplied without any form of processing are exempt from GST under Entry 87 (HSN 1211) of Notification No. 10/2025-Central Tax (Rate).

Facts

-

The applicant is a GST-registered proprietorship based in Gujarat that proposes to trade Psyllium (Isabgol) seeds.

-

The seeds are to be procured directly from farmers through Agricultural Produce Market Committee (APMC) auctions under a valid commission agent license.

-

The procured seeds will be stored in a registered warehouse and subsequently supplied to processing units within the same state.

-

The seeds will be sold in the exact same condition as harvested, without undergoing any cleaning, grading, artificial drying, dehydration, freezing, or any other industrial processing.

Decision

-

Held, Psyllium (Isabgol) seeds supplied in their natural, raw, and unprocessed form qualify as “fresh” Isabgol seeds under the law.

-

Held, because the seeds do not undergo any post-harvest processing like crushing, freezing, or artificial drying, they satisfy the criteria of Entry 87 under HSN 1211.

-

Held, the transaction is entirely exempt from tax under Entry 87 of Notification No. 10/2025-Central Tax (Rate) dated September 17, 2025, ruling in favor of the assessee.

Key Takeaways

Preservation of Raw Status: Agricultural seeds or plant parts retain their “fresh” status and eligibility for tax exemptions as long as they are traded in their natural state without any value-adding industrial processing.

APMC Direct Sourcing: Procuring raw produce directly from farmers via official channels like APMC auctions for onward supply to processing factories does not change the tax-exempt character of the primary agricultural product.

| i. | Procurement of Psyllium seeds (Isabgol) directly from farmers through Agricultural Produce Market Committee (APMC) auctions. |

| ii. | Storage of such seeds in godowns without any processing. |

| iii. | Supply of the said Psyllium seeds (Isabgol), without any processing, to Isabgol processing units engaged in extraction of Psyllium (Isabgol) husk. |

| iv. | The commodity proposed to be traded is raw Psyllium seeds (Isabgol) that will be procured from the farmers by APMB after threshing (operation of separating the grains from the plants done by the farmers, without any alteration in form, character or composition). |

| v. | At no stage, either prior to purchase from farmers or prior to subsequent sale, do the Psyllium seeds (Isabgol) undergo any processing or treatment. There is no cleaning, sorting, grading, roasting, drying, freezing or any other activity which alters the form, character or essential nature oi the seeds. The seeds remain in same condition from point of harvest to purchase of trader from farmers and upto the point of supply to the processing units. There is no intervention or value addition after harvesting. |

| vi. | In established trade and agricultural practice, Psyllium seeds (Isabgol) are simply known as “Isabgol seeds” and there is no such recognised commercial or agricultural distinction between fresh, dried or frozen Psyllium seeds; that such terms as fresh, dried or frozen for Psyllium seeds arises only from GST circular and FAQs and not from actual agricultural or market practice. Hence, the distinction between “Fresh or Chilled” and “Dried or Frozen” might be required for other such seeds but in case of Psyllium seeds, they are always “fresh” and never be in “Dried or Frozen’ condition. |

| (a) | Whether Psyllium Seeds (Isabgol) supplied in their natural, raw and unprocessed form as procured through Agricultural Produce Market Committee (APMC) auctions directly from farmers, without undergoing any drying, freezing, crushing or other processing qualifies as “fresh” Isabgol seeds and are exempted under Entry 87 (HSN 1211) of Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025 as “Plants and parts of plants (including seeds and fruits) of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, fresh or “chilled”? |

| (b) | Alternatively, whether Psyllium Seeds (Isabgol) as discussed above qualifies as “goods of seed quality” and are exempt from GST under Entry 77 (HSN 12) of Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025?” |

| • | Psyllium seeds (Isabgol) are classifiable under Chapter 12 of the Customs Tariff, which covers oil seeds, miscellaneous grains, seeds and fruits; industrial or medicinal plants. Specifically, Psyllium seeds (Isabgol) are covered under tariff item 12119013. |

| • | Chapter 12 expressly covers seeds and other agricultural produce and Psyllium seeds being seeds obtained directly from cultivation and supplied without processing, squarely fall under this Chapter. |

| • | The following entries are relevant for the present application. |

| 1. | As per Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 87 (covering HSN 1211) which reads as ‘Plants and parts of plants (Including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, fresh or chilled, exempts the product from GST. |

| 2. | As per Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 77 (covering HSN 12) reads as ‘All goods of seed quality’ exempts the product from GST. |

| 3. | As per Notification No. 09/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 71 (covering HSN 1211) reads as ‘Plants and parts of plants (Including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, frozen or dried, whether or not cut, crushed or powdered.” GST rate here is 5%. |

| • | As per FAQ F.No.332/2/2017-TRU dated December, 2017, CBIC clarified that Isabgol seeds are classifiable under heading 1211, that fresh Isabgol seeds attract NIL rate of GST whereas dried Isabgol seeds attract 5% GST & that Isabgol husk falls under heading 1211 attracting GST rate oi 5%. |

| • | While FAQ draws distinction between ‘fresh’ and ‘dried or frozen’ Isabgol seeds for GST purposes, it does not define the scope or meaning of the expression ‘fresh’ in the context of Isabgol seeds; that in established agricultural and commercial practice, there is no marketable product such as ‘Dried Isabgol seeds’ or ‘Frozen Isabgol seeds’ in wholesale or retail trade. Psyllium seeds (Isabgol) are traded as it is, after being harvested, in the same form (fresh form) without any further categorisation. Hence, seeds supplied in natural, unprocessed form must be treated as fresh. |

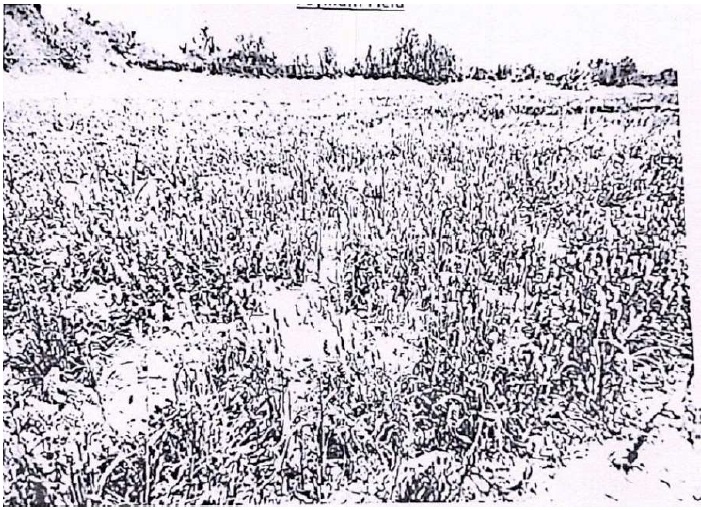

| • | The Psyllium seeds (Isabgol) are agricultural produce obtained from the plant Plantago ovata and the seeds are cultivated by farmers as a seasonal agricultural crop and are harvested in seed form after maturity. |

| • | The applicant proposes to purchase such Psyllium seeds (Isabgol) directly from farmers through APMC auctions without any processing, and further such seeds will be supplied to the processing units; that the applicant will be engaged in mere trading activity and will not undertake any activity that alters the form, character, composition or essential nature of the Psyllium seeds (Isabgol) at any stage. |

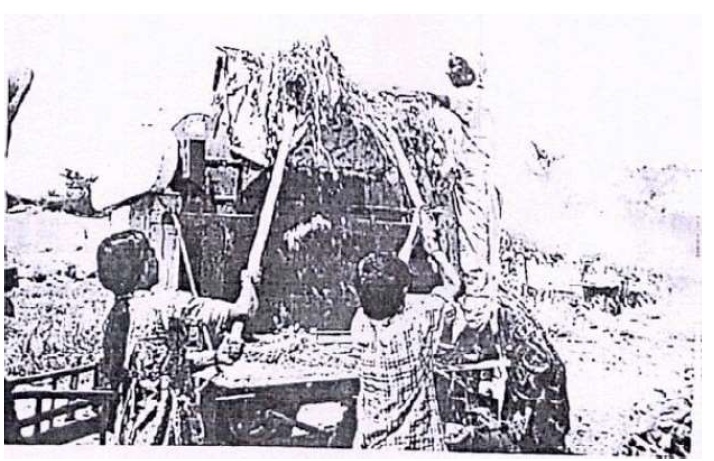

| • | Psyllium (Plantago ovata) is cultivated by farmers following standard agricultural produce and after the crop matures, farmers remove the whole plant from the field and the harvested plants are subjected to threshing, whereby seeds are separated from the spikes, straw and dust; that threshing is an integral and unavoidable agricultural activity carried out to separate the seeds from the plant and does not amount to processing or manufacture as it is a part of harvesting process; that the output at this stage is raw Psyllium seeds (isabgol), retaining their original botanical and physical characteristics. |

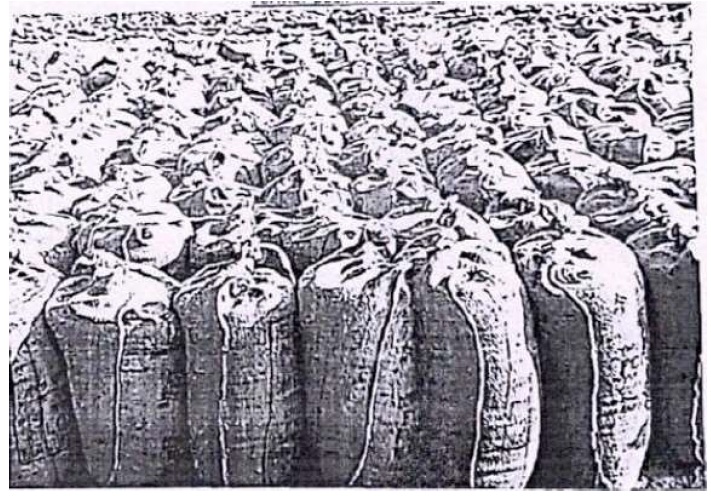

| • | After threshing, the psyllium seeds (isabgol) are packed in gunny bags in the same condition as harvested and transported by farmers to APMC mandis for sale through auction; that at the time oi sale in APMC mandi, the psyllium seeds remain whole and intact, retain natural moisture content and are not subjected to drying, freezing, grading, roasting, polishing, crushing, or any chemical or mechanical treatment. Thus at the primary sale stage, the Psyllium seeds (isabgol) are unprocessed agricultural produce. |

| • | The applicant proposes to purchase Psyllium seeds (isabgol) from farmers strictly through the APMC auction mechanism and the same will be procured in the same condition in which they are brought by farmers, without any intervention or alteration and after procurement, the applicant will store the psyllium seeds (isabgol) in dry and ventilated godowns to preserve their natural condition; that no artificial or intentional drying, no dehydration, no freezing and no processing of any kind will be undertaken at any stage by the applicant; that the psyllium seeds (isabgol) shall remain in the same natural form so harvested by the farmers, without any change or alteration, from the stage oi procurement up to their supply to the processing unit; that the applicant supplies psyllium seeds (isabgol) as raw material to isabgol processing units; that there is no proposal to undertake husk separation or any other processing activity; that processing will be carried out only by the processing units, where mechanical separation of the husk from the seed takes place resulting in Psyllium (isabgol) husk, which is a processed product; that the husk is a processed product, whereas the seeds remain agricultural raw material; that psyllium seeds (isabgol) shall be traded exclusively as agricultural produce and shall be supplied only as raw material to processing units for further processing, namely Psyllium (isabgol) husk; that the seeds in the form proposed to be supplied by the applicant, shall have no direct consumable or therapeutic use and shall be marketed or sold as a finished product. |

| • | The whole process flow of trade of psyllium seeds (isabgol) in brief, is as under: |

| 1. | Cultivation by farmers: Psyllium is cultivated as a seasonal agricultural crop using standard farming practices i.e. seeds are sown, irrigated and grown naturally in open fields, crops mature in the field, generally during the months of March-April depending on climactic conditions. |

| 2. | Harvesting by farmers: After maturity, the entire plant is cut close to the ground using sickles or similar manual tools. |

| 3. | Threshing by farmers: Harvested plants are fed into a thresher machine where seeds are separated from spikes, straw and dust. Loose straw, chaff and visible dust are separated during threshing and no grading, polishing or chemical treatment is done & seeds are obtained. |

| 4. | Packing by farmers: Seeds obtained after threshing are directly collected and packed in jute bags or PP bags without any treatment. |

| 5. | Transportation to mandi bv farmers: Packed bags are transported by tractors, carts or trucks to the nearest APMC mandi for sale. |

| 6. | Primary sale to APMC: Psyllium seeds (Isabgol) are sold through auction in APMC mandis and mandis only facilitates regulated sale and does not involve any processing. |

| 7. | Procurement by APMC agent: Traders procure Psyllium Seeds directly from farmers through APMC auctions in the same condition as brought by the farmers. |

| 8. | Storage at APMC: Seeds are stored in dry and ventilated godowns to prevent moisture damage. Manual removal of visible foreign matter such as straw or dust, if required is done and no mechanical clearing, grading, or polishing is undertaken. |

| 9. | Supply by APMC agent to processing unit: Seeds are supplied as received without drying, dehydration, freezing, grading, polishing, roasting, milling, crushing or any chemical treatment. The applicant supplies Psyllium seeds without undertaking husk separation & husk separation is done mechanically by the processing units. |

| • | Psyllium seeds (Isabgol) are plants or parts of plants (including seeds) used primarily in pharmacy as the seeds constitute the source material for extraction of Psyllium husk which is a recognised pharmaceutical and nutraceutical ingredient. When supplied in fresh condition, they are exempted under Sr. No. 87 of Notfn. No. 10/2025-Central Tax (Rate) dated 17.09.2025. |

| • | The term fresh’ is not defined in GST law, however, fresh agricultural produce refers to goods supplied in the same state as harvested without undergoing any drying or freezing process. In present case, no artificial drying or freezing process is carried out. Natural low moisture content is an inherent characteristic of Psyllium seeds and cannot be equated with ‘dried’ goods. |

| • | Process of drying is discussed in para 3.2. of Circular No. 169/19/2021-GST dated 06.10.2021 as under: “Fresh fruit and nuts would thus cover fruit and nuts which are meant to be supplied in the state as plucked. They continue to be fresh even if chilled. However, fruit and nuts do not qualify as fresh, once frozen (cooked or otherwise), or intentionally dried to dehydrate including through sun drying, evaporation or freezing, for supply as dried fruits or nuts.” |

| • | Psyllium seeds are proposed to be procured directly from farmers through APMC auction and shall be supplied in fresh condition, without undergoing any process such as drying, freezing, crushing, grading, polishing or chemical treatment; that these seeds shall be supplied in the same state as harvested and shall retain their original character, identity and essential attributes as agriculture produce; that psyllium seeds (isabgol) are plants or parts of plants used primarily in pharmacy as they constitute the source material for extraction of psyllium husk, which is a recognised pharmaceutical and nutraceutical ingredient and when supplied in fresh and unprocessed condition, the said goods are exempt from GST as per Sr.No. 87 of Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025. |

| • | Alternatively, the Psyllium seeds (Isabgol) are capable of germination and can be supplied in seed form as harvested from farmers which would also qualify for exemption as per Sr.No. 77 oi Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025. |

| • | The term ‘goods of seed quality’ is generally understood to refer to seeds that are viable, capable oi germination and suitable for sowing or cultivation and such goods retain their basic character as planting material; that in the present case, the psyllium seeds supplied are in their natural, unprocessed form and are capable of germination, hence, they also fall within the scope of ‘goods oi seed quality.’ |

| • | The applicant has concluded his submission by stating that the proposed supply of psyllium seeds (isabgol) is wholly exempt from GST and seeks a clear ruling to the effect to avoid unwarranted litigation. |

| (a) | Whether Psyllium Seeds (Isabgol) supplied in their natural, raw and unprocessed form as procured through Agricultural Produce Market Committee (APMC) auctions directly from farmers, without undergoing any drying, freezing, crushing or other processing qualifies as “fresh” Isabgol seeds and are exempted under Entry 87 (HSN 1211) of Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025 as “Plants and parts of plants (including seeds and fruits) of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, fresh or “chilled”? |

| (b) | Alternatively, whether Psyllium Seeds (Isabgol) as discussed above qualifies as “goods of seed quality” and are exempt from GST under Entry 77 (HSN 12) of Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025?” |

| 1. | Heading 1207 applies, inter alia, to palm nuts and kernels, cotton seeds, castor oil seeds, sesamum seeds, mustard seeds, safflower seeds, poppy seeds and shea nuts (karite nuts). It does not apply to products of heading 0801 or 0802 or to olives (Chapter 7 or Chapter 20). |

| 2. | Heading 1208 applies not only to non-defatted flours and meals but also to flours and meals which have been partially defatted or defatted and wholly or partially defatted with their original oils. It does not, however, apply to residues of headings 2304 to 2306. |

| 3. | For the purposes of heading 1209, beet seeds, grass and other herbage seeds, seeds oi ornamental flowers, vegetable seeds, seeds of forest trees, seeds of fruit trees, seeds of vetches (other than those of the species Vida faba) or of lupines are to be regarded as “seeds of a kind used for sowing”. Heading 1209 does not, however, apply to the following even if for sowing: |

| (a) | leguminous vegetables or sweet corn (Chapter 7); |

| (b) | spices or other products of Chapter 9; |

| (c) | cereals (Chapter 10); or |

| (d) | products of headings 1201 to 1207 or 1211. |

| 4. | Heading 1211 applies, inter alia, to the following plants or parts thereof: basil, borage, ginseng, hyssop, liquorice, all species of mint, rosemary, rue, sage and wormwood. Heading 1211 does not, however, apply to: |

| (a) | medicaments of Chapter 30; |

| (b) | perfumery, cosmetic or toilet preparations of Chapter 33; or |

| (c) | insecticides, fungicides, herbicides, disinfectants or similar products of heading 3808. |

| 5. | For the purposes of heading 1212, the term “seaweeds and other algae” does not include : |

| (a) | dead single-cell micro-organisms of heading 2102; |

| (b) | cultures of micro-organisms of heading 3002; or |

| (c) | fertilizers of heading 3101 or 3105. |

| 1211 | PLANTSAND PARTS OF PLANTS (INCLUDING SEEDSAND FRUITS), OF A KIND USED PRIMARILY IN PERFUMERY, IN PHARMACY OR FOR INSECTICIDAL, FUNGICIDAL OR SIMILAR PURPOSE, FRESH OR DRIED, WHETHER OR NOT CUT, CRUSHED OR POWDERED | |

| 1211 20 00 | – | Ginseng roots |

| 1211 30 00 | – | Coca leaf |

| 1211 40 00 | – | Poppy straw |

| 1211 50 00 | – | Ephedra |

| 1211 60 00 | – | Bark of African cherry (Prunus africana) |

| 1211 90 | – | Other: |

| – | Seeds, Kernel, Aril, Fruit, Pericarp, Fruit rind, Endosperm, Mesocarp, Endocarp: | |

| 1211 90 11 | – | Ambrette seeds |

| 1211 90 12 | – | Nuxvomica, Dried ripe seeds |

| 1211 90 13 | – | Psyllium seeds (isobgul) |

| 1211 90 14 | – | Neem seeds |

| 1211 90 15 | – | Jojoba seeds |

| 1211 90 16 | – | Garcinia |

| 1211 90 19 | – | Other |

| – | Leaves, Leaf bud, Galls, flowers, Inflorescence, Spadix, Flower bud, Style and Stigma, Stamen and pods: | |

| 1211 90 21 | – | Belladona leaves |

| 1211 90 22 | – | Senna leaves and pods |

| 1211 90 23 | – | Neem leaves |

| 1211 90 24 | – | Gymnema |

| 1211 90 25 | – | Cubeb |

| – | ||

| 1211 90 26 | – | Pyrethrum |

| 1211 90 29 | – | Other |

| – | Bark, Husk and Rind: | |

| 1211 90 31 | – | Cascara sagrada bark |

| 1211 90 32 | – | Psyllium husk (isobgul husk) |

| 1211 90 33 | – | Gamboge fruit rind |

| 1211 90 34 | – | Ashoka (Saraca asoca) |

| 1211 90 35 | – | Arjuna (Terminalia arjuna) |

| 1211 90 39 | – | Other |

| – | Roots, Root stalk, Bulb, Corn, Tuber, Stolon and rhizome: | |

| 1211 90 41 | – | Belladona roots |

| 1211 90 42 | – | Galangal rhizomes and roots |

| 1211 90 43 | – | Ipecac dried rhizome and roots |

| 1211 90 44 | – | Serpentina roots (rowwalfia serpentina and other species of rowwalfias) |

| 1211 90 45 | – | Zedovary roots |

| 1211 90 46 | – | Kuth root |

| 1211 90 47 | – | Sarasaparilla roots |

| 1211 90 48 | – | Sweet flag rhizomes |

| 1211 90 49 | – | Other |

| – | ||

| – | Whole Plant, Aerial Part, Stem, Shoot and Wood: | |

| 1211 90 51 | – | Sandalwood chips and dust |

| 1211 90 52 | – | Vinca rosea herbs |

| 1211 90 53 | – | Mint |

| 1211 90 54 | – | Agarwood |

| 1211 90 55 | – | Chirata |

| 1211 90 56 | – | Basil, hyssop, rosemary, sage and savory |

| 1211 90 57 | – | Ashwagandha (Withania somnifera) |

| 1211 90 58 | – | Giloy (Tinospora cordifolia) |

| 1211 90 59 | – | Other |

| 1211 90 90 | – | Other |

1211.20 – Ginseng roots

1211.30 -Coca leaf

1211.40 – Poppy straw

1211.50 -Ephedra

1211.90 – Other

| (a) | Products of this heading, unmixed, but put up in measured doses or in forms or packings for retail sale, whether for therapeutic or prophylactic purposes, or put up for retail sale as perfumery products or as insecticidal, fungicidal or similar products. |

| (b) | Products which have been mixed for use for the purposes described in (a) above. |

| (a) | mixtures consisting of different species of plants or parts of plants of this heading (heading 21.06); |

| (b) | mixtures of plants or parts of plants of this heading with vegetable products falling in other Chapters (e.g., Chapters 7, 9, II) (Chapter 9 or heading 21.06). |

Aconite (Aconitum napellus): roots and leaves.

Ambrette (musk) (Hibiscus abelmosc/ws) : seeds.

Angelica (Archangelica officina/is) : roots and seeds.

Angostura (Galipea officinalis): bark.

Araroba (Andira araroba) : powder. Arnica (Arnica montana): roots, stems, leaves and flowers.

Basil (Ocimum basilicum): flowers and leaves.

Bearberry (Uva ursi) : leaves.

Belladonna (Atropa belladonna): herbs, roots, berries, leaves and flowers. Boldo (Peumus boldus): leaves.

Borage (Borago officinalis): stems and flowers.

Bt-yony (Blyonia dioica) : roots. Buchu (Barosma betulina, Barosma serratifo/ia and Barosma crenulata): leaves.

Buckbean (Menyanthes trifoliata): leaves.

Burdock (Arctium lappa) : Seeds and dried roots.

Calabar (Physostigma venenosum): beans.

Calamus (Acarus calamus) : roots. Calumba (Jateorhiza palmata): roots.

Cannabis (Cannabis sativa): herbs.

Cascara sagrada (Rhamnus purshiana) :bark.

Cascarilla (Croton el uteri (a) :bark.

Cassia (Cassia fistula): pods and unpurified pulp. (Purified cassia pulp (aqueous extract) is classified in heading 13.02.)

Centauria (Elythraea centaurium) : herbs.

Cevadilla (Sabadilla) (Schoenocaulon officina/e): seeds.

Chamomile (Matricaria chamomilla, Anthemis nobilis) : flowers.

Chenopodium: seeds.

Cherry: stalks.

Cherry laurel (Pnmus laurocerasus) : berries. Cinchona : bark.

Clove (Cmyophyllus aromaticus) : bark and leaves.

Coca (Elythroxylon coca and Elythroxylon truxi/lense) : leaves.

Cocculus indicus (Indian berry) (Anamirta paniculata): fruit.

Cocillana (Gumea rusbyi) : bark.

Colchicum (Colchicum autumnale): corms and seeds. Colocynth (Citmllus co/ocynthis): fruit.

Comfrey (Symphytum officinale) : roots. Condurango (Marsdenia condurango) : bark.

Couchgrass (Triticum) (Agropyrum repens) : roots. Cube (barbasco or timbo) (Lonchocmpus nicou) : bark and roots. Cubeb (Cubeba officina/is Miquel or Piper cubeba): powder.

Damiana (Turnera diffusa): leaves.

Dandelion (Taraxacum officinale): roots.

Datura metel: leaves and seeds.

Derris (or tuba) (Derris el/iptica and Derris trifoliata): roots.

Digitalis (Digitalis pwpurea): leaves and seeds.

Elder (Sambucus nigra) : flowers and bark.

Ephedra (Mahuang) : stems and branches.

Ergot of rye. Eucalyptus (Eucalyptus g/obu!us): leaves.

Frangula: bark.

Fumitory (Fumaria officinalis) : leaves and flowers.

Galangal (Aipinia officinarum): rhizomes.

Gentian (Gentiana lutea) : roots.

Ginseng (Panax quinquefolium and Pan ax ginseng)roots.

Golden seal (Hydrastis) (Hydrastis canadensis): roots.

Guaiacum (Guaiacum officinale and Guaiacum sanctum): wood.

Hamamelis (witch hazel) (Hamamelis virginiana) : bark and leaves.

Hellebore (Veratrum album and Veratrum viride) : roots.

Henbane (Hyoscyamus) (Hyoscyamus niger) : roots, seeds and leaves. Horehound (Marrubium vulgare) : herbs and stems.

Hyssop (Hyssopus officinalis) : flowers and leaves.

Ipecacuanha (Cephaelis ipecacuanha): roots.

Ipomoea (Ipomoea orizabensis) : roots.

Jaborandi (Pilocmpusjaborandi and Pi/ocmpus microphyllus): leaves.

Jalap (Ipomoea purga): roots. Lavender (Lavandula vera) : flowers and herbs.

Leptandra (Veronica virginica): roots.

Linaloe (Bursera delpechiana):wood.

Linden (Tilia europaea): flowers and leaves.

Liquorice (Glycyrrhiza glabra): roots.

Lobelia (Lobelia inj/ata): herbs and flowers.

Long pepper (Piper longum): roots and underground stems.

Male fern (Dl)’Opteris filix-mas) : root.

Mallow (Malva silvestris and Malva rotundifolia): leaves and flowers.

“Mandrake : roots or rhizomes. Marjoram (see “Wild mmj_oram” below). Marshmallow (Althaea ojjicinalis) : flowers, leaves and roots.

Melissa (Melissa officinalis): leaves, flowers and tops. Mint (all species). Mousse de chene (oak moss) (Everniafwjitracea) (a lichen).

Mugwort (Artemisia vulgaris) :roots. Nux vomica (Stl)clmos nux-vomica) : seeds.

Orange tree (Citrus aurantium): leaves and flowers.

Orris (Iris germanica, Iris pal/ida and Iris fiorentina) : roots.

Pansy: flowers.

Patchouli (Pogostemon patchouli): leaves. Peppermint (see mint). Pine: buds.

Plantago psyllium : herbs and seeds.

Podophyllum (Podophyllum pe/tatum): roots or rhizomes.

Poppy (Papaver somniferum): heads (unripe, dried).

Pulsatilla (Anemone pulsatilla) :herbs.

Pyrethrum (Chi)’Santhemum cinerariaefolium): leaves, stems and flowers.

Pyrethrum (Anacyc/us pyrethrum):roots.

Quassia (Quassia amara and Picraena excel sa) : wood and bark.

Quince: seeds.

Rhatany (Krameria triandra) : roots.

Rhubarb (Rheum officina/e): roots. (Rose : flowers.

Rosemary (Rosmarilws officina/is) : herbs, flowers and leaves.

Rue (Rut a graveolens): leaves.

Sage (Salvia officinalis) : leaves and flowers.

St. Ignatius beans (Stlychnos ignatii).

Sandalwood: chips (white and yellow).

Sarsaparilla (Smilax): roots.

Sassafras (Sassafras officina/is) : bark, roots and wood.

Scammony (Convolvulus scammonia): roots.

Senega (Polygala senega):roots.

Senna (Cassia acutifo/ia and Cassia angustifolia): pods and leaves.

Slippery elm (Lllmus fillva) : bark.

Solanum nigrum.

Squill (Urginea maritima, Urginea scilla): bulbs.

Stramonium (Datura stramonium) : leaves and tops.

Strophanthus (Strophanthus kombe) : seeds.

Tansy (Tanacetum vulgare) : roots, leaves and seeds.

Tonka (tonquin) (Dipterix odorata) : beans.

Valerian (Valeriano officina/is): roots.

Verbascum (mullein) (Verbascum thapsus and Verbascum phlomoides): leaves and flowers.

Verbena: leaves and tops.

Veronica (Veronica officinalis): leaves.

Viburnum (Viburnum prunifo/ium): root bark.

Violets (Viola odorata): roots and dried flowers.

Walnut: leaves.

Wild marjoram (Origanum vulgare); sweet marjoram (Majorana hortensis or Origanum majorana) is excluded (Chapter 7).

Woodruff (Asperula odorata) : herbs.

Wormseed (Artemisia cina): flowers.

Wormwood (Artemisia absinthium): leaves and flowers.

Yohimba (Col)’lwnthejohimbe): bark.

| 1. | As per Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 87 (covering HSN 1211) which reads as ‘Plants and parts of plants (Including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, fresh or chilled, exempts the product from GST. |

| 2. | As per Notification No. 10/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 77 (covering HSN 12) reads as ‘All goods of seed quality’exempts the product from GST. |

| 3. | As per Notification No. 09/2025-Central Tax (Rate) dated 17.09.2025, Entry No. 71 (covering HSN 1211) reads as ‘Plants and parts of plants (Including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, frozen or dried, whether or not cut, crushed or powdered.” GST rate here is 5%. |

| (i) | cultivation by farmers followed by |

| (ii) | harvesting of the plants, |

| (iii) | threshing of the plants in a thresher through which psyllium seeds are obtained, |

| (iv) | collecting and packing of seeds by farmers in PP bags, |

| (v) | transport of seeds to APMC mandis through tractors, carts or trucks, |

| (vi) | primary sale to APMC through auction in APMC mandis, |

| (vii) | procurement of psyllium seeds by APMC agent from farmers through APMC auctions in the same condition as brought by farmers, |

| (viii) | Storage of seeds in dry and ventilated godowns to prevent moisture damage where manual removal of visible foreign matter such as straw or dust, if required is done and no mechanical clearing, grading, or polishing is undertaken. |

| (ix) | Supply of seeds as received without drying, dehydration, freezing, grading, polishing, roasting, milling, crushing or any chemical treatment to the processing units. Husk separation from psyllium seeds is done mechanically by the processing units. |

| (i) | 2.5 per cent, in respect of goods specified in Schedule I; |

| (ii) | 9 per cent, in respect of goods specified in Schedule II; |

| (iii) | 20 per cent, in respect of goods specified in Schedule III; |

| (iv) | 1.5 per cent, in respect of goods specified in Schedule IV; |

| (v) | 0.125 per cent, in respect of goods specified in Schedule V; |

| (vi) | 0.75 per cent, in respect of goods specified in Schedule VI, and |

| (vii) | 14 per cent, in respect of goods specified in Schedule VII, |

| S.No. | Chapter/Heading/Sub-heading/Tariff item | Description of goods |

| (1) | (2) | (3) |

| 71 | 1211 | Plants and parts of plants (including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, frozen or dried, whether or not cut, crushed or powdered. |

| S.No. | Chapter/Heading/Sub-heading/ Tariff item | Description of goods |

| (D | (2) | (3) |

| 77 | 12 | All goods of seed quality |

| 87 | 1211 | Plants and parts of plants (including seeds and fruits), of a kind used primarily in perfumery, in pharmacy or for insecticidal, fungicidal or similar purpose, fresh or chilled |