The Lakshadweep Excise Regulation 2026 No 7 of 2026

![]()

The Gazette of India

CG-DL-E-05062026-273174

EXTRAORDINARY

PART II — Section 1

PUBLISHED BY AUTHORITY

No. 22] NEW DELHI, FRIDAY, JUNE 5, 2026/JYAISHTHA 15, 1948 (Saka)

Separate paging is given to this Part in order that it may be fi led as a separate compilation.

MINISTRY OF LAW AND JUSTICE

(Legislative Department)

New Delhi, the 5th June, 2026/Jyaishtha 15, 1948 (Saka)

THE LAKSHADWEEP EXCISE REGULATION, 2026

NO 7 of 2026

Promulgated by the President in the Seventy-seventh Year of the Republic of India.

A Regulation to provide for regulating the manufacture, possession, import, export,

transport, purchase, sale and consumption of liquor and levy of excise duty on

them, in the Union territory of Lakshadweep and for matters connected

therewith or incidental thereto.

In exercise of the powers conferred by article 240 of the Constitution, the

President is pleased to promulgate the following Regulation made by her:

CHAPTER I

PRELIMINARY

1. (1) This Regulation may be called the Lakshadweep Excise

Regulation, 2026.

(2) It extends to the whole of the Union territory of Lakshadweep.

(3) It shall come into force on such date as the Administrator may, by

notification in the Official Gazette, appoint.

2. In this Regulation, unless the context otherwise requires,

(1) Administrator means the Administrator of the Union territory of

Lakshadweep appointed by the President under article 239 of the Constitution;

(2) alcohol means ethyl alcohol of any strength and purity having the

chemical composition C2H5OH;

(3) alcoholic beverage means a beverage or a liquor or a brew

containing more than 0.5 per cent. above the ethanol limit used in the

production of alcoholic beverage, which shall be of agricultural origin,

provided that its limit shall be zero in case of alcohol-free beer;

(4) Appellate Authority means the Appellate Authority referred to in

section 84;

(5) authorised officer means an officer authorised by the

Administrator to exercise such powers and perform such duties and functions

under the provisions of this Regulation and the rules framed thereunder;

(6) beer means an alcoholic beverage prepared from malt or grain with

or without addition of sugar and hops and includes black beer, ale, stout, porter

and such other substance as may be specified by the Administrator, by

notification.

Explanation. For the purposes of this clause, hops mean ripened

cones of female hop plant used for giving flavour to malt liquor;

(7) black jaggery means coarse brown sugar made from palm trees or

cane juice ordinarily unfit for human consumption, but contains sufficient

quantity of fermentable sugar for manufacture of ethyl alcohol;

(8) blending means mixing of two or more spirits of different strengths

and different qualities;

(9) description as may be or as may have been permitted by the Excise

Commissioner from time to time and includes can and pouch;

(10) brewery means premises where beer is manufactured and

includes every place therein where beer is stored or wherefrom it is issued;

(11) compounding means the manufacture of alcoholic beverage by

addition to spirit of a flavouring or colouring matter or both;

(12 contagious d

spread rapidly from person to person through direct contact (touching a person

who has the infection), indirect contact (touching a contaminated object), or

droplet contact (inhaling droplets made when a person who has the infection

coughs, sneezes, or talks);

(13) country liquor or traditional liquor means plain or spiced spirit

which has been manufactured in India from material recognised as base for

country or traditional spirit, namely, mahua, rice, gur, molasses or other

traditional spirit;

(14) denaturant means any substance completely miscible in spirit and

of such a character that its addition renders the material, or any aqueous

dilution of it, non-potable;

(15) Deputy Commissioner means the Deputy Commissioner

appointed or designated under section 5;

(16) District Excise Officer means the District Excise Officer

appointed or designated under section 5;

(17) Excise Commissioner means the officer appointed or designated

as Excise Commissioner by the Administrator under section 3;

(18) Excise Officer means any officer or person appointed or invested

with powers under this Regulation;

(19) excise revenue means revenue derived or derivable from any

payment, duty, fee, tax, confiscation or fine imposed or ordered under this

Regulation, or of any other law for the time being in force relating to liquor,

but does not include fine imposed by a Court of law;

(20) export means to take out of the Union territory of Lakshadweep

to any other State or Union territory within the country;

(21) foreign liquor means any liquor imported by land, sea or air, into

India;

(22) Government means the Union territory Administration of

Lakshadweep;

(23) import means to bring into the Union territory of Lakshadweep

from any other State or Union territory of the country;

(24) Indian liquor means liquor manufactured in India by process

of distillation or using alcohol obtained by distillation, such as, whisky,

brandy, rum, gin, vodka, but does not include country liquor or fermented

liquor.

Explanation. For the purposes of this clause, fermented liquor

means liquor obtained by the process of fermentation and includes beer, ale,

stout, porter wine and any other similar liquor;

(25) licence means a licence granted under this Regulation;

(26) liquor means any alcoholic beverage and includes whisky,

brandy, beer, wine, toddy, vodka, gin, tequila, country liquor, arrack and

intoxicating liquid consisting of or containing alcohol besides any similar

substance which the Administrator may, by notification, declare to be liquor

for the purposes of this Regulation;

(27) malt means germinated barley;

(28) manufactory means any distillery, brewery, winery or any

establishment distilling, brewing, manufacturing, blending or bottling liquor.

Explanation. For the purposes of this clause,

(a

includes every place therein where it is stored or wherefrom it is issued;

(b) winery means premises where wine is manufactured and

includes every place therein where wine is stored or wherefrom it is

issued;

(29) manufacture includes any process,

(a) incidental or ancillary to the completion of a manufactured

liquor; or

(b) whether natural or artificial, by which any liquor is produced

or prepared and also re-distillation and every process for the

rectification, reduction, flavouring, blending or colouring of liquor; or

(c) which, in relation to liquor, involves packing or repacking in a

bottle or unit package, or labelling or re-labelling of bottles or unit

package, including the declaration or alteration of maximum retail price

on it, or adoption of any other treatment on the liquor for sale to

consumers:

Provided that labelling of bottles or unit packages, imported into India

or into the Union territory of Lakshadweep, to comply with statutory

requirements, shall not be construed as manufacture;

(30) manufacturer means any person who manufactures Indian liquor

and includes a manufacturer of alcohol subject to excise duty under the Central

Excise Act, 1944;

(31) maximum retail price means the maximum price at which the

liquor may be sold to the ultimate consumer and shall include all taxes, freight,

transport charges, commission or trade margin payable to dealers, including

charges towards marketing, delivery, packing, forwarding and the like, as the

case may be;

(32) molasses means heavy dark coloured viscose liquid produced

from residual syrup, drained away in the final stage of the manufacture of gur

or sugar including khandasari sugar from sugarcane or gur, when liquid as

such or in any form or admixture containing sugar which can be fermented;

(33) notification means a notification published in the Official Gazette

be construed accordingly;

(34) permit means an authorisation granted under this Regulation and

the rules made thereunder;

(35) police station means the police station having jurisdiction over

the place or any other place, which the Administrator may, by notification,

declare to be a police station for the purposes of this Regulation;

(36) prescribed means prescribed by rules made by the Administrator

under this Regulation;

(37) special duty means a tax on the import of any excisable article,

being an article on which countervailing duty as is mentioned in entry 51 of

List II in the Seventh Schedule to the Constitution, is not imposable on the

ground merely that such article is not being manufactured or produced in the

territory;

(38) spirit means any liquor containing alcohol obtained by

distillation, whether denatured or not;

(39) still means an apparatus for distillation or manufacture of spirits

and includes any part thereof;

(40) transport means to move from one place to another within the

Union territory of Lakshadweep;

(41 territory of Lakshadweep;

(42) warehouse means a place where storage of liquor is permitted and

includes a relevant part of manufactory; and

(43) wine shall be the un-distilled alcoholic beverage produced by the

partial or complete alcoholic fermentation of the juice of fresh sound ripe

grapes, including grape juice concentrate, restored or un-restored pure

condensed grape must, and raisins:

1 of 1944.

Provided that a vintage wine is a wine made from grapes, of which at

least 85 per cent. were grown in a particular year and labelled as such and the

yield of the season of wine from a vineyard is a vintage wine.

CHAPTER II

ESTABLISHMENT AND CONTROL

3. The Administrator may, by notification, appoint or designate an officer as

the Excise Commissioner who shall be the chief controlling authority for

administration of this Regulation in the Union territory.

4. The Excise Commissioner shall exercise and perform the following powers

and functions, namely:

(a) to regulate, control and monitor the manufacture, possession, import,

export, transport, sale, purchase and consumption of liquor;

(b) to curb illegal trade in liquor and illicit distillation;

(c) to protect excise revenues of the Union territory and ensure prompt

recovery;

(d) to submit returns and information as required by this Regulation or

the rules made thereunder, upon all matters concerning excise;

(e) to ensure social well-being through education for responsible

drinking;

(f) to take adequate steps for imparting training to the excise staff in

preventive and detective work;

(g) to coordinate in matters covered under this Regulation with other

authorities;

(h) to introduce e-governance in various aspects of excise administration

and to maintain the national network information on manufacture, possession,

transport, sale, import or export of liquor.

Explanation. –

information and communication technology to promote efficient and

cost-effective services to the public;

(i) to submit to the Administrator an annual report on the administration

of this Regulation in such form as may be prescribed; and

(j) to perform such other functions and to exercise such other powers as

may, from time to time, be entrusted or delegated to him by the Administrator.

5. The Administrator may appoint or designate such number of Deputy

Commissioners, District Excise Officers and such other officers and staff as he may

deem fit for the purpose of performing the functions under this Regulation.

6. (1) Subject to the provisions of sub-section (1) of section 12, the

Administrator may issue licence or permit to any Government Corporation, or

Government company, or Government agency, or any autonomous body owned or

controlled by the Government, for the purposes of import and retail vending of

liquor in the Union territory.

(2) Save as otherwise provided in sub-section (1), the Deputy Commissioner

shall be the licensing authority who shall exercise all powers and functions under

this Regulation, subject to the general control and supervision of the Excise

Commissioner.

(3) The Deputy Commissioner shall, within the limits of his jurisdiction,

exercise such other powers and perform such duties and functions as are assigned

by or under the provisions of this Regulation subject to such control as the

Administrator or the Excise Commissioner may from time to time, direct.

(4) The District Excise Officer and other subordinate officers shall assist the

Deputy Commissioner in exercising his functions.

7. (1) The Administrator may, by order, delegate his powers to the Excise

Commissioner, subject to such limitations and conditions as may be specified in

such order.

(2) The Excise Commissioner or the Deputy Commissioner may, by order,

delegate their powers under this Regulation to any subordinate officer, subject to

such limitations and conditions as may be specified in such order.

(3) The Administrator or Excise Commissioner or the Deputy Commissioner,

as the case may be, may, by order, withdraw from any officer or person, any or all

the powers delegated to subordinate officers under this section.

8. The Administrator may, by notification, invest the power with any officer

of the Union territory, not being an Excise Officer, to perform all or any of the

powers or functions of any Excise Officer under this Regulation.

9. The Excise Commissioner may grant such reward to such officers and

employees under this Regulation and also to such informers for such work, subject

to such terms and conditions, as may be prescribed.

CHAPTER III

LICENCE AND PERMIT FOR MANUFACTURE, POSSESSION, SALE, ETC., OF LIQUOR

10. (1) No person shall construct or establish any manufactory or warehouse

or bottle, or possess, sell, collect, transport, transit, import, export or purchase any

liquor, or use, keep or have in his possession any still, utensil, implement, apparatus,

label, cork, capsule or seal, for manufacture of any liquor except under the authority

and in accordance with the terms and conditions of a letter of intent, licence or

permit granted under this Regulation or the rules made thereunder:

Provided that possession of labels, corks or capsules by its printer or

manufacturer, as the case may be, shall not amount to illegal possession constituting

an offence if the label, cork or capsule is printed or manufactured under the authority

from the holder of the licence to manufacture liquor under this Regulation.

(2) No person shall engage in the manufacture of alcohol exclusively for

industrial use unless he is registered with the Excise Commissioner in such manner

as may be prescribed.

11. Every letter of intent, licence or permit under this Regulation shall be

granted on payment of such fees, for such period, and subject to such terms and

conditions and in such form and shall contain such particulars, as may be prescribed.

12. (1) While considering an application for grant of a licence or permit, the

authorised officer shall ensure that the applicant

(a) is a citizen of India;

(b) is above eighteen years of age;

(c) is not a defaulter, or blacklisted, or debarred from holding an excise

licence;

(d) submits an affidavit as a proof for the following, namely:

(i) that he possesses or has an arrangement for taking on rent a

suitable premises for conducting the business and the said premises is

located more than fifty meters away from any medical institution,

educational institution, religious institution, women hostel, orphanage,

hospital, primary health centre or community health centre;

(ii) that the premises have not been constructed in violation of any

law for the time being in force;

(iii) that he possesses a good moral character and has no criminal

background nor has been convicted of any offence punishable under this

Regulation or any other law for the time being in force;

(iv) that he shall not employ any salesman or worker or

representative who has criminal background or suffers from any

infectious or contagious diseases or is below eighteen years of age;

(v) that he does not owe any public dues or dues to the

Administration;

(vi) that he is solvent and has the necessary funds or has made

arrangements for the necessary funds, for conducting the business; and

(vii) that the details of funds for conducting the business shall be

made available to the authorised officer, if so required.

(2) The licence or permit shall be liable for cancellation if any statement made

in the affidavit or any document produced with the application is found to be false

or forged.

13. Subject to such conditions as may be prescribed, the authority granting a

licence under this Regulation may require the licensee to

(a) give security for the observance of the terms of his licence; and

(b) execute a counterpart agreement in conformity with the tenure of his

licence.

14. (1) No licence or permit granted under this Regulation shall be deemed to

be invalid by reason merely of any technical defect, irregularity or omission in the

licence or permit, or in any proceeding conducted prior to grant thereof.

(2) The decision of the licensing authority, on the technical defect, irregularity

or omission shall be conclusive and binding.

15. (1) Whenever the authority which granted a licence or permit under this

Regulation considers that such licence or permit should be withdrawn for any

reason, it may do so, on expiry of a period of twentyto do so forthwith, after giving a reasonable opportunity of being heard and

assigning the reasons therefor in writing.

(2) If any licence or permit is withdrawn, the licensee or the permit holder shall

be paid such sum, by way of compensation, as the authority who granted licence or

permit may direct and refund any fee paid in advance or deposit made by the licensee

in respect thereof, after deducting the amount recoverable by the Government.

16. (1) Subject to such restrictions, as may be prescribed, the authority who

granted licence or permit under this Regulation may, after giving reasonable

opportunity of being heard, suspend or cancel the licence or permit, in the following

circumstances, namely:

(a) if the licence or permit is transferred or sublet by the holder thereof

without the permission of the said authority; or

(b) if any excise revenue payable by the holder thereof is not duly paid; or

(c) in the event of any breach of the terms and conditions of such licence

or permit by the holder or by his employee or agent; or

(d) if the holder of the licence or permit, or the agent or employee of

such holder, is convicted of an offence punishable under this Regulation or

under any other law for the time being in force, relevant to and connected with

excise matters or relating to excise revenue or of any cognizable and

non-bailable offence; or

(e) if the purpose for which the licence or permit was granted ceases to

exist; or

(f) if the licence or permit has been obtained through misrepresentation

or fraud.

(2) When a licence or permit held by such person is cancelled under

sub-section (1), the authority referred to therein may cancel any other licence or

permit granted to such person under this Regulation or under any other law relating

to excise revenue.

(3) In the case of cancellation or suspension of licence or permit under

sub-section (1), the fee payable for the balance of the period for which any licence

or permit shall have been valid but for such cancellation or suspension, may be

recovered from the licensee who held the licence before such cancellation or

suspension as excise revenue.

(4) The holder of a licence or permit shall not be entitled to any compensation

for the cancellation or suspension thereof nor shall be entitled to refund of any fee

paid or deposit made, if any, in respect thereof.

17. No person, to whom a licence or permit has been granted, shall be entitled

to claim right of any renewal thereof, and no claim shall lie for damages or otherwise

in consequence of any refusal to renew a licence or permit on the expiry of the period

for which the same remains in force.

18. No holder of a licence or permit granted under this Regulation shall

surrender his licence

writing, given by him to the Deputy Commissioner, of his intention to surrender the

same on payment of the fee payable for such licence or permit for the whole period

for which it shall have been valid but for the surrender:

Provided that if the Deputy Commissioner is satisfied that there are sufficient

reasons for surrendering the licence or permit, he may remit to the holder thereof

the sum so payable or any portion thereof, on surrender.

19. The licence or permit granted under this Regulation shall not be

transferable except with the prior approval of the Excise Commissioner or any

officer authorised by him in this behalf, subject to such terms and conditions, as may

be prescribed.

20. Subject to the provisions of this Regulation and subject to such terms and

conditions, as may be prescribed, the Excise Commissioner may grant to any person,

a licence or lease, or both, either jointly or severally, for the exclusive privilege or

for manufacture, supplying by wholesale or sale by retail, or both, any liquor within

any local area.

21. No liquor shall be removed from any manufactory, warehouse or other

place of storage established under this Regulation, unless duty and fee payable have

been paid or a bond, as may be prescribed, has been executed for the payment

thereof.

22. No person, or licensed vendor, or his employee or agent, shall sell or

deliver any liquor to any person under the age of twenty-one years whether for

consumption by self or of others.

23. No licensee shall employ or permit to be employed in his premises any

person under the age of eighteen years or who is suffering from any contagious

disease.

24. The District Magistrate or any other officer authorised by him may, by a

notice in writing to the licensee, require that any shop in which any liquor is sold

shall be closed at such times or for such period as he may think necessary, for

preservation of public peace:

Provided that the closure days in the licensing year shall not exceed seven days

in all or more than three days continuously at any given time:

Provided further that if the Excise Commissioner or an officer authorised by

him in this behalf is of the opinion that any particular shop or all shops in any

particular area shall be closed for a period exceeding seven days in a licensing year,

or more than three days continuously at any given time, he may, with the prior

sanction of the Administrator, permit to do so.

25. The excise revenue shall be levied and recovered under the following

heads, namely:

(a) duty;

(b) licence fee;

(c) label registration fee; and

(d) import or export fee.

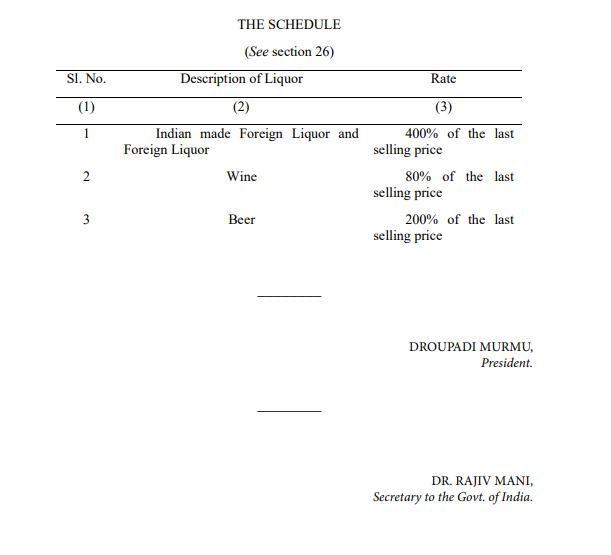

26. (1) There shall be levied and collected in the manner provided by this

Regulation and the rules made thereunder, at such rates, not exceeding the rates set

forth in the Schedule, as the Administrator may, by notification, specify, a duty of

excise or a countervailing duty or a special duty, as the case may be, on all liquor of

the descriptions notified by the Administrator from time to time, being

manufactured or produced in, or imported into, the Union territory, from the person

so manufacturing or producing or importing:

Provided that no such duty shall be levied on toddy when used for the

manufacture of jaggery, vinegar, yeast or neera, or when drunk as such.

Explanation. For the purposes of this section, it is hereby declared that in

any notification issued under this section, it shall not be necessary to specify

separately the rate of countervailing duty or special duty and, unless otherwise

provided in such notification expressly, any rate specified in such notification as the

rate of excise duty in respect of any description of liquor shall be deemed to be also

the rate of countervailing duty or a special duty, as the case may be, in respect of

such description of liquor.

(2) There shall be levied and collected a fee for issue of licence or permit

subject to such terms and conditions, as may be prescribed.

(3) There shall be levied and collected the import, export or transport duties

assessed in such manner as may be prescribed.

27. (1) All duties, fees, taxes, fines payable to the Government under this

Regulation may be recovered from the persons liable to pay the same, or from his

surety, or his agent, as if they were arrears of land revenue.

(2) In the event of default by any person to whom a licence or permit has been

granted under this Regulation, his manufactory, warehouse, shop or premises and

all fittings, apparatus, stocks of liquor or materials for the manufacture of the same,

held therein, shall be liable to be attached towards any claim for excise revenue

or in respect of any loss incurred by the Government through such default and be

sold to satisfy such claim, which shall be a first charge upon the proceeds of such

sale.

(3) Where the duty due is not levied or not paid or short-levied or short-paid

or erroneously refunded,

(a) the District Excise Officer may, within a period of three years from

the relevant date, serve notice on the person chargeable with the duty of excise,

which has not been levied or paid, or which has been short-levied or

short-paid, or to whom the refund has erroneously been made, requiring him

to show cause why he should not pay the amount specified in the notice:

Provided that where the service of the notice is stayed by an order of a

Court, the period of such stay shall be excluded in computing such period of

three years.

(i) in cases in which duty of excise has not been paid or has been

short-levied or short-paid, the date on which the duty is to be paid under

this Regulation or the rules made thereunder;

(ii) in a case where duty of excise is provisionally assessed under

this Regulation or the rules made thereunder, the date of adjustment of

duty after the final assessment thereof; and

(iii) in a case where the duty of excise has been erroneously

refunded, the date of such refund; and

(b) the District Excise Officer shall, after considering the representation,

if any, made by the person on whom notice is served under clause (a),

determine the amount of duty of excise due from such person (not being in

excess of the amount specified in the notice) and thereupon such person shall

pay the amount so determined.

28. If the duty of excise payable by a person under this Regulation or the rules

made thereunder is not paid within time, he shall be liable to pay on the sum due, a

simple interest at the rate of twelve per cent. per annum from the day next following

the day on which such payment became due:

Provided that where the duty determined to be payable is reduced or increased

by the Appellate Authority or the Court, the interest shall be payable on such

reduced or increased amount of duty, as the case may be.

29. Notwithstanding anything contained in this Regulation, the Excise

Commissioner may, on an application made in this behalf by a person, with the

approval of the Administrator and after recording his reason for so doing, reduce or

waive the amount of any interest payable by him under this Regulation, if he is

satisfied that

(a) to do otherwise would cause genuine hardship to the person having

regard to the circumstances of the case; and

(b) the person has cooperated in any proceeding for the recovery of any

amount due from him.

30. Notwithstanding that a writ petition has been preferred or a suit or other

proceeding has been instituted in any Court, or any appeal has been filed before any

Court or Tribunal or before the Excise Commissioner, or a revision has been filed

before the Administrator, any sum due to the Government under this Regulation as

a result of demand or order made or passed by any officer or authority empowered

in this behalf by or under this Regulation, shall be payable in accordance with such

demand or order unless and until such payment has been stayed by such Court or

Tribunal or Excise Commissioner or Administrator.

31. Every licensee shall maintain such accounts and submit to the concerned

officers such returns in such forms, containing such particulars relating to stock,

apparatus, excise duty or fee payable or paid, and such other information at such

interval, as may be prescribed.

CHAPTER V

OFFENCES AND PENALTIES

32. Whoever manufactures, imports, exports, transports or removes any

liquor, in contravention of any of the provisions of this Regulation or of any rule

made, or notification or order issued, thereunder, or of any condition of licence or

permit granted or issued thereunder, shall be punishable,

(a) where the liquor involved in the offence is less than such value, as

may be prescribed, with imprisonment for a term which shall not be less than

one year, but which may extend to five years, and with fine which shall not be

less than fifty thousand rupees or five times of the value of liquor, whichever

is higher;

(b) where the liquor involved in the offence exceeds such value, as may

be prescribed, with imprisonment for a term which may extend to seven years,

and with fine, which may extend to one lakh rupees or five times of the value

of liquor, whichever is higher.

33. Whoever constructs or works in any manufactory or warehouse, in

contravention of any of the provisions of this Regulation, or of any rule made, or

notification or order issued, thereunder, or of any condition of licence or permit

granted or issued thereunder, shall be punishable with imprisonment for a term

which may extend to three years, or with fine which may extend to fifty thousand

rupees, or with both.

34. Whoever bottles any liquor for the purposes of sale, in contravention of

any of the provisions of this Regulation, or of any rule made, or notification or order

issued, thereunder, or of any condition of licence or permit granted or issued

thereunder, shall be punishable with imprisonment for a term which may extend to

one year, and with fine which may extend to one lakh rupees or five times of the

value of liquor, whichever is higher.

35. Whoever uses, keeps or possesses any materials, still, utensils, implements

or apparatus whatsoever for the purposes of manufacturing any liquor, in

contravention of any provisions of this Regulation, or of any rule made, or notification

or order issued, thereunder, or of any condition of licence or permit granted or issued

thereunder, shall be punishable with imprisonment for a term which may extend to six

months, or with fine which may extend to twenty thousand rupees, or with both.

36. Whoever possesses any material or film, either with or without Union

territory logo or wrapper or any other thing in which liquor can be packed, or any

apparatus or implement or machine for the purpose of packing any liquor, in

contravention of any of the provisions of this Regulation, or of any rule made, or

notification or order issued, thereunder, or of any condition of licence or permit

granted or issued thereunder, shall be punishable with imprisonment for a term

which may extend to three months, or with fine which may extend to fifty thousand

37. Whoever sells, transports, possesses or buys any liquor beyond such

quantity, as may be prescribed, in contravention of any of the provisions of this

Regulation, or of any rule made, or notification or order issued, thereunder, or of

any condition of licence or permit granted or issued thereunder, shall be punishable

with imprisonment for a term which may extend to three months, and with fine

which may extend to one lakh rupees or five times of the value of liquor, whichever

is higher.

38. If any offence referred to in sections 32, 33, 34, 35, 36 and 37 is committed

by a person not holding valid licence or permit under this Regulation, he shall be

liable to twice the fine provided for such offence.

39. Whoever renders or attempts to render fit for human consumption any

spirit which has been denatured, or has in his possession any spirit in respect of

which he knows or has reason to believe that any such attempt has been made, shall

be punishable with imprisonment for a term which shall not be less than two years,

but which may extend to three years, and with fine which may extend to two lakh

rupees or five times of the value of liquor, whichever is higher.

Explanation. For the purposes of this section, denatured spirit means the

spirit with an added denaturant to render it effectively and permanently unfit for

human consumption.

40. Whoever mixes or permits to be mixed with any liquor sold or

manufactured or possessed by him, any noxious drug or any foreign ingredient,

likely to cause disability or grievous hurt or death to human being, shall be

punished,

(a) if as a result of such an act, death is caused to any person, with

imprisonment for a term which shall not be less than ten years, but which may

extend to imprisonment for life and shall also be liable to fine, which may

extend to ten lakh rupees; or

(b) if as a result of such an act, disability or grievous hurt is caused to

any person, with imprisonment for a term which shall not be less than seven

years but which may extend to ten years, and with fine which may extend to

five lakh rupees; or

(c) if as a result of such an act, any other consequential injury is caused

to any person, with imprisonment for a term which may extend to one year

and shall also be liable to fine which may extend to two lakh fifty thousand

rupees; or

(d) if as a result of such an act, no injury is caused to any person, with

imprisonment which may extend to six months and with fine which may

extend to one lakh rupees or five times the value of liquor, whichever is higher.

Explanation.

shall have the same meaning as assigned to it in section 116 of the Bharatiya Nyaya

Sanhita, 2023.

41. (1) Notwithstanding anything contained in the Bharatiya Nagarik Suraksha

Sanhita, 2023, the Court, when passing an order under this Regulation may, if it is

satisfied that death or injury has been caused to any person due to consumption of

liquor sold in any place, order the manufacturer or seller, whether or not he is

convicted of an offence, to pay, by way of compensation, an amount not less than

three lakh rupees to the legal representatives of each deceased, or two lakh rupees

to the person to whom grievous injury has been caused, or twenty thousand rupees

to the person for any other consequential injury:

Provided that where such liquor is sold in a licensed shop, the liability to pay

the compensation under this section shall be on the licensee.

45 of 2023.

46 of 2023.

(2) Any person aggrieved by an order under sub-section (1) may, within a

period of thirty days from the date of order, prefer an appeal to the High Court:

Provided that no appeal shall be filed by the accused unless the amount

ordered to be paid under sub-section (1) is deposited by him in the Court:

Provided further that the High Court may entertain an appeal after the expiry

of the said period of thirty days if it is satisfied that the appellant was prevented by

sufficient cause from preferring the appeal in time.

42. Whoever sells, or keeps, or exposes for sale, as foreign liquor which he

knows or believes it to be Indian liquor, shall be punishable with imprisonment

which may extend to six months, and with fine which may extend to one lakh rupees

or five times the value of liquor, whichever is higher.

43. Whoever has in his possession, any liquor, knowing that it shall be liable

to penalty for having unlawfully imported, transported or manufactured, or

knowingly avoids payment of duty for possession of liquor, shall be punishable with

imprisonment for a term which may extend to six months and with fine which may

extend to one lakh rupees, or five times the value of liquor, whichever is higher.

44. (1) If a chemist, druggist, apothecary or keeper of a dispensary, allows any

liquor which has not been bonafidely medicated for medicinal purposes to be

consumed on his business premises by any person, he shall be punishable with fine

which may extend to five thousand rupees.

(2) If any person consumes liquor on a business premises referred to in

sub-section (1), he shall be punishable with fine which may extend to two thousand rupees.

45. Whoever consumes liquor in a public place, in contravention of the any of

the provisions of this Regulation, or of any rule made, or notification or order issued,

thereunder, shall be punishable with fine which may extend to five thousand rupees.

46. Whoever consumes liquor in public place and creates nuisance, in

contravention of the any of the provisions of this Regulation, or of any rule,

notification or order made thereunder, shall be punishable with imprisonment for a

term which may extend to three months, and with fine which may extend to ten

thousand rupees.

47. Whoever permits drunkenness or allows assembly of anti-social elements,

on the premises of liquor establishments in contravention of the any of the

provisions of this Regulation, or of any rule made, or notification or order issued,

thereunder, shall be punishable with imprisonment for a term which may extend to

six months, and with fine which may extend to fifty thousand rupees.

48. Whoever prints, publishes or gives an advertisement in any media soliciting

use of any liquor, shall be punishable with imprisonment for a term which may extend

to six months, or with fine which may extend to ten lakh rupees, or with both:

Provided that this section shall not apply to catalogue or price list or

advertisement generally or specially approved by the Excise Officer for the purposes

of display at the points of sale for consumer information and education.

49. Any person who unlawfully releases or abets escape of any person arrested

under this Regulation, or abets the commission of offence under this Regulation, or

engages himself in a criminal conspiracy for contravention of the any of the provisions

of this Regulation, shall be punishable with imprisonment for a term which may

extend to one year, and with fine which may extend to fifty thousand rupees.

50. If any licence holder or any person acting in his behalf, sells or delivers

any liquor to any person apparently under the age of twenty-one years or employs

any person under the age of eighteen years, he shall be punishable with

imprisonment for a term which may extend to three months, or with fine which may

extend to fifty thousand rupees, or with both.

51. Notwithstanding anything contained in the Bharatiya Nyaya

Sanhita, 2023, any person who assaults or threatens to assault or obstructs or

attempts to obstruct any Excise Officer in the discharge of his official duties, shall

be punishable with imprisonment for a term which may extend to two years, and

with fine which may extend to one lakh rupees.

52. The holder of a licence or permit granted or issued under this Regulation,

shall be liable for any offence committed by his employee or his agent, unless he

proves that due and reasonable precautions were exercised by him to prevent

commission of such offence.

53. (1) Where any liquor has been manufactured or sold or is possessed by

any person on account of any other person and such other person knows, or has

reason to believe, that such manufacture or sale was or that such possession is, on

his account, such liquor shall, for the purposes of this Regulation, be deemed to

have been manufactured, sold or to be in the possession of such other person.

(2) Nothing in sub-section (1) shall absolve any person who manufactures,

sells or has possession of any liquor on account of another person, from liability to

any punishment under this Regulation for unlawful manufacture, sale or

possession of such liquor.

54. Whoever, being the holder of a licence or permit granted or issued under

this Regulation, or being in the employment of such holder and acting on his

behalf, fails to produce such licence or permit on demand by any Excise Officer or

any other officer duly empowered to make such demand, shall be punishable with

fine which may extend to fifty thousand rupees.

55. Whoever, being the holder of a licence or permit granted or issued under

this Regulation, or being in the employment of such holder and acting on his

behalf, wilfully does or omits to do anything in breach of any of the conditions of

his licence or permit otherwise than provided in this Regulation, or fails to print

the maximum retail price on the label or tampers with it, shall be punishable with

imprisonment for a term which may extend to six months, and with fine which

may extend to one lakh rupees.

56. Whoever, being the holder of a licence or permit granted or issued under

this Regulation, or being in the employment of such holder and acting on his

behalf, fails to submit returns, shall be punishable with fine which may extend to

one lakh rupees, and ten thousand rupees per day for any subsequent delay.

57. (1) If any person fails to pay any duty or fee under this Regulation, he

shall be punishable with imprisonment for a term which may extend to one year

and also with fine which may extend to one lakh rupees.

(2) Without prejudice to sub-section (1), the person referred to therein shall also be

liable to pay interest on delayed payment and damages at such rates as may be imposed.

58. Whoever, in any declaration or affidavit or periodic return made to an

Excise Officer, makes a statement which is false or found to be false, after due

verification or which he believes to be false or does not believe it to be true,

touching any point material to the object for which the statement is made or used,

shall be punishable with imprisonment for a term which may extend to one year,

and with fine which may extend to fifty thousand rupees.

59. Whoever, being a licensee and having the control or use of any house,

room, enclosure, space, animal or conveyance, knowingly permits it to be used for

commission by any other person of an offence punishable under any of the

provisions of this Regulation, shall be punishable in the same manner as if he had

himself committed the said offence.

60. Whoever attempts to commit any offence punishable under this

Regulation, shall be liable for half the punishment provided for such offence

under this Regulation.

61. Any Excise Officer or other person, who with vexatious intention and

without reasonable ground for suspicion,

(a) enters or searches or causes to be entered or searched any closed place

under the guise of exercising any power conferred by this Regulation; or

(b) seizes the movable property of any person on the pretext of

seizing or searching for any article liable to confiscation under this

Regulation; or

(c) searches, detains or arrests any person; or

(d) exceeds his lawful powers under this Regulation,

shall be punishable with fine which may extend to ten thousand rupees.

62. Any Excise Officer who, without lawful excuse, refuses to perform, or

withdraws himself from the duties of his office, unless expressly allowed to do

so in writing by the Excise Commissioner, or unless he has given to his superior

or who shall be

guilty of cowardice, shall be punishable with imprisonment for a term which

may extend to three months, or with fine which may extend to ten thousand

rupees, or with both.

63. Whoever, does any act in contravention of any of the provisions of this

Regulation, or any rule made, or notification or order issued, thereunder and

punishment for such contravention has not been provided under this Regulation,

shall be punishable with imprisonment for a term which may extend to six

months, and with fine which may extend to ten thousand rupees or five times the

value of the liquor, whichever is higher.

64. (1) In a prosecution under section 32, 33, 34, 35, 36 or section 37, it

shall be presumed, until the contrary is proved, that the accused person has

committed the offence punishable under that section in respect of any liquor,

still, utensil, implement or apparatus, for the possession of which he is unable to

account satisfactorily.

(2) Where any animal, vessel, cart or other vehicle is used in the

commission of any offence under this Regulation, and is liable to confiscation,

the owner thereof shall be deemed to be guilty of such offence and such owner

shall be liable to be proceeded against and punished accordingly unless he

satisfies the Court that he had exercised due care in the prevention of the

commission of such an offence.

65. If any person, after having been previously convicted of an offence

punishable under this Regulation, subsequently commits and is convicted for the

same offence, he shall be liable to twice the punishment provided for the first

conviction subject to the maximum punishment provided for such offence and

with twice the fine amount provided under the first conviction, or with both.

66. Where at any time during the trial of any offence under this Regulation

alleged to have been committed by any person, not being the manufacturer,

distributor or dealer of any liquor, the Court is satisfied, on the evidence

adduced before it, that such manufacturer, distributor or dealer is also concerned

with that offence, then, the Court may, notwithstanding anything contained in

sub-section (3) of section 358 of the Bharatiya Nagarik Suraksha Sanhita, 2023,

proceed against him under the respective provisions of this Chapter.

67. (1) If the person committing an offence under this Regulation is a

company, the company and every person who at the time the offence is committed

was in-charge of, and responsible to, the company for the conduct of its business

at the time of the commission of the offence, shall be deemed to be guilty of such

offence, and shall be liable to be proceeded against and punished accordingly:

Provided that where a company has different establishments or branch, the

concerned Chief Executive and the person in-charge of such establishment, branch

or unit, nominated by the company as responsible for the conduct of business,

shall be liable for that offence in respect of such establishment, branch or unit:

Provided further that nothing in this sub-section shall render any such person

liable to any punishment if he proves that the offence was committed without his

knowledge or that he exercised all due diligence to prevent the commission of

such offence.

(2) Notwithstanding anything contained in sub-section (1), where an offence

under this Regulation has been committed by a company and it is proved that the

offence has been committed with the consent or connivance of, or that the commission

of the offence is attributable to any neglect on the part of any director, manager,

secretary or other officer of the company, such director, manager, secretary or other

officer shall be liable to be proceeded against and punished accordingly.

68. (1) The authorised Excise Officer shall, after investigation of any offence

committed under this Regulation, send his report to the Deputy Commissioner.

(2) The Deputy Commissioner shall, after scrutiny of the investigation report

sent to him under sub-section (1), decide within such period as may be prescribed,

and on the basis of the gravity of offence, that the matter be referred to

(a) a Court of ordinary jurisdiction in case of offences punishable with

imprisonment for a term which may extend to three years; or

(b) a special Court in case of offences punishable with imprisonment

for a term exceeding three years, where such Special Court is established,

and in case no Special Court is established, such cases shall be tried by a

Court of ordinary jurisdiction.

(3) The Deputy Commissioner shall communicate his decision to the

concerned Excise Officer, who shall launch prosecution before a Court of ordinary

jurisdiction or a Special Court, as the case may be.

69. (1) Any other contravention under this Regulation shall be adjudicated

by an Adjudicating Officer.

(2) The Administrator shall, by notification, appoint an officer not below the

rank of an Additional District Magistrate of the district where the alleged

contravention occurred, to be the Adjudicating Officer for adjudication in such

manner as may be prescribed.

(3) The Adjudicating Officer shall, after giving the person a reasonable

opportunity for making representation in the matter, and if, on such inquiry, he is

satisfied that the person has contravened the any of the provisions of this Regulation

or any rule made, or notification or order issued, thereunder, impose such penalty as

he thinks fit in accordance with the provisions relating to that contravention.

(4) The Adjudicating Officer shall have the powers of a Civil Court and all

the proceeding before him shall be deemed to be

(a) a judicial proceeding within the meaning of sections 229 and 267 of

the Bharatiya Nyaya Sanhita, 2023;

(b) a Court for the purposes of sections 384 and 385 of the Bharatiya

Nagarik Suraksha Sanhita, 2023.

(5) While adjudicating the quantum of penalty under this Chapter, the

Adjudicating Officer shall have due regard to the provisions of section 71.

70. (1) Notwithstanding anything contained in the Bharatiya Nagarik

Suraksha Sanhita, 2023, the offences punishable under sections 44, 45, 54, 56 and

61 may either before or after the institution of any proceeding, be compoundable

under this Regulation.

(2) Any person who is reasonably suspected of having committed an offence

specified under sub-section (1) may apply to the District Excise Officer for

compounding of the offence.

(3) On receipt of an application under sub-section (2), the District Excise

Officer, having regard to the circumstances of the case, may at his discretion order

for compounding of the offence on payment of such sum of money by way of

compounding fee or compensation for the offence, in accordance with such

guidelines as may be prescribed.

(4) On payment by the person such sum of money specified under

sub-section (3), no proceeding shall be instituted or continued against such person

in any Criminal Court:

Provided that the sum of money fixed as compounding fee or compensation

by the District Excise Officer under this section shall not be less than five times

but not more than ten times the duty involved or the value of liquor, apparatus,

vehicle and other material, whichever is higher:

Provided further that where liquor, apparatus, vehicle or other material is

seized, the same shall not be released but shall be disposed of in such manner as

may be prescribed.

(5) Where the composition of any offence is made after the institution of any

prosecution, such composition shall be brought by the District Excise Officer in

writing, to the notice of the Court in which the prosecution is pending and on such

notice of the composition of the offence being given, the person in relation to

whom the offence is so compounded shall be discharged.

71. While adjudging the quantum of fine or penalty under this Chapter, the

Court or the Adjudicating Officer, as the case may be, shall have due regard to the

following, namely:

(a) the amount of gain or unfair advantage, wherever quantifiable,

made as a result of the contravention;

(b) the amount of loss caused or likely to cause to the Government or

any person as a result of the contravention;

(c) the repetitive nature of the contravention;

(d) whether the contravention is without his knowledge; and

(e) any other relevant factor.

72. Whenever an offence punishable under this Regulation has been

committed, the following things shall be liable to confiscation, namely:

(a) any liquor, material, still, utensil, implement apparatus in respect of

or by means of which such offence has been committed;

(b) any liquor unlawfully imported, transported, manufactured, sold or

brought along with, or in addition to any liquor, liable to confiscation under

clause (a);

(c) any receptacle, package, or covering in which anything liable to

confiscation under clause (a) or clause (b) is found, and the other contents, if

any, of such receptacle package or covering; and

(d) any animal, vehicle, vessel, or other conveyance used for carrying

liquor.

73. (1) Notwithstanding anything contained in this Regulation or any other

law for the time being in force, where anything liable for confiscation under

section 72 is seized or detained under the provisions of this Regulation, the officer

seizing or detaining such property shall, without any unreasonable delay, produce

the said seized property before the Deputy Commissioner.

(2) On production of the property seized under sub-section (1), the Deputy

Commissioner, if satisfied that an offence has been committed under this

Regulation, may, whether or not a prosecution is instituted for the commission of

such offence, order for confiscation of such property, or otherwise he may order

for its return to the rightful owner.

(3) While making an order of confiscation under sub-section (2), the Deputy

Commissioner may also order that such of the properties to which the order of

confiscation relates, which, in his opinion, cannot be preserved or are not fit for

human consumption, be destroyed.

(4) Whenever any confiscated article has to be destroyed under this section,

it shall be destroyed in the presence of the Excise Officer ordering the confiscation

or forfeiture, as the case may be, or in the presence of an Excise Officer not below

the rank of an Inspector.

(5) Where the Deputy Commissioner, after passing an order of confiscation

under sub-section (2), is of the opinion that it is expedient in the public interest so

to do, he may order the confiscated property or any part thereof to be sold by

public auction or dispose it of otherwise.

(6) The Deputy Commissioner shall submit a report of all particulars of

confiscation to the Excise Commissioner within a period of one month of such

confiscation.

(7) Any liquor, mahua flowers or molasses and any other property if

confiscated in a case compounded under section 70 or in respect of which an

offence has been committed and the offender is not known or cannot be found,

shall be disposed of in such manner as may be prescribed.

74. (1) The order of any confiscation under section 73 shall not prevent

imposition of any other punishment to which the person affected thereby is liable

under this Regulation.

(2) Notwithstanding anything contained in any other law for the time being

in force, the non-production of confiscated property before the trial Court due to

disposal of such property, shall not affect the proceeding under this Regulation:

Provided that the samples of liquor and the photographs of the confiscated

property may be preserved to meet the evidentiary requirements.

75. (1) Subject to the provisions of this Regulation, when any article, animal

or thing is duly confiscated either by order of Court or otherwise, such article,

animal or thing shall be made over to the Deputy Commissioner for disposal in

such manner and on payment of such fees, as may be prescribed.

(2) When an order for confiscation of any property has been passed under

section 73 and such order has become final in respect of the whole or any portion

of such property, such property or portion thereof, as the case may be, shall vest in

the Administrator, free from all encumbrances.

CHAPTER VI

DETECTION, INVESTIGATION AND TRIAL OF OFFENCES

76. The Excise Commissioner or any authorised Excise Officer may, by

order, require any person or any establishment deemed reasonably connected with

any unlawful handling of liquor, to furnish to him such information as may be

specified in that order.

77. (1) Whenever any liquor is manufactured, exported, imported or

transported, collected, possessed or sold, in contravention of any provisions of this

Regulation, the owner or occupier of the land or building or his agent, and every

officer of police and land revenue department, local bodies and block development

office shall, in the absence of reasonable excuse, be bound to give notice of the

fact to a Magistrate or to an officer of the Excise Department as soon as the fact

comes to their knowledge.

(2) Every Excise Officer shall be bound to give immediate information to his

immediate superior, of all breaches of any of the provisions of this Regulation,

which may come to his knowledge under sub-section (1) or otherwise.

78. (1) The authorised Excise Officer may search any place, or seize any

article, or arrest or detain any person, if there is a reasonable doubt that such place,

article or person is involved in commission of any offence under this Regulation:

Provided that no search shall be deemed to be irregular by reason only of the

fact that witness for the search is not inhabitant of the locality in which the place

searched is situated.

(2) Save as otherwise expressly provided in this Regulation, the provisions

of the Bharatiya Nagarik Suraksha Sanhita, 2023 relating to search, seizure, arrest,

detention, summons and investigation shall apply, as far as may be, to all actions

taken under this Regulation.

79. Every officer-in-charge of a police station shall take charge of and keep

in safe custody, pending the orders of a Magistrate or of the Deputy

Commissioner, all articles seized under this Regulation, which may be delivered to

him and shall allow any officer of the Excise Department who may accompany

such articles, to affix his seal to such articles and to take samples of and from them

and all samples so taken shall also be sealed with the seal of the officer-in-charge

of the police station.

Explanation. For the purposes of this section, officer-in-charge means

the Excise Officer authorised to supervise and control manufactory or warehouse.

80. All offences under this Regulation shall be cognizable and the provisions

of the Bharatiya Nagarik Suraksha Sanhita, 2023, shall apply to them.

81. The offences punishable under this Regulation with imprisonment of two

years and more, shall be non-bailable and the provisions of the Bharatiya Nagarik

Suraksha Sanhita, 2023, with respect to non-bailable offences, shall apply to those

82. Notwithstanding anything contained in the Bharatiya Nagarik Suraksha

Sanhita, 2023, the Magistrate shall have the power to try summarily in accordance

with the provisions contained in sections 285 to 288 of that Sanhita, all or any of

the offences which are punishable under this Regulation with imprisonment for a

term not exceeding six months, or with fine, or with both.

83. (1) Whenever any person is convicted of an offence punishable under

this Regulation and the Court convicting him is of the opinion that such person

habitually commits or attempts to commit, or abets the commission of such

offence and that it is necessary to require such person to execute a bond for

abstaining from the commission of any such offence, the Court may, at the time of

passing sentence on such person, order him to execute a bond for a sum

proportionate to his means, with or without sureties, for abstaining from the

commission of such offence during such period, not exceeding three years, as it

thinks fit to fix.

(2) The bond referred to in sub-section (1) shall be in such form in terms of

the provisions of the Bharatiya Nagarik Suraksha Sanhita, 2023 and shall, in so far

as they are applicable, apply to all matters connected with such bond as if it were a

bond to keep the peace ordered to be executed under section 125 of that Sanhita.

(3) If the conviction is set aside on appeal or otherwise, the bond so executed

under this section shall become void.

(4) An order under this section may also be made by an Appellate Court or

by the High Court when exercising its power of revision.

CHAPTER VII

APPEAL AND REVISION

84. (1) Any person aggrieved by any decision or order passed under this

Regulation by an Excise Officer, may appeal to the Deputy Commissioner.

(2) Any person aggrieved by any decision or order of the Deputy

Commissioner, may appeal to the Excise Commissioner.

(3) An appeal under this section shall be filed within a period of thirty days

from the date of receipt of such decision or order together with self-attested copy

thereof:

Provided that a further period of thirty days may be allowed, if the appellant

establishes that sufficient cause prevented him from filing the appeal within the

said period of thirty days.

85. (1) At the hearing of an appeal, an appellant may be allowed to go into

any ground not specified in the grounds of appeal or take additional evidence

where necessary, if it is established that such omission was not wilful or

unreasonable.

(2) The Appellate Authority may, after making such further inquiry as may

be necessary, pass such order, as he thinks fit, just and proper, confirming,

modifying or annulling the decision or order appealed against, as the case may be.

(3) The appeal shall be heard and decided within a period of six months from

the date on which such appeal is filed:

Provided that if an appeal is not decided within the period specified, the

relief prayed for in the appeal shall be deemed to have been granted.

86. (1) The order of the Appellate Authority disposing of the appeal shall be

in writing and shall state the points for determination, the decision thereon and the

reasons for the decision.

(2) The Appellate Authority shall communicate the order passed by him to

the appellant and the Excise Officer or Deputy Commissioner, as the case may be,

whose order formed the subject matter of appeal.

87. The Excise Commissioner may, at any time within six months from the

date of the order, with a view to rectifying any mistake apparent from the record,

amend any order passed by him and shall make such amendments if the mistake is

brought to his notice by any of the parties to the appeal:

Provided that an amendment which has the effect of enhancing an

assessment or reducing a refund or otherwise increasing the liability of the other

party, shall not be made under this section unless the Excise Commissioner has

given notice to the appellant of his intention so to do and has granted him an

opportunity of being heard.

88. (1) The Excise Commissioner may, on his own motion, call for the

record of any proceeding in which an officer subordinate to him has taken any

decision or passed an order under this Regulation, including those related to the

grant, issue or refusal to grant a licence, for the purpose of satisfying himself as to

the legality or propriety of any such decision or order and may make such inquiry

or cause such inquiry to be made and, subject to the provisions of this Chapter,

pass such order thereon as he thinks fit.

(2) No order, which is prejudicial to any person, shall be passed under this

section unless the person has been given an opportunity of being heard.

(3) The Excise Commissioner shall communicate the order passed by him

under sub-section (1) to such person and the Excise Officer or Deputy

Commissioner, whose order formed the subject matter of revision.

(4) No order under this section shall be passed by the Excise Commissioner

in respect of any issue, if an appeal against such issue is pending before the

Deputy Commissioner.

(5) No order under this section shall be passed after the expiry of a period of

six months from the date on which the order sought to be revised has been passed.

89. (1) Where in any appeal under this Chapter, the decision or order

appealed against relates to any duty or fee demanded or any penalty or fine levied

under this Regulation, the person desirous of appealing against such decision or

order shall, pending the appeal, deposit with the Excise Officer, the duty or fee as

demanded or the penalty or fine levied, if such amount exceeds one lakh rupees.

(2) Where in any particular case, the Appellate Authority is of the opinion that

the appellant has a prima facie case in his favour and deposit of duty demanded or

penalty levied would cause undue hardship to such person, the Appellate Authority

may dispense with such deposit and stay its recovery subject to such conditions as he

may deem fit to impose so as to safeguard the interest of revenue.

(3) Where an application is filed for dispensing with the deposit of duty or

fee demanded or penalty or fine levied under sub-section (2), the Appellate

Authority shall, where it is possible so to do, decide such application within a

period of thirty days from the date of its filing.

(4) Notwithstanding anything contained in sub-section (1), no recovery

action shall be initiated against the appellant until the application under

sub-section (3) has been decided by the Appellant Authority.

90. (1) Any Government Corporation or Government company or

Government agency or any autonomous body owned or controlled by the

Government referred to in sub-section (1) of section 6, is aggrieved by the order of

the Administrator may file an appeal to the High Court.

(2) An appeal shall lie to the High Court from an order passed in appeal by

the Excise Commissioner, if the High Court is satisfied that the case involves a

substantial question of law.

(3) The Government or the other party aggrieved by any order passed by the

Excise Commissioner may file an appeal to the High Court and such appeal under

this sub-section shall be

(a) filed within a period of sixty days from the date on which the order

appealed against is received by the Government or the other party;

(b) accompanied by a fee of ten per cent. of the amount involved or

two thousand rupees, whichever is higher, where such appeal is filed by the

other party;

(c) in the form of a memorandum of appeal precisely stating therein the

substantial question of law involved.

(4) Where the High Court is satisfied that a substantial question of law is

involved in any case, it shall formulate that question.

(5) The appeal shall be heard only on the question so formulated, and the

respondent shall, at the hearing of the appeal, be allowed to argue that the case

does not involve such question:

Provided that nothing in this sub-section shall be deemed to take away or

abridge the power of Court to hear, for reasons to be recorded in writing, the

appeal on any other substantial question of law not formulated by it, if it is

satisfied that the case involves such question of law.

(6) The High Court shall decide the question of law so formulated and

deliver such judgment thereon containing the grounds on which decision is

founded and may award such cost as it deems fit.

(7) The High Court may determine any issue which

(a) has not been determined by the Excise Commissioner;

(b) has been wrongly determined by the Excise Commissioner, by reason

of a decision of such question of law as is referred to in sub-section (2).

(8) An Appeal under this section shall be heard by a bench of not less than

two judges of the High Court, and shall be decided in accordance with the opinion

of such judges or of the majority, if any, of such judges.

(9) Where there is no such majority, the judges shall state the point of law

upon which they differ and the case shall, then, be heard upon that point only by

one or more of the other judges of High Court and such point shall be decided

according to the opinion of the majority of the judges who have heard the cases

including those who first heard it.

(10) Save as otherwise provided in this section, the provisions of the Code of

Civil Procedure, 1908, relating to the appeals to the High Court shall as far as may

be, apply in cases of appeal under this section.

91. Notwithstanding that an appeal has been preferred to the High Court,

sums due to the Government as a result of an order passed by the Excise

Commissioner shall be payable in accordance with the order so passed:

Provided that nothing contained in this section or Chapter shall affect the

inherent powers of the High Court for granting stay on the recovery of such

amount.

CHAPTER VIII

MISCELLANEOUS

92. Every person, who manufactures or sells any liquor under a licence

granted under this Regulation, shall

(a) supply himself with such measures, weights and instruments as the

Excise Commissioner may specify in this behalf, and keep the same in good

condition; and

(b) on the requisition of any Excise Officer, at any time to measure,

weight or test any liquor in his possession in such manner as the said Excise

Officer may require.

93. The Administrator may, by notification, declare as to what shall be

deemed to be liquor for the purposes of this Regulation or the rules made

thereunder.

94. The Administrator may issue such order and take such measures as may

be deemed appropriate to regulate drinking of liquor or to enforce prohibition of

such drinking in the whole or any part of the Union territory.

95. The Administrator may make rules to regulate movement, possession and

sale of molasses, black jaggery, mahua flower, etc., indicating terms and

conditions as are necessary and expedient to prevent their misuse for illicit

distillation.

96. No advertisement, direct or surrogate, shall be made for promoting

consumption of liquor:

Provided that the Excise Commissioner may, at his discretion, allow such

advertisement which is educative and promotes responsible drinking.

97. The Administrator may, by notification, declare in respect of the whole

of the Union territory or to any local area comprised therein, as regards to

purchasers generally or any specified class of purchasers and generally or for any

specified occasion, the maximum or minimum quantity, or both, of a liquor, which

for the purposes of this Regulation, may be sold by retail and by wholesale.

98. No suits for damages shall lie in any Civil Court against the

Administrator or any officer or person for any act done in good faith, or ordered to

be done in pursuance of this Regulation or of any other law for the time being in

force relating to excise revenue.

99. (1) The Administrator may, by notification, make rules not inconsistent with

the provisions of this Regulation, for carrying out the provisions of this Regulation.

(2) In particular, and without prejudice to the generality of the foregoing

powers, such rules may provide for all or any of the following matters, namely:

(a) the form in which an annual report shall be submitted by the Excise

Commissioner under clause (i) of section 4;

(b) the terms and conditions for grant of reward to the officers and

employees, and informers for the work under section 9;

(c) the manner of registration for the purpose of manufacture of alcohol

exclusively for industrial use under sub-section (2) of section 10;

(d) the fees, period, terms and conditions and form, for grant of licence

(e) the conditions for security and counterpart agreement under section 13;

(f) the restrictions on power of the licensing authority to suspend or

cancel licence or permit under sub-section (1) of section 16;

(g) the terms and conditions subject to which transfer of licence or

permit may be made under section 19;

(h) the terms and conditions for granting of licence or lease under

section 20;

(i) the bond to be executed for removal of liquor from manufactory,

warehouse, etc., under section 21;

(j) the terms and conditions for collection of fee for issue of licence or

permit under sub-section (2), and the manner of assessment of import, export

and transport duties under sub-section (3), of section 26;

(k) the returns, forms and the particulars and such other information to

be submitted by the licensee under section 31;

(l) the value of liquor which may be less than or exceed under clauses (a)

and (b), respectively, of section 32;

(m) the quantity of the liquor to be sold, transported, possessed or

bought by the manufacturer under section 37;

(n) the period within which any major offence may be referred by the

Deputy Commissioner under sub-section (2) of section 68;

(o) the manner of adjudication by an Adjudicating Officer under

sub-section (2) of section 69;

(p) the guidelines for compounding under sub-section (3) and the

manner in which the liquor, apparatus, vehicle or other material seized shall

be disposed of under sub-section (4) of section 70;

(q) the manner in which any liquor, mahua flowers or molasses and

any other confiscated property shall be disposed of under sub-section (7) of

section 73;

(r) the manner and fees for disposal of confiscated property under

sub-section (1) of section 75;

(s) the regulation of movement, possession and sale of molasses, black

jaggery, mahua flower, etc., under section 95;

(t) any other matter which is to be, or may be prescribed under this

Regulation.

100. Every rule made, or notification or order issued, under this Regulation

shall be laid, as soon as may be after it is made or issued, before each House of

Parliament, while it is in session, for a total period of thirty days which may be

comprised in one session or in two or more successive sessions, and if, before the

expiry of the session immediately following the session or the successive sessions

aforesaid, both Houses agree in making any modification in the rule or

notification or order, or both Houses agree that the rule or notification or order

should not be made, the rule or notification or order shall thereafter have effect

only in such modified form or be of no effect, as the case may be; so, however,

that any such modification or annulment shall be without prejudice to the validity

of anything previously done under that rule or notification or order.